Global fast fashion retailer ASOS plc entered fiscal 2023 in a challenging position. Company CEO José Antonio Ramos Calamonte said they had more stock than they would have liked, their buying processes were too deep and too slow, they lacked profitability and they had tension in their balance sheet with earnings-based covenants on their debt. Despite making progress against most the issues they faced during the year, the company has reduced its expectations for its cash flow for the year due to timing effects.

Summary Unaudited Financial Results*

Calamonte said in a recent statement regarding an outline of Q4 and full-year results that they addressed those issues by refinancing their balance sheet and rebuilding their leadership team.

“I also explained that we had begun to pivot to a new commercial model that puts speed at the heart of everything we do, bringing the most relevant and exciting fashion to our customers and making our operations more profitable and more cash generative,” Calamonte said.

The company said in the most recent release that it has continued to execute on its Driving Change agenda. The following progress was made during the full-year period ended September 3:

- Adjusted H2 EBIT was up more than 100 percent year-over-year (YoY) and H2 cashflow improved by approximately £140 million despite double-digit revenue decline, reflecting material improvements to core profitability and strong inventory management.

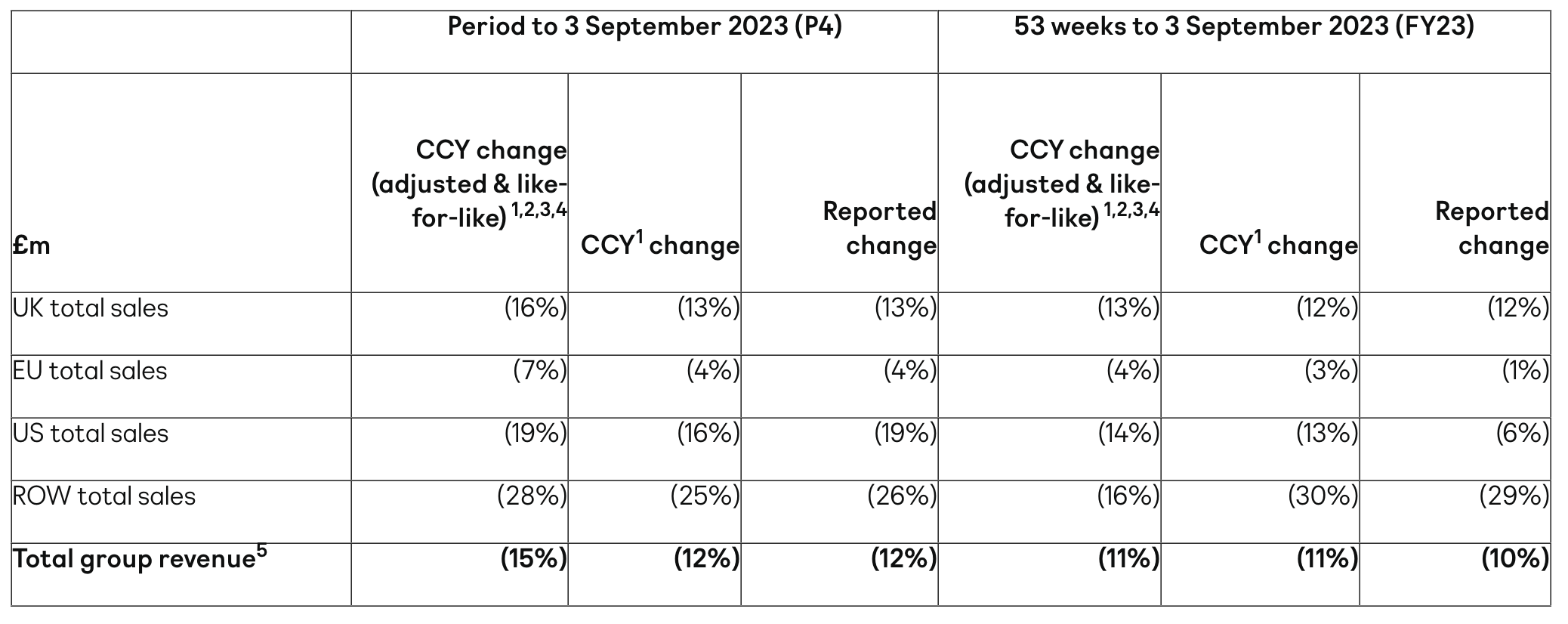

- Sales declined 15 percent YoY in Q4, in line with guidance, with a stronger start to the period followed by weaker performance in July and August amidst a deterioration in the UK clothing market.

- Despite the decline in sales, Q4 is reported to be another profitable quarter. Approximately £300 million of profit improvement and cost savings have now been realized, in line with the FY23 target set under the Driving Change agenda, driving order profitability up more than 35 percent YoY.

