Callaway Golf Company reported sales increased 8 percent in the third to $263 million, a record for the third quarter. The continued net sales growth was led by increases in Gear, Accessories and Other (29 percent), Putters (28 percent), Balls (14 percent) and Irons (7 percent). In addition to this sales growth, the company also significantly improved profitability including a 77 percent increase in income from operations as compared to the third quarter 2017.

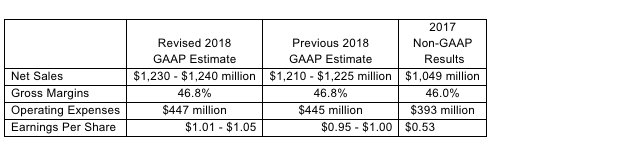

As a result of this better-than-expected quarter, the company increased its full year sales guidance by $15 million-$20 million to $1,230 million-$1,240 million as compared to prior guidance of $1,210 million-$1,225 million. The company also increased its full year 2018 earnings per share guidance to $1.01-$1.05 compared to prior guidance of $0.95-$1.00.

“The third quarter results continue what has been a tremendous year for Callaway,” commented Chip Brewer, president and chief executive officer of Callaway Golf. “All major regions and product categories continue to perform at a high level, including our TravisMathew business, which we acquired in August 2017. On a year-to-date basis, our net sales increased $205 million (24 percent) to $1,062 million, a record for the company, while gross margins increased 110 basis points and adjusted EBITDA increased $73 million, or 63 percent, compared to the same period in 2017. This is a result of the continued strength across our entire product line, favorable industry conditions and in the first half of the year favorable foreign currency market conditions, as well as the investments we have made the last couple of years in our core business and our acquired businesses. I am pleased with our performance this year and remain optimistic about our long-term outlook.”

Summary of Third Quarter 2018 Financial Results

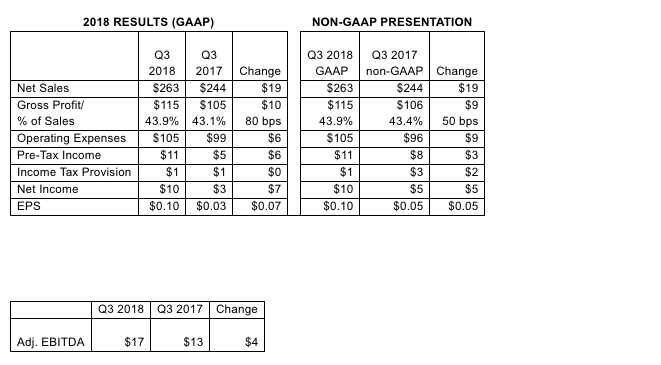

For the third quarter of 2018, the company’s net sales increased $19 million (8 percent) to $263 million, compared to $244 million for the same period in 2017. Net sales increased in all major regions and all product categories except Woods. The decrease in Woods sales for the quarter was expected and is a result of the product launch timing for Woods in 2018 (on a year-to-date basis, net sales of Woods increased 4.8 percent). The increase in net sales is attributable to the continued strength of the company’s 2018 product line and brand momentum, the addition of the TravisMathew business and improved market conditions.

For the third quarter of 2018, the company’s net sales increased $19 million (8 percent) to $263 million, compared to $244 million for the same period in 2017. Net sales increased in all major regions and all product categories except Woods. The decrease in Woods sales for the quarter was expected and is a result of the product launch timing for Woods in 2018 (on a year-to-date basis, net sales of Woods increased 4.8 percent). The increase in net sales is attributable to the continued strength of the company’s 2018 product line and brand momentum, the addition of the TravisMathew business and improved market conditions.

For the third quarter of 2018, the company’s gross margin increased 80 basis points to 43.9 percent compared to 43.1 percent for the third quarter of 2017. This increase was primarily driven by increased average selling prices, favorable product mix and the TravisMathew business, which is accretive to gross margins, offset slightly by higher product costs due to more technologically advanced products.

Operating expenses increased $6 million to $105 million in the third quarter of 2018 compared to $99 million for the same period in 2017. This increase is primarily due to the addition of operating expenses from the TravisMathew business in 2018 as well as some variable expenses associated with higher core business net sales.

Third quarter 2018 earnings per share increased $0.07 (233 percent) to $0.10 compared to $0.03 for the third quarter of 2017. On a non-GAAP basis, 2017 third quarter earnings per share was $0.05, which excludes $0.02 per share related to the impact of the non-recurring OGIO and TravisMathew transaction and transition expenses. The increased earnings in 2018 are the result of the increased sales in the core business, the addition of the TravisMathew business, improved gross margins, operating expense leverage and a lower tax rate due to the tax reform legislation enacted at the end of 2017.

Summary of First Nine Months 2018 Financial Results

For the first nine months of 2018, the company’s net sales increased $205 million (24 percent) to a record $1,062 million compared to $857 million for the same period in 2017. Net sales increased in all operating segments, all regions and across all product categories. The increase in net sales is attributable to the strength of the company’s 2018 product line and continued brand momentum, a $16 million favorable impact resulting from changes in foreign currency rates and improved market conditions. In addition, year-to-date net sales of gear and accessories increased significantly as a result of the company’s acquisition of TravisMathew in the third quarter of 2017.

For the first nine months of 2018, the company’s gross margin increased 110 basis points to 47.9 percent compared to 46.8 percent for the first nine months of 2017. This increase reflects an overall increase in average selling prices, the addition of the TravisMathew business, which is accretive to gross margins, and the net favorable translation impact of changes in foreign currency rates, partially offset by higher product costs as more technology is incorporated into the new product line.

Operating expenses increased $36 million to $337 million in the first nine months of 2018 compared to $301 million for the same period in 2017. This increase is primarily due to the addition of operating expenses from the TravisMathew business in 2018 as well as some variable expenses associated with higher core business net sales and continued investment in the core business.

First nine months 2018 earnings per share increased $0.75 (121 percent) to $1.37, compared to $0.62 for the first nine months of 2017. On a non-GAAP basis, 2017 first nine months earnings per share was $0.69 which excludes $0.07 per share related to the impact of the non-recurring OGIO and TravisMathew transaction and transition expenses. The increased earnings in 2018 reflect the increased sales in the core business, the addition of the TravisMathew business, improved gross margins, operating expense leverage, favorable foreign currency rates and hedging activities and a lower tax rate due to the tax reform legislation enacted at the end of 2017.

Business Outlook for 2018

The company’s revised 2018 net sales estimate of $1,230 million, $1,240 million, represents an increase of $15 million, $20 million over its prior estimate. This would result in net sales growth of 17 percent – 18 percent in 2018 compared to 2017. The estimated, incremental sales growth compared to previous estimates is expected to be driven by further increases in the core business (currently estimated at 12-13 percent full year sales growth compared to 2017). The increases in core business are expected to be driven by the Rogue line of woods and irons, the new Chrome Soft golf balls, including continued success of the Truvis golf balls and continued healthy market conditions. As a result of an overall strengthening of foreign currencies during the first half of 2018, the company currently estimates that changes in foreign currency rates will positively impact 2018 full-year net sales by approximately $14 million consistent with previous guidance.

The company estimates that its 2018 operating expenses will increase $2 million compared to prior estimates. Variable expenses related to higher sales are causing the increase. The company continues to realize operating expense leverage as the top line increases.

The company increased its GAAP earnings per share guidance to $1.01 – $1.05 primarily due to the projected increase in net sales, operating expense leverage and a lower estimated tax rate. The company’s 2018 earnings per share estimates currently assume a tax rate of approximately 21.0 percent and a base of 97 million shares.

Image courtesy Callaway Golf