Accell Group N.V. published its annual results for the 2017 financial year and presented a strategy update for the period 2018-2022.

Financial Highlights

- Adjusted net turnover up 3.7 percent1 at €1,069 million, largely on the back of growth in e(performance) bikes and strong contributions from Germany, Austria, Switzerland (DACH) and France, turnover increase under pressure from reduced bike sales in North America and the Netherlands

- Operating result 37.1 percent lower at €38.0 million, primarily due to (1) weak performance and transformation of the organisation in North America (in total €10 million) and (2) extra (budgeted) costs for the implementation of the group strategy

- High tax rate due to non-cash write-off of tax assets in North America and Finland resulted in net profit of €10.5 million; dividend proposal of €0.50 per share

Strategic Highlights

- Refined strategy with six renewed pillars to form basis for realisation of growth and profit ambitions for 2018-2022; turnover to €1.5 billion and ROCE above 15 percent

- Strategy roll-out accelerated with stronger emphasis on reduction of complexity within the group, centralized management of (e-)commerce and innovation, plus use of scale and synergy potential across the value chain and all regions. Additional expenses of strategy execution amount to a total of €30-€40 million over the next five years, on top of the 2017 expenditure

- Anticipated realisation of €60-€80 million in structural savings on an annual basis by 2022

- 2018 will be key transitional year; announcement of changes in board

KEY FIGURES

Ton Anbeek, chairman of the Board of Directors: “In 2017, we started the executing of our new strategy in Europe and North America. Unfortunately, the initial results of this strategy were overshadowed by a disappointing performance in North America. Sales via existing distribution channels (IBDs and multi-sport) came under pressure and the contract with a major multi-sport chain was terminated. These developments prompted a restructuring, including the replacement of the local management and an adjustment of the North American organization, which also gave rise to a necessary correction on US import levies for the period 2013-2017.

In Europe, we benefited from our leading position in the field of e-bikes. Sales of e-performance bikes for active recreation and sports saw a particularly strong increase and we also recorded a further increase in the order file for 2018. Turnover of regular bikes declined, but this was compensated by the higher turnover of e-bikes. In addition to e-bikes sales, we also recorded an organic increase in the turnover of parts and accessories, partly on the back of growth in our own XLC brand. The higher turnover in Europe translated into a higher underlying operating result for our European businesses.

In 2017, we incurred extra costs of €7 million for the roll-out of our strategy. As part of this drive, we raised the supply chain organization to full capacity and we are making considerable headway in the field of parts and accessories, portfolio management and IT.

We have refined the strategy and translated it into a concrete roadmap for the period 2018-2022, including related goals and guidance for required investments and anticipated savings. Our ambition is to become market leader in the mid and high end of the e-bike market in a consumer-centric and socially responsible way. For this, 2018 will be an important transitional year. We will accelerate our strategy roll-out and reduce the complexity of the group in order to better and faster anticipate changes in the market. As such, we can add more value for dealers and consumers and at the same time realize our ambitions for growth and profitability.”

Strategy Update 2018-2022

- For 2022 Accell Group has outlined the following financial objectives:

- Net turnover of around €1.5 billion

- Added value of more than 31 percent

- EBIT margin of around 8 percent

- Working capital of less than 25 percent of turnover

- ROCE of more than 15 percent

We have built this strategy on six renewed, strategic pillars to help us realize these goals: (1) Lead global. Win local.; (2) Winning at the point of purchase; (3) Consumer-centric omni-channel business model; (4) Innovation; (5) Centralized and integrated Parts & Accessories business and (6) Fit to compete. Within this framework, Accell Group will accelerate roll-out of the following initiatives as of the second quarter of 2018:

- Realisation of central management and coordination of commerce policy, the innovation programme and production allocation within the group

- Focus on large-scale innovations combined with less fragmented and higher marketing budgets

- Determination per country of a strategic brand portfolio for marketing and sales via and with dealers, and with emphasis on avoiding channel conflicts

- Per country, focus on perfect execution of plans geared towards maximization of customer satisfaction and improved utilization of opportunities in the local market

- Formation of six key regions (DACH, Benelux, Southern Europe, UK & Ireland, Scandinavia and North America), which together represent almost 100 percent of turnover

- Focus on e-bikes supported by digital platforms, experience centres and mobile bike service

- Centralisation and increased integration of parts and accessories with bicycle activities in each region

- Accelerated implementation of the centrally-managed supply chain with an emphasis on further rationalization, standardization and reduction of complexity, Accell Group expects the investments and costs associated with the implementation of the strategy to total €30-€40 million, on top of the €7 million spent on this front in 2017. The aim is to realize €60-€80 million in structural savings on an annual basis in 2022.

