China's biggest shoe retailer Belle International Holdings Ltd reported net profit rose 1 percent to RMB 5.16 billion ($827 million) for the 14 months ended Feb. 28. Its CEO said the macroeconomic outlook for the next two years is not optimistic.”

The company earned RMB5.11 billion in the comparable 14-month period ended February 2013. Belle, a key distributor for western sports brands such as Nike, Adidas and Puma, changed to a fiscal year ending in February from one ending in December earlier this year.

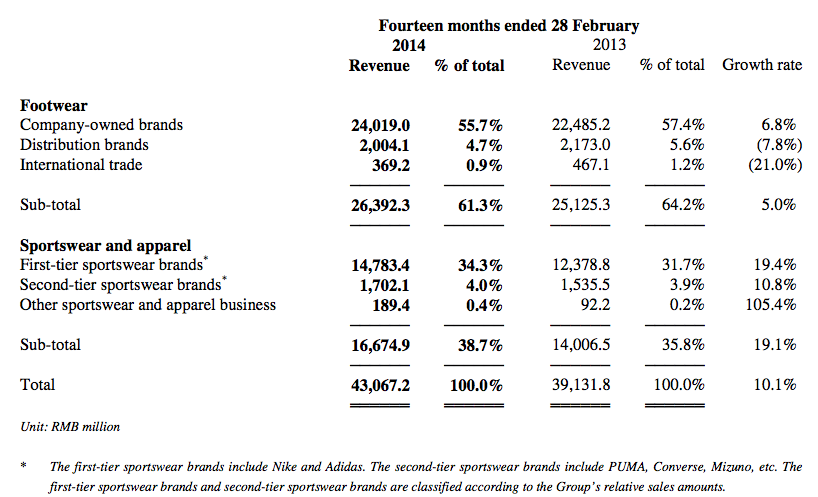

For the 14 months, revenue at Belle rose 10.1 percent to RMB43.06 billion ($5.89 bn) yuan, up from 39.13 billion yuan in the 14 months ended February 2013.

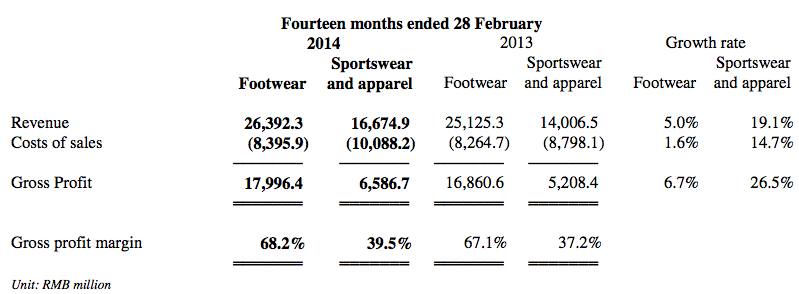

Revenue from the footwear business increased by 5.0 percent, which the company said was “significantly lower than prior years.” The sportswear and apparel business increased by 19.1 percent although the gains were mainly due to the consolidation of the newly acquired business and relatively higher same store sales growth.

Operating profits grew 4.1 percent to RMB6.63 billion ($1.06 bn).

“During the fourteen months ended 28 February 2014, the Group's business continued to be negatively affected by

various factors in the macro environment,” said Belle International Holdings' CEO and Executive Director Sheng Baijiao. “First, with the economy continuing its structural rebalancing and slower growth becoming the new normal, consumer confidence has been low and consumer sentiment weak.

“Second, retail channels continued to evolve rapidly. While the foot traffic in department stores was diluted, the

fast-growing shopping mall channel and e-commerce channel have not become effective retail channels for quality footwear products,” Baijiao continued. “Third, with an unusually warm winter last year and a very cold spring this year, sales performance of footwear and apparel products, being seasonal businesses, experienced strong headwinds over the past two quarters.”

In addition to an unsupportive macro environment and sluggish consumer demand, he said businesses are also facing challenges of rising costs. Various costs and expenses, especially staff related costs and expenses, are expected to continue to rise. In the near term, he said the Group does not expect significant changes to the current situation of slow growth and margin pressure.

“The macroeconomic outlook for the next two years is not optimistic,” Baijiao said. “The consumer retail market is expected to be under continued pressure due to weak consumer sentiment. Retail channels continue to evolve at a rapid pace. Traditional retail channels including the street shops and department stores are under continued pressure due to dilution in foot traffic. New emerging channels have not been effectively utilized by fashion footwear and apparel retailers. A “new normal” state of lower growth is here to stay. Profitability, on the other hand, is

also facing continued challenges.”

The full statement is here.