Vail Resorts Inc. reported that the company’s losses in the fourth quarter ended July 31 grew to $83.7 million, or $2.07 a share, from $57.1 million, or $2.07. Results were better than Wall Street’s consensus target of loss of $2.26.

Revenues gained 1.2 percent to $211.6 million from $209.1 million. Wall Street’s average target had been $213.2 million.

Vail Resorts statement elaborated on results for the fiscal year ending July 31, 2019.

Highlights

- Net income attributable to Vail Resorts, Inc. was $379.9 million for fiscal 2018, an increase of 80.4 percent compared to fiscal 2017, which was positively impacted by tax benefits as described in the operating results highlights below.

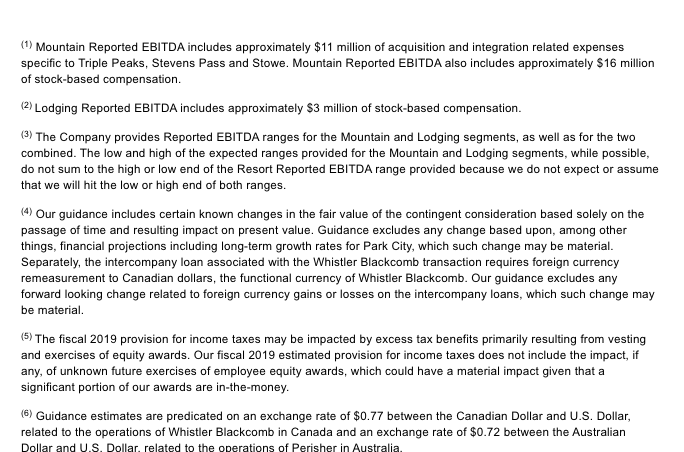

- Resort Reported EBITDA was $616.6 million for fiscal 2018, an increase of 3.9 percent compared to fiscal 2017. Fiscal 2018 Resort Reported EBITDA includes $10.2 million of acquisition and integration related expenses and $2.6 million of additional payroll taxes related to the CEO’s exercise of Stock Appreciation Rights (SARs).

- Season pass sales through September 23, 2018 for the upcoming 2018/2019 North American ski season increased approximately 25 percent in units and 15 percent in sales dollars as compared to the period in the prior year through September 24, 2017, including all military pass products in both periods. Pass sales exclude Stevens Pass and Triple Peaks pass sales in both periods and are adjusted to eliminate the impact of foreign currency by applying current period exchange rates to the prior period for Whistler Blackcomb pass sales.

The company issued its fiscal 2019 guidance range and expects Resort Reported EBITDA to be between $718 million and $750 million, including approximately $11 million of acquisition and integration related expenses for the previously announced acquisitions of Stevens Pass, Triple Peaks and Stowe.

Commenting on the company’s fiscal 2018 results, Rob Katz, chief executive officer, said, “We are very pleased to complete fiscal 2018 with Resort Reported EBITDA growth from the prior year, despite the very challenging conditions in the western U.S. this past winter. This year’s results highlight the positive impact of our expanding geographic diversification, the stability provided by our growing season pass program and the success of our guest-focused marketing efforts. Our western U.S. destination resorts experienced modest visitation declines compared to the prior year due to the historically poor conditions, particularly for the first half of the season. However, revenue at our western U.S. resorts was in line with prior year performance due to season pass sales and yield growth. Whistler Blackcomb had another record-breaking year, growing from an exceptional fiscal 2017 as the resort benefited from excellent conditions throughout the season, currency favorability that attracted guests from the U.S. and around the world and the first season of full integration with Vail Resorts. At Perisher, fiscal 2018 results were strong with double-digit revenue and EBITDA growth compared to the prior year, driven by a strong finish to the 2017 Australian ski season and a strong start to the current 2018 Australian ski season, supported by pass sales momentum, which was positively impacted in part by the new pass partnership with Hakuba Valley in Japan.”

Katz added, “With a strong base of high-end consumers, we are continuing to leverage our growing network of resorts and sophisticated marketing and yield strategies to drive guest spending across our Mountain segment. For fiscal 2018, total Mountain net revenue increased 6.9 percent to approximately $1.7 billion. Total skier visits, including results from Stowe in fiscal 2018, increased 2.5 percent, primarily as a result of the inclusion of Stowe, which was acquired in June 2017, offset by the poor conditions at our western U.S. resorts during the first half of the 2017/2018 ski season. Total Effective Ticket Price (“ETP”) increased 5.0 percent, driven by season pass and lift ticket price increases across our resorts, as well as lower visitation per pass. Our ancillary businesses also experienced growth, with ski school, dining and retail/rental revenue up 6.8 percent, 7.2 percent and 1.0 percent, respectively, compared to the prior year, primarily driven by the addition of results at Stowe. Our U.S. Epic Discovery business continues to grow and generate strong financial returns on the capital we invested. However, Epic Discovery has not yet reached full maturity on profitability as quickly as we had originally planned. With each summer season, we continue to learn more about our guests, improve operational consistency and refine our pricing, product and promotion strategy to take advantage of the high levels of summer visitation which already exists at these resort locations.”