Group Performance

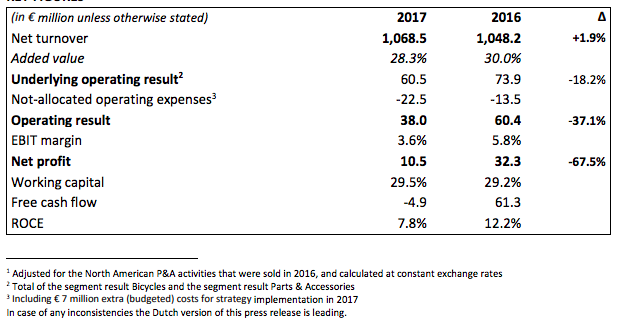

Net turnover came in 1.9 percent higher at €1,069 million in 2017 (2016: €1,048 million). Adjusted for the sale of the parts and accessories activities in North America in 2016, organic turnover growth was 2.7 percent. Including the adjustment for the effect of currency exchange rates, growth came in at 3.7 percent.

The added value (net turnover less cost of materials and incoming transport costs) as a percentage of turnover came in at 28.3 percent. The added value was primarily impacted by the increase in the share of ebikes, reduced margins on regular bikes and higher discounts. Added value was further pressured by overdue US import duties of on average €0.8 million per year for the period 2013-2017, resulting in a total one-off charge of €4 million.

During the transformation of the North American organisation, it came to light that the import classification of hybrid bikes (sports bikes combining the properties of both racing bikes and mountain bikes) had not been applied uniformly during the past years. The new local management discovered that insufficient US import duties on these bicycles were paid, because the allocation of classification codes had not been carried out scrupulously enough. The classification codes currently used are correct and the lack of uniform application in the past does not affect the operational developments. Due to the self-correction, fines do not apply. Legal interest will be charged on the amounts to be repaid, which has been included in the one-off charge.

Operating costs were 3.8 percent higher at €264 million. Operating costs as a percentage of turnover came in at 24.7 percent (2016: 24.3 percent). The increase in operating costs was due to €7 million in (budgeted) extra costs related to the implementation of the strategy. These costs are related to the strengthening of the group organization, IT projects and the hiring of consultancy services. In addition, Accell Group took an extra charge of €6 million related to the reorganization and reduction of inventories in North America in the second half of 2017.

The operating result declined by 37.1 percent to €38.0 million (2016: €60.4 million). The decline is explained by the events in North America, which had a negative impact of €13.1 million, due to a weak operational performance and the aforementioned one-off charges related to the transformation of the local organization. The remaining part of the decline in operating result is explained by the lower added value and the extra costs associated with the implementation of the strategy. This resulted in an EBIT margin of 3.6 percent.

The financial expenses of €8.2 million recorded in 2017 were slightly lower than in the previous year. The extension of the group financing agreed on in March 2017 resulted in improved terms and reduced interest expenses. This was offset by the accelerated write-down of the financing costs of the previous refinancing arrangements and a reduced result from the exchange rate differences on positions in foreign currencies.

The tax rate was higher in 2017 due to the non-cash write-down of existing tax assets in North America (€3.8 million) and Finland (€1.9 million) and the non-capitalization of carry-forward losses in North America.

Net profit declined to €10.5 million in 2017 (2016: €32.3 million). This translates into net earnings per share of €0.40 (2016: €1.24). Excluding the one-off charges in North America (€10 million) and the write-down of tax assets (€5.7 million), earnings per share came in at €1.00.

Developments Per Segment

Net turnover in the bicycle segment was 3.5 percent higher compared to 2016, largely on the back of an increase in sales of e-bikes, and in particular the e-MTBs of the brands Haibike, Ghost and Lapierre. Accell Group noted strong growth in turnover of these bikes, especially in Europe. Sales of regular bikes declined compared to the previous year, both in sales volume and in turnover. Driven by this development, the share in turnover accounted for by e-bikes in this segment increased to 63 percent (2016: 55 percent).

Net turnover in the bicycle segment was 3.5 percent higher compared to 2016, largely on the back of an increase in sales of e-bikes, and in particular the e-MTBs of the brands Haibike, Ghost and Lapierre. Accell Group noted strong growth in turnover of these bikes, especially in Europe. Sales of regular bikes declined compared to the previous year, both in sales volume and in turnover. Driven by this development, the share in turnover accounted for by e-bikes in this segment increased to 63 percent (2016: 55 percent).