- Adjusted gross margin up approximately 150 basis points (bps) YoY in H2 (vs. guidance up approximately 200 bps), driven primarily by lower freight and duty costs, partially offset by tactical investment in promotional activity to prioritize stock reduction in a challenging trading environment.

As such, inventory was down approximately 30 percent YoY, ahead of guidance, supporting the transition to the new commercial model in FY24 and beyond.

The pivot to a faster stock model is said to be on track with approximately 500 Test & React options launched on approximately 2-week lead times, with approximately 60 percent of each product launch selling through in seven days and stock turning approximately 3x faster than average.

EBIT is now expected around the bottom of the guided £40 million to £60 million range, with free cash inflow in H2 now expected to be approximately £60 million excluding refinancing costs (previously £150 million), principally as a result of timing effects that will reverse in September and October.

All other guidance remains unchanged.

Cash and undrawn facilities totaling approximately £430 million at year-end, providing substantial liquidity following the refinancing and equity raise announced in May 202.

“ASOS has delivered on the Driving Change agenda and as a consequence is a leaner and more resilient business twelve months after its launch,” Calamonte suggested. “We have reduced our stock balance by approximately 30 percent, significantly improved the core profitability of the business and generated cash against a very challenging market backdrop. We continue to focus on bringing the best fashion and the most engaging proposition to our customers as we make progress on our journey to sustainably profitable and cash-generative growth.”

He said that inventory is now down ahead of guidance, by approximately 30 percent YoY, and order profitability is up over 35 percent as a result of targeted action to manage the least profitable customers.

“Most pleasingly, new product operating under our refreshed commercial model is performing well and our Test & React pilot has produced extremely positive results that we will scale up over the coming months,” he offered.

“We have successfully reduced inventory more than planned while delivering sales and profit broadly in line, but cash generation in the period has lagged, predominantly as a result of timing,” Calamonte suggested.

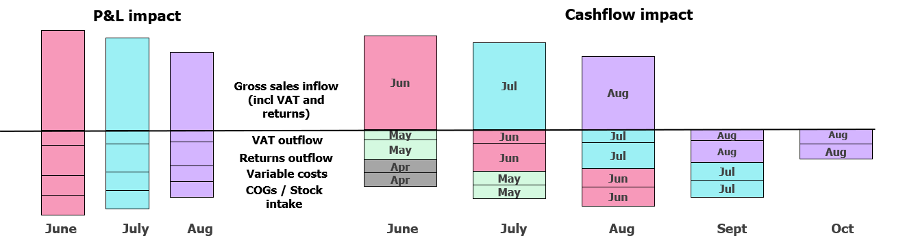

“Across many of our markets (but most notably the UK), the hot weather drove a strong June and a wet July and August produced a weaker sales result,” he explained. “While the stronger-than-expected June and weaker-than-expected July and August broadly netted out to deliver sales and EBIT in line with guidance, the phasing of sales impacted year-end cashflow. This is due to the immediate reduction in the cash inflow from our sales and the delayed reduction in the cash outflow on our costs.” See below for the company-provided graphic outlining the shifting cash flow impact.

Calamonte said they typically receive cash from their sales gross of returns and sales tax immediately. However, the cash outflow from sales tax, returns and variable costs associated with those sales predominantly impact the following two months. As a result, cash flow was negatively impacted by approximately £60 million as weaker July and August gross sales coincided with higher sales costs from strong June trading.

He said this impact will reverse during September and October.

Progress Towards a New Commercial Model

Calamonte said there are two key stages to our new commercial model, converting current inventory into cash and then turning inventory faster on an ongoing basis to make the business model more cash-generative.

“Over the last year (starting with our £130 million stock write-down) we focused the business on selling excess stock and improving the way we buy stock, buying less on faster lead times with more flexibility. To achieve this, we have rewritten our commercial model to focus on speed, this means a better customer proposition, less inventory risk, higher margins and greater cash generation,” he explained.

“Despite the difficult trading environment, we have reduced inventory by approximately 30 percent during FY23 which has required higher levels of discounting in the short-term as well as reducing our intake, which as I previously shared, has resulted in reduced width and newness, negatively impacting revenue,” Calamonte continued. “This elevated level of discounting is likely to persist through FY24, and notably through P1, as we seek to clear last year’s Autumn/Winter stock, which is now among our oldest inventory. We remain on track to return stock to pre-COVID levels by the end of FY24 (reducing stock below £600 million), which will importantly continue to drive down our net debt.”

Calamonte said its newest, high fashion product is selling very well, with a 50 percent increase in 4-week sell-through since the start of the year.

“However, due to our reduced stock intake and seasonally low newness in July and August, new stock is a low proportion of sales and the strong performance on new products has therefore not been enough to offset the challenging discount season for clearance product,” he said.

