Yue Yuen Industrial (Holdings) Limited reported that revenues increased 5.1 percent to US$8.97 billion in the year ended December 31, compared to US$8.53 billion in the prior year, with “mostly solid growth” of its manufacturing business being partially offset by weak retail sales in mainland China. The company pointed to “volatile retail sentiment due to pandemic outbreaks and control measures during the year” as the primary reason for the retail shortfall at its Pou Sheng subsidiary.

The profit attributable to owners of the company was US$296.3 million, an increase of 157.5 percent compared to US$115.1 million recorded for the previous year. The profit attributable to owners of the manufacturing business increased by 257.0 percent to US$288.1 million, while the profit attributable to owners of Pou Sheng retail operation decreased by 75.0 percent to RMB89.2 million. Basic earnings per share for the year under review was 18.41 US cents, as compared to 7.15 US cents for the previous year.

Full-Year Revenue Analysis

In the year ended December 31, 2022, revenue attributed to footwear manufacturing activity (including athletic/outdoor shoes, casual shoes and sports sandals) increased by 28.2 percent to US$5.71 billion, compared with the previous year. The volume of shoes shipped during the year was 272.7 million pairs, representing an increase of 14.4 percent which was attributed to solid global demand for its footwear products, together with a low-base effect following disruptions to its Vietnam operations in the third quarter of the previous year. The average selling price increased by a robust 12.0 percent to US$20.93 per pair, led by resilient demand for the Group’s high-end footwear, as well as its ongoing efforts to refine its product mix by obtaining more high-value orders.

The Group’s total revenue with respect to the manufacturing business (including footwear, as well as soles, components and others) in the year ended December 31, 2022, was US$6.20 billion, representing an increase of 26.2 percent as compared with the previous year.

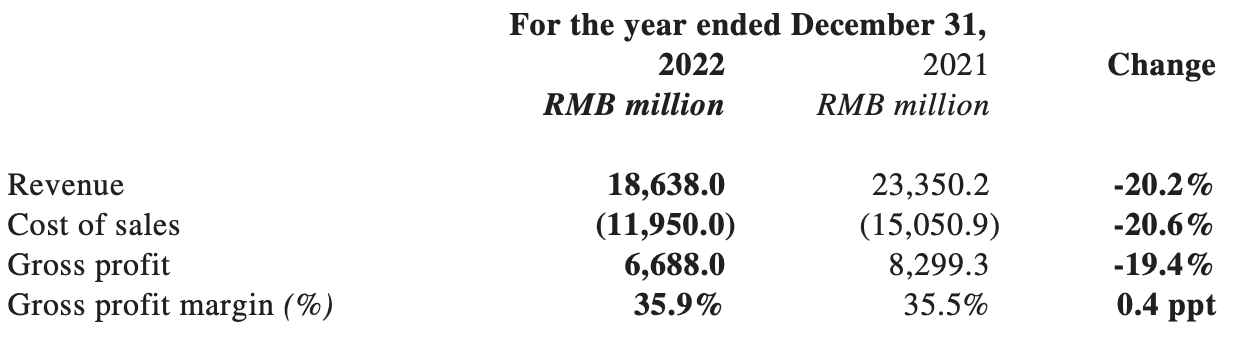

In the year ended December 31, revenue attributed to Pou Sheng, the Group’s retail subsidiary, declined by 23.5 percent to US$2.77 billion, compared to US$3.62 billion in the previous year. In RMB terms (Pou Sheng’s reporting currency), revenue decreased by 20.2 percent to RMB18.64 billion, compared to RMB23.35 billion in the previous year, despite a strong start to the year in early 2022 and the “solid performance of its Pan-WeChat Ecosphere.” The decline was mainly attributed to soft consumer sentiment and volatile foot traffic in the shopping venues and cities where Pou Sheng operates following control measures introduced by local governments across mainland China.