Partly due to the increased focus on sales of more expensive and high-grade (e-)bikes, the number of bicycles sold declined to 1,278,000 in 2017 (2016: 1,457,000). Particularly in North America, sales volumes of (regular) bikes showed a particularly strong decline compared to the previous year. The primary reason for this was the loss of sales volume and turnover from large multi-sports retail chains In case of any inconsistencies the Dutch version of this press release is leading. 5 as well as a slight decline in turnover from the traditional specialist retailers (IBDs) as a consequence of the revised distribution strategy. Accell Group was unable to fully offset this decline in sales volume and turnover through sales via other, new channels in 2017.

The segment result was negatively impacted primarily by the weak performance in North America and the transformation of the local organiz ation in that region. However, the continued growth in e-bikes and positive developments in Germany had a positive impact on the result. Excluding the poorer results in North America, the Bicycles segment result remained stable.

Net turnover in parts and accessories declined in 2017 due to the termination of the parts and accessories activities in North America in 2016. Organic net turnover growth in parts and accessories came in at 0.5 percent. The growth in turnover was booked primarily in Europe, partly driven by the organic growth of our own XLC brand.

The segment result of this trading activity increased. The higher share of our own XLC brand (in Europe) in turnover made a positive contribution to the segment result on the back of the improved utilization of procurement benefits.

Developments Per Region

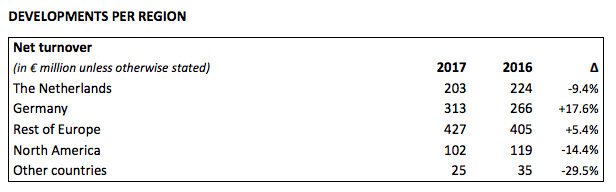

In the Netherlands, Accell Group booked lower turnover in both bicycles and parts and accessories. Koga was the only Dutch brand to record growth in 2017. Batavus and Sparta recorded lower turnover in both regular bikes and e-bikes, particularly in the first half of 2017. With the implementation of the refined strategy, a new margin structure and the introduction of a selective distribution system, Accell Group has taken a number of significant steps towards creating a level playing field for all dealers on the basis of which the relationship and cooperation with the specialist retailers can be improved.

In Germany, turnover was higher on the back of increased sales volumes in electric bikes. Both the sales of Haibike and Ghost e-MTBs and the sales of Winora’s traditional e-bikes were higher than in the previous year. Sales of regular bikes also declined in Germany. In addition to the higher sales of ebikes, turnover in parts and accessories was also higher than in 2016.

In the Rest of Europe, increased sales of e-MTBs resulted in higher turnover. The popularity of the eMTBs of our international brands Haibike, Lapierre and Ghost increased in virtually all European countries, and in particular in France, Austria and Spain. Sales of regular bikes declined in most countries. In virtually all European countries, turnover in parts and accessories was higher than in the previous year. Turnover in Scandinavia and Spain saw a particularly marked increase last year.

In North America, turnover declined. The lower turnover was primarily due to reduced sales via the multi-sports retail channel and the termination of the parts and accessories activities. Positive developments came in the form of higher turnover via new sales channels and growth in the sales of the Haibike, Raleigh and IZIP brands. In the IBD sales channel, turnover was slightly lower than in the previous year as a result of the change in distribution strategy in 2017. This was caused by a changing sales mix. Dealers bought fewer but more expensive bikes.

Turnover in Other countries was limited and declined due to the economic conditions in Turkey, especially in the first half of 2017. Turnover in Asian countries and Australia was more or less unchanged from 2016.

Financial Strength and Capital Efficiency

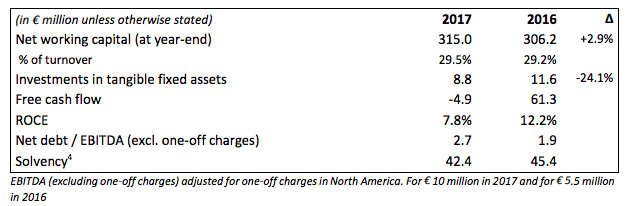

The net working capital came in at €315 million in 2017, 2.9 percent higher than in 2016. Inventories were up 3.7 percent at €334 million. Accounts receivable were €127 million, compared with €138 million in 2016. Accounts payable were lower than in the previous year, at €146 million.

