The Finish Line reported fourth-quarter earnings topped Wall Street’s targets as better full-price selling at the Finish Line chain, healthy sales at its Macy’s partnership, and robust digital momentum offset below-plan profits at Running Specialty Group.

The Finish Line reported fourth-quarter earnings topped Wall Street’s targets as better full-price selling at the Finish Line chain, healthy sales at its Macy’s partnership, and robust digital momentum offset below-plan profits at Running Specialty Group.

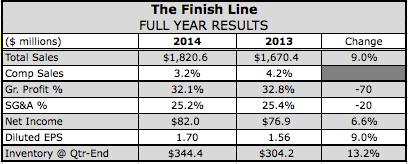

Sales improved 6.3 percent in its quarter ended Feb. 28, to $551.3 million with comps ahead 2.6 percent.

Earnings declined 5.4 percent, to $40.4 million, or 87 cents. Excluding the impact of impairment charges and store closing costs, earnings were down 4.0 percent to $41.3 million, or 88 cents, a share, exceeding the Street’s consensus estimate of 86 cents.

“Our fourth-quarter results, particularly in our core business, represented a solid finish to a disappointing year,” said Glenn Lyon, chairman and CEO, on a conference call with analysts. “The team responded quickly to the product margin headwinds we faced in the back half of the year by reducing expenses to deliver Q4 EPS ahead of guidance.”

He added, “We still have work to do to improve the overall profitability of the company. However, we are encouraged by the improving trends of The Finish Line brand and the continuing growth of our Macy's business.”

The 6.3 percent overall sales increased consisted of a Finish Line comp gain of 2.6 percent; sales associated with Macy's of $61.3 million, up 44.6 percent compared to last year; and Running Specialty Group (RSG) sales of $16.3 million, up 29.2 percent.

Comps at Finish Line rose 6.3 percent in December and 16.2 percent in January, but fell 8.7 percent in February. Comps in March are down slightly month-to-date, although expected to be up low-single digits after this weekend following a strong Jordan Retro launch.

Gross margins decreased 180 basis points to 34.1 percent. Product margin, net of shrink, was down 120 basis points. Officials had expected product margins to be down due to higher markdowns at Finish Line, and that contributed to roughly half of the product margin decline. The other half was driven by an inventory write-down of $3.8 million at RSG to clean up aged and defective product.

SG&A expense were down 30 basis points to 22.4 percent of sales, due to expense management and lower incentive compensation costs.

Sam Sato, president, noted that the 2.6 percent comp gain was in line with the midpoint of its guidance range. Footwear comps inched up 0.5 percent with footwear ASPs ahead mid-single digits. The increase was led by a mid-single digit gain in women's, a “sharp acceleration” from recent quarters. Kids' was up low singles while men's was down low-single digits.

“Full-price selling of footwear improved as we started to see the benefits from having a more relevant product assortment late in the quarter,” said Sato.

Running comps increased low-single digits, highlighted by strong full-price selling of Nike styles led by Roshe Run and Air Max 2015. The Free platform performed better in women's than men's. Under Armour “made a considerable leap in its contribution to sales and margins,” driven by its Scorpio running shoe, as well as new color waves in Speedform. Positive gains were seen from Adidas, Puma, Brooks and Mizuno.

Basketball was down low-single digits although it faced tough comparisons against a mid-teens increase a year ago. Added Sato, “While sales were below plan, margins were in line with expectations, and within the product assortment there were a number of bright spots.”

Brand Jordan and Nike improved and were slightly positive. Jordan Retro styles and Nike signature products, like Lebron, KD, as well as Kyrie Irving’s new shoe, were described as “standouts.” Under Armour's Steph Curry signature sneaker “had a phenomenal debut,” said Sato. The rest of its basketball mix “continues to be disappointing.”

Kids comps increased low-single digits with many of the styles that did well on the adult side doing well in kids. Boots were “up nicely,” led by Timberland.

Soft goods banged out a high-teens comp gain, its third consecutive quarter of positive comp growth. Apparel was “the standout,” driven by branded outerwear and licensed fleece. Accessories returned to positive comp gains, led by socks although it was price-driven and margins declined.