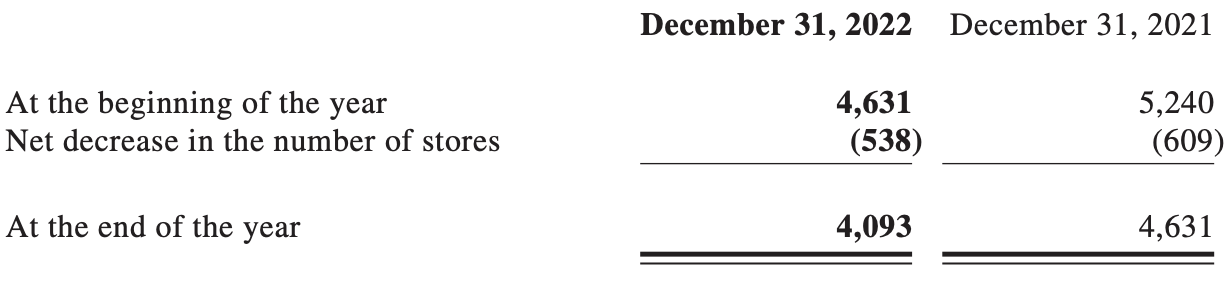

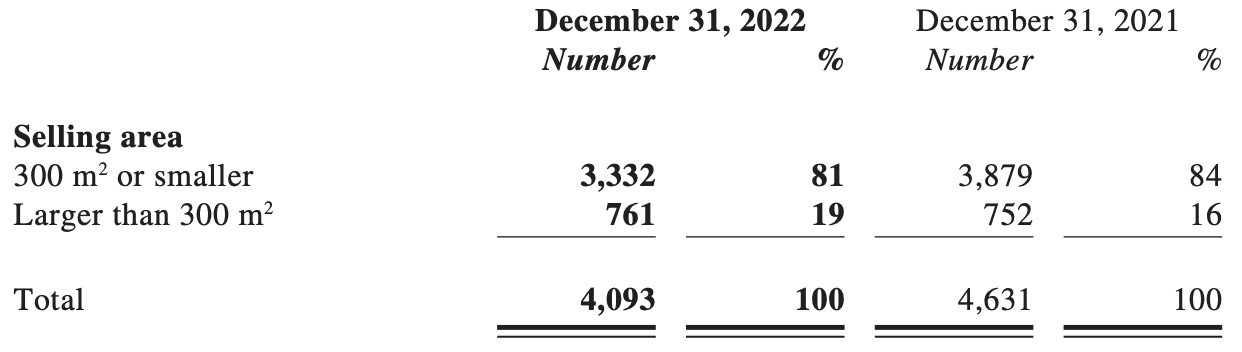

As of December 31, 2022, Pou Sheng had 4,093 directly operated retail outlets and 3,200 sub-distributors stores across the Greater China region, representing an overall net closure of 1,124 stores as compared with the 2021 year-end.

The net closure is in line with Pou Sheng’s retail refinement strategy that focuses on streamlining and refining store networks to enhance efficiency. It has also leveraged its operational expertise, adopting a more holistic approach and prioritizing selective high-quality openings with business partners. As a result, the contribution of quality larger-format stores (above 300 square meters) to Pou Sheng’s directly-operated store count rose to 18.6 percent (2021: 16.2 percent).

Gross Profit

In the year ended December 31, the Group’s gross profit increased by 4.3 percent to US$2.14 billion. The overall gross profit margin decreased by 0.2 percentage points to 23.8 percent of sales. The gross profit of the manufacturing business increased by 50.2 percent to US$1.14 billion. The gross profit margin of the manufacturing business expanded to 18.4 percent of sales, an increase of 2.9 percentage points as compared with the prior year, with the gross profit margin improving sequentially on a quarter-on-quarter basis in the first three quarters of the year and maintaining a solid trend in the final quarter when headwinds impacted the Group’s capacity utilization due to softer demand. The increase in the full-year gross profit margin of the manufacturing business for 2022 was attributed to improved capacity utilization and production efficiency for most of the year, better operating leverage brought by a recovery in sales scale, a low-base effect following disruptions to its Vietnam operations in the third quarter of 2021, stringent cost control measures, as well as agile balancing of demand and capacity. The foreign exchange trend was also favorable, benefiting part of the Group’s local production costs in Southeast Asia during the second half of year 2022.

Pou Sheng’s gross profit margin increased by 0.4 percentage points to 35.9 percent of sales in 2022 as compared to the prior year. The resilient year-on-year performance was mainly attributed to an enhanced channel mix within the current volatile retail environment.

Selling & Distribution Expenses and Administrative Expenses and Other Income/Expenses

The Group’s total selling and distribution expenses for 2022 amounted to US$988.5 million (2021: US$1.19 billion), equivalent to approximately 11.0 percent (2021: 13.9 percent) of revenue. Administrative expenses for 2022 were US$609.1 million (2021: US$611.9 million), equivalent to approximately 6.8 percent (2021: 7.2 percent) of revenue.

Following the Group’s efforts in cost control and efficiency enhancement, the expenses to revenue ratios stated above decreased as compared with the previous year.

Other income for 2022 decreased by 6.3 percent to US$131.3 million (2021: US$140.1 million), equivalent to approximately 1.5 percent (2021: 1.6 percent) of revenue. Other expenses increased by 12.7 percent to US$254.1 million (2021: US$225.4 million), equivalent to approximately 2.8 percent (2021: 2.6 percent) of revenue.

Recurring Profit Attributable To Company Owners

In the year ended December 31, 2022, the Group recognized a non-recurring profit attributable to owners of the company of US$4.5 million, due to a gain of US$8.9 million on fair value changes on financial instruments at fair value through profit or loss (“FVTPL”), as well as a gain of US$3.6 million on the disposal of a joint venture, largely offset by a loss due to fair value changes on investment properties. In 2021, the Group recognized a non-recurring profit attributable to owners of the company of US$52.1 million, which included a combined gain of US$33.6 million due to fair value changes on financial instruments at FVTPL and investment properties, and a combined one-off gain of US$32.0 million on the disposal of a joint venture and associates, which was partly offset by an impairment loss of US$14.0 million on interest in an associate.

Excluding all items of non-recurring in nature, the recurring profit attributable to owners of the company for the year ended December 31, 2022 increased substantially by 363.1 percent to US$291.9 million, compared to a recurring profit attributable to owners of the company of US$63.0 million for the previous year.