In September, the proportion of inventory that is less than a month old will have almost doubled from the levels seen in July, which improves the proposition for their customers, according to the CEO’s comments.

“Over the course of the last year, we have made substantial progress on initiatives to improve our stock efficiency on an ongoing basis, and in FY24 we will see these measures ramp up,” Calamonte continued. “On the own-brand side, our Test & React pilot has been a resounding success. As a reminder, we define Test & React to be a product that moves from initial design to available on-site in less than three weeks. This enables us to react to fashion trends and produce products we know our customers want. We have now launched approximately 500 Test & React options, reducing lead times to around two weeks and with close to two-thirds of each product run selling through in the first seven days. When it comes to partner brands, the technology and team are now in place to enable us to scale up the number of brands operating on the Partner Fulfills model in the next twelve months, providing additional width and depth to our assortment while simultaneously reducing inventory risk and enabling us to better curate our local product offering in international markets.

“These initiatives will be transformative for our customer proposition and for our ability to generate profit and cash,” Calamonte explained. “There is still a lot for us to learn, but we have an experienced and dedicated team.”

Calamonte revealed that as part of this transformation, he hired Elena Martínez Ortiz as senior product director. Elena joined ASOS as womenswear director in August 2022, following nearly 18 years at Inditex, where, most recently, she was product director. Ortiz has been instrumental in the launch of Test & React and is said to be the “driving force” behind the company’s speed-to-market initiatives. In her new role, she reportedly becomes the single leader of the company’s product organization, with responsibility for all ASOS-owned brands and partner brands sold through ASOS. This is expected to simplify decision-making and hence accelerate speed to market.

Improving Profitability

Calamonte said the company’s new commercial model improves profitability, requiring lower investment into discounting as well as potentially increasing basket value and customer lifetime value once fully operational. The company has already seen these benefits on a small scale through its Test & React trials with no promotional investment to sell through approximately 60 percent of each product launch in seven days across approximately 500 options produced to date, more than offsetting the higher cost of goods for product created under this model. For its partner brands, its rollout of DTC solutions, including partner fulfills, will also reduce the risk of inventory overhang typical of branded products sold through its retail model that is often ordered around nine months ahead of the point of purchase.

Calamonte said these benefits will accelerate as they scale up the company’s flexible stock models; however, he said the core improvements they implemented over FY23 to drive the more than 35 percent YoY improvement in order profitability and 100 percent improvement in H2 EBIT include:

- Targeted action to improve the behavior of the least profitable customers including reduced marketing contact and restrictions on Buy Now, Pay Later solutions at checkout, with a positive impact on the return rate since these changes were introduced. Asos has also recently launched personalized marketing to improve the profitability of its entire customer base.

- Charging for returns in a number of non-core markets or introducing charges for returns made after fourteen days but within the twenty-eight-day returns window and maximizing the opportunity to resell returned products at full price.

- Optimization of the distribution network resulting in an approximately 20 percent reduction in the UK fixed warehouse cost per unit despite inflation headwinds.

“While some of these profitability measures have led to higher levels of churn (23.3m active customers at FY23, down approximately 9 percent YoY and approximately 3 percent from Q3) we have exited our least profitable orders and customers as evidenced by the approximately 35 percent increase in profit per order over the period and lower than expected returns rate. We are laying the right foundations for sustainably profitable and cash-generative growth. We will provide a more detailed update on our FY24 strategy alongside our FY23 results,” Calamonte concluded.

The company’s FY 2023 results announcement and analyst presentation will take place on October 25, 2023.

*Notes: Summary Unaudited Financial Results

- Constant currency is calculated to take account of hedged rate movements on hedged sales and spot rate movements on unhedged sales.

- Adjusted revenue excludes non-underlying jobber income associated with the transition to the new Commercial Model across FY23.

- Like-for-like sales are adjusted to remove the benefit of the additional three days of trading in Q4 FY23 (1 June to 3 September 2023) vs. Q4 FY22 (1 June to 31 August 2022) and the additional three days of trading in FY23 (1 September 2022 to 3 September 2023) vs. FY22 (1 September 2021 to 31 August 2023). The impact of the additional days is approximately 3 percent at group level in Q4 FY23 and approximately 1 percent in FY23.

- All numbers subject to rounding. Revenue is stated at constant currency, adjusted for non-underlying items, based on like-for-like sales (as defined in note 3 above) and excludes Russia from the FY22 comparative base period following the decision to suspend trade in Russia on 2 March 2022, unless otherwise stated. Any other adjusted measures exclude non-underlying items.

- Includes retail sales, wholesale and income from other services comprising delivery receipt payments, marketing services and commission on partner-fulfilled sales.

Photo courtesy ASOS