“Overall, we are pleased with the steady progress we are making, improving sales and margin trends through a more exciting and relevant apparel offering,” said Sato. “While there is still work to be done, especially with respect to accessories, we're more optimistic about our outlook for this category.”

On the digital side, traffic to its digital channel, which includes desktop and mobile sites, increased double digits. Mobile now represents over half of its total digital traffic. The launch of a new app and enhancements to its web experience were favorably received. For the first time in any quarter, digital sales represented over 20 percent of total sales, and for the year accounted for over 16 percent.

Looking ahead, Sato said he continues to be “optimistic” around a number of launches, including new iterations from Air Max and Roshe Run, a heightened focus on women's Free, and retro styles like Huarache and Cortez from Nike; Under Armour's Flow; New Balance 574; and new casual running products from Puma. Early sell-through for Reebok's ZPump have exceeded expectations. Said Sato, “Collectively, these new sneakers should drive excitement and additional full-price selling in the category.”

Basketball is expected to return to positive comps in the first quarter, driven by retro and off-court styles from Brand Jordan, signature products from Nike, as well as Under Armour.

Elaborating on progress around its three segments: Lyon said the following an inventory rebalance over the back half of the year, the Finish Line chain is starting to “flow more freshness into the assortments.” Coupled with the expected launches, “this should help drive better full-price selling as the year progresses,” Lyon said.

Lyon also noted that since it launched its digital push three years ago, digital sales have tripled for Finish Line. But Lyon believes the company is only “scratching the surface of this channel's potential,” believing smartphones are becoming “the primary source of customer interaction.”

To build on the current momentum, its digital platform is being upgraded to improve customer experience and more investments are being made to mine data in its loyalty program.

“Capabilities we are developing will allow us to deliver improved, more personalized communications and better understanding of our target customer,” said Lyon. “This will allow us to evolve our tactics as customers evolve their tastes and purchasing habits.”

Finish Line is also spending more on remodels and updating its store design, including expanding the penetration of Nike Track Clubs.

Regarding RSG, Lyon noted that with a number of acquisitions last year, including its recent purchase of JackRabbit Sports in New York earlier this month, RSG now operate 76 locations.

“While the pace of growth has allowed RSG to reach scale, the profitability of this business has fallen short of our expectations,” said Lyon. “We need to drive best practices to create a service and operational model in an omnichannel world that meets our premium standards and can be applied division-wide to achieve profitable growth.”

The “primary focus” at RSG is now shifting from acquisitions to “operational excellence and evolving our channel strategies to better serve the customer.” RSG will be leveraging more of The Finish Line infrastructure to obtain optimal workflow in inventory management, store operations, supply chain, IT, and digital.

“We still view the opportunity to build a national active lifestyle retail brand as very compelling,” said Lyon. “We are confident that the long-term goal of achieving $200 million in sales and a high single-digit operating margin remains clearly in our sights.”

Finally, Lyon said its partnership to run athletic footwear shops inside Macy’s as well as the department store’s online athletic assortments delivered sales ahead of plan this year and was considered a “bright spot” alongside digital this past year. The roll out of the shops was completed and the focus like RSG now shifts to “achieving operational excellence” to drive higher sales and profitability. A particular focus will be on 75 to 100 stores “where we see meaningful upside potential.”

Finish Line sees “tremendous potential” to expand kids and is increasing the number of shops carrying kids. Digital sales growth through macys.com has been on a “steep trajectory” over the last several quarters and is now benefiting from having all 400 in-store shop doors fulfilling online orders. Finally, adjustments are being made to in-store labor scheduling to improve expenses. Said Lyon, “Our Macy's business is now over $200 million and is well on its way to exceeding the long-term vision we initially outlined for this partnership.”

For the fiscal year ending Feb. 27, 2016, Finish Line expects comps to be up in the low-single to mid-single digit range and EPS to increase in the low-single to mid-single digit range over fiscal year 2015 non-GAAP EPS of $1.67.