Although working capital was up slightly compared to the previous year, the movements in working capital were positive. As such, the number of bicycles in stock fell by 8 percent (24,000) compared to the previous year. The fact that the value of inventories was higher in 2017 than in 2016 was due to the higher average cost price per bicycle, which was 11 percent higher than in the previous year. The higher cost price was due to the greater share of e-bikes in the inventories. The higher inventories are needed to make sure Accell Group can respond to the greater demand for these bicycles in the first quarter of 2018. In conjunction with these higher inventory of e-bikes, the value of inventories of components is also higher, because the company maintains higher inventories of e-bike components and components for more expensive bikes. In addition, accounts receivable were lower than in the previous year despite higher turnover in the fourth quarter. While Accell Group procured less, accounts payable per yearend 2017 were slightly below the level of 2016, due to the longer payment terms negotiated with suppliers.

Total net debt, comprising interest-bearing loans, bank credits and cash and cash equivalents, stood at €161 million at year-end 2017, up from €147 million at year-end 2016, largely due to movements in working capital. Excluding one-off charges, EBITDA declined by 22.5 percent to €59.1 million. This resulted in a net debt / EBITDA (excl. one-off charges) ratio of 2.7, a worsening compared to the previous year.

Shareholders’ equity stood at €299 million, which resulted in a solvency ratio of 42.4 percent (2016: 45.4 percent). The change in the shareholders’ equity of €20.1 million was largely due to the result for the period (+€10.5 million), dividend payments (-/- €6.7 million), the valuation of financial instruments (-/-€10.3 million) and currency exchange rate differences (-/-€13.5 million).

Developments After the Balance Sheet Date

Board changes Hielke Sybesma (CFO) decided after 23 years to leave the company as of 1 May 2018 and will step down from the Board of Directors as of 25 April. The search for a successor to Hielke Sybesma has started.

Jeroen Snijders Blok (COO) will resign from the Board of Directors at his own request as of 25 April 2018, while retaining his current activities and reporting directly to the CEO. The responsibility for the production sites has recently been transferred to Jeroen Both (CSCO). The Supervisory Board would like to thank Hielke and Jeroen for their years of involvement as members of the Board of Directors and is grateful for their contribution to the development of Accell Group for many years.

Jeroen Hubert has been appointed Chief Commercial Officer (CCO) as of March 1 2018. Jeroen reports to the CEO and is responsible for marketing, innovation, (e)commerce and retail/experience centers. He has previously gained extensive experience in the aforementioned areas at Pepsico, Friesland Campina, Wehkamp and Ikea.

Earnings Per Share and Dividend

Earnings per share based on the weighted average number of outstanding shares (year-end 26,101,222 shares) declined by 67 percent to €0.40 in 2017 (2016: €1.24). Earnings per share excluding one-off charges came in at €1.00. Due to the issuance of 399,871 shares for the payment of the stock dividend for the 2016 financial year, the correction factor for the earnings per share from previous years is 0.98476.

For the 2017 financial year, Accell Group shareholders will be asked to approve the payment of an optional dividend of €0.50 per share (2016: €0.72), to be paid out in cash or shares. The dividend proposal is related to the earnings per share excluding one-off charges, which puts the pay-out ratio at 50 percent. The pay-out ratio based on the reported earnings per share amounts to 124 percent. The expectations for the coming years as a result of the refined strategy and the incidental nature of the charges in 2017, underpin a dividend that is higher than the reported earnings per share. Based on the closing price at year-end 2017 (€23.43), the dividend return amounts to 2.1 percent.

Management Agenda and Outlook

Cycling will remain popular for mobility, recreational and sports purposes in the years to come. Accell Group expects to remain a leader in the market with it high-quality products and to be in a position to continue to add innovations to make cycling even more attractive for various purposes. This will be a key transitional year that will be dominated to a large extent by a reduction in complexity and centralization of management in areas such as (e-)commerce, innovation, supply chain, human resources and IT. This will accelerate the realization of a more efficient operational processes, will improve utilization of scale and synergy potential and strengthens the execution power in the various regions. In addition, Accell Group will actively seek increases in scale via acquisitions that fit the strategy.

For 2018, Accell Group expects to see an improvement in the results in North America on the back of the omni-channel strategy and the strong growth in the e-bike market. In Europe, they expect continued growth in turnover as a result of higher sales of e-bikes and high-end regular bikes. Based on this and barring unforeseen circumstances, Accell Group expects an increase in group turnover and a higher underlying operating result for 2018.