Fourth Quarter Analysis

For the fourth quarter ended December 31, total revenues declined 4.5 percent to US$2.00 billion from US$2.09 billion in the prior-year quarter. The decline was primarily attributed to the Retail business in China, which fell 29.3 percent to US$588.7 million in the period, and to a lesser extent, the Soles & Component business, which declined 14.6 percent to US$97.2 million in the quarter.

Fourth quarter revenue attributed to footwear manufacturing activity (including athletic/outdoor shoes, casual shoes and sports sandals) increased by 14.6 percent to US$1.32 billion, compared with US$1.15 billion in the prior-year quarter.

Consolidated Group gross margin was up 70 basis points to 24.0 percent of sales in the fourth quarter. Total net profit jumped five-fold to US$20.9 million in Q4 2022, compared to US$3.4 million in the prior-year period.

Year-End Financial Position

As at December 31, the Group had net borrowing of US$416.7 million (December 31, 2021: US$879.1 million) and a net gearing ratio (net bank borrowings to total equity) of 9.0 percent (December 31, 2021: 19.1 percent). Overall net increase in cash and cash equivalents amounted to US$188.3 million (2021: net decrease US$65.0 million).

Share of Results of Associates and Joint Ventures

In 2022, the share of results of associates and joint ventures was a combined profit of US$62.6 million, compared to a combined profit of US$11.8 million in the previous year.

Prospects

The Group remains optimistic about the prospects of its manufacturing business in the long term. However, many headwinds are impacting the global macroeconomic environment, including inflation, rising interest rates and other uncertainties. This is continuing to result in soft global demand and low visibility that combined together with high inventory levels will weigh on the near-term performance of the Group’s manufacturing business. With the short-term demand outlook for footwear remaining cloudy and the magnitude of order recovery uncertain, the Group will continue to actively manage its supply chain and its manufacturing capacity to balance demand, its order pipeline and labor supply to control risk. It will sustain its efficiency and productivity, as well as the highest level of flexibility and agility, by leveraging its core strengths, adaptability, and competitive edges to overcome any short-term disruptions and safeguard its profitability.

The Group will also strengthen its mid-term capacity allocation strategy of continuing to diversify its manufacturing capacity in regions such as Indonesia and other potential countries where labor supply and infrastructure are supportive of sustainable growth once demand recovers. It will continue to exploit its strategy of prioritizing value growth, leveraging the ‘athleisure’ and premiumization trends to seek more high value-added orders with a better product mix.

The Group will continue to pursue its long-term digital transformation strategy with an aim of achieving operational excellence through digital lean management, having rolled out a new wave of SAP ERP implementation coupled with the implementation of other real-time data applications and remote monitoring systems. It will also continue to proactively adapt its production capacity and capability to cater to the fast-moving market environment and ongoing trends, including increased demand from brand customers for greater versatility, flexibility, eco-friendliness, more efficient turnaround times, on-time delivery and end-to-end capabilities. This includes enabling digital prototyping and production simulations, automation, more flexible set-ups and frequent line change-overs through process re-engineering, and the further integration of other digitalization tools such as increasingly important Operational Control Procedures (“OCP”) and Distributed Resource Scheduler (“DRS”) to optimize its ongoing eco-intelligent and smart manufacturing strategy.

Following the easing of control measures and benefiting from an earlier Chinese New Year, the Group’s retail business, Pou Sheng, has seen sound recovery momentum and improved in-store traffic and purchase intent in certain regions. The Group is cautiously optimistic about a recovery of Pou Sheng, despite the likelihood of short-term volatility in consumer confidence. The prospects of the sports industry remain bright. It will continue to refine its growth strategies and pursue its own digital transformation by further strengthening and diversifying its omnichannel, as well as elevating digitally-enabled physical stores. It is actively expanding its strategic alliance with its brand partners, many of whom are long-term customers of the Group’s manufacturing business, in ways that support inventory integration, loyalty and membership growth, increase in-season sales, and accelerate the sales cycle to ensure better profitability and operating efficiency

The Group will continue to benefit from cross-business synergies while providing differentiated value-added and one-stop services to its customers and strategic partners.

Going forward, the Group remains confident that the above strategies will enable it to continue providing its brand partners with the best possible end-to-end solutions, anchoring its quality growth while safeguarding its solid long-term profitability and ability to deliver sustainable returns to shareholders.

Mr. Lu Chin Chu, chairman, commented, “We once again proved our resilience and unmatched expertise, delivering expanded top-line and bottom-line growth within an exceptional and unpredictable industry environment. These attributes will no doubt help us navigate the toughening demand cycle we are facing on the manufacturing side of our business. We remain committed to delivering for our shareholders with our ongoing growth and profit-accretive strategies. I am also pleased to share that the Group’s CDP Climate Change Score was upgraded to ‘B’ (Management) level and its MSCI ESG rating was maintained at ‘BBB’, reflecting the efforts and that of its parent company, Pou Chen, in setting targets and taking action to enhance sustainability, good working relationship and corporate governance.”