Regarding Lodging, Katz said, “Fiscal 2018 Lodging results were impacted by the less favorable conditions in Colorado and Utah compared to the prior year. Revenue (excluding payroll cost reimbursements) increased 2.4 percent and revenue per available room (“RevPAR”) increased 2.4 percent compared to the prior year, while Lodging Reported EBITDA declined 7.7 percent compared to fiscal 2017, which included a one-time association fee benefit in the prior year.”

Turning to Real Estate, Katz commented, “We generated $0.1 million of Net Real Estate Cash Flow in fiscal 2018. During fiscal 2018, we closed on the sale of a land parcel at Keystone for $3.0 million and contributed $4.3 million to the Town of Vail related to a parking development. As of July 31, 2018, we had approximately $99.4 million of real estate held for sale and investment associated with land parcels at our resorts.”

Katz continued, “Our balance sheet continues to be very strong. We ended the fiscal year with $178.1 million of cash on hand, $130.0 million of borrowings under the revolver portion of our senior credit facility and total long-term debt, net (including long-term debt due within one year) of approximately $1.3 billion. As of July 31, 2018, we had available borrowing capacity under the revolver component of our Vail Holdings, Inc. credit facility of $185.1 million. In addition, we had $164.6 million available under the revolver component of our Whistler Blackcomb credit facility. Our Net Debt was 1.8 times trailing twelve months Total Reported EBITDA, which includes $334.5 million of long-term capital lease obligations associated with the Canyons transaction. On August 15, 2018, the company entered into an amendment agreement to amend and restate in its entirety the senior credit facility. The amended agreement provides for a revolving loan facility in an aggregate principal amount of $400.0 million and a term loan facility in an aggregate principal amount of $950.0 million, increased from the previous term loan facility of $684.4 million as of July 31, 2018. The company borrowed $70.0 million on August 15, 2018, primarily to fund the Stevens Pass acquisition and on September 27, 2018, the company borrowed an additional $195.6 million, primarily to fund the Triple Peaks acquisition. I am also very pleased to announce that our Board of Directors has declared a quarterly cash dividend on Vail Resorts’ common stock. The quarterly dividend will be $1.47 per share of common stock and will be payable on October 26, 2018 to shareholders of record on October 9, 2018.”

Operating Results

Mountain Segment

- Fiscal 2018 results reflect a full year of Whistler Blackcomb operations, as compared to fiscal 2017 results, which include Whistler Blackcomb operations from the date of acquisition, October 17, 2016, through July 31, 2017.

- Total skier visits for fiscal 2018 increased to approximately 12.3 million, an increase of 2.5 percent compared to the prior fiscal year, which includes incremental skier visits from Stowe.

- Total lift revenue increased $62.0 million, or 7.6 percent, compared to the prior fiscal year, primarily due to an increase in pass revenue and incremental revenue from Stowe.

- Ski school revenue increased $12.2 million, or 6.8 percent, primarily as a result of increased revenue at Whistler Blackcomb and Park City, as well as incremental revenue from Stowe.

- Dining revenue increased $10.8 million, or 7.2 percent, primarily as a result of incremental revenue from Stowe and increased revenue from Whistler Blackcomb, partially offset by lower revenue at our western U.S. resorts.

- Retail/rental revenue increased $3.0 million, or 1.0 percent, of which rental revenue increased $2.9 million, or 3.2 percent, and retail revenue was relatively flat. Both rental and retail revenue were positively impacted by an increase in revenue at Whistler Blackcomb and incremental revenue from Stowe, partially offset by decreased revenue at stores proximate to our western U.S. resorts and other city stores.

- Operating expense for Fiscal 2018 increased $85.5 million, or 8.2 percent, which was primarily attributable to the inclusion of Stowe operations and incremental operating expenses from Whistler Blackcomb as a result of reflecting a full year of operations for fiscal 2018.

- Mountain Reported EBITDA increased $25.3 million, or 4.5 percent, which includes $15.7 million of stock-based compensation expense and $10.2 million of acquisition and integration related expenses for fiscal 2018, compared to $15.0 million and $10.8 million for fiscal 2017, respectively.

Lodging Segment

- Lodging segment net revenue (excluding payroll cost reimbursements) increased $6.5 million, or 2.4 percent.

- Occupancy increased 1.3 percentage points and Average Daily Rate (“ADR”) decreased 0.6 percent at the company’s owned hotels and managed condominiums compared to the prior fiscal year.

- Lodging Reported EBITDA for Fiscal 2018 decreased $2.1 million, or 7.7 percent compared to fiscal 2017, which included a one-time benefit for association fees with respect to a lodging property at Park City in the prior year.

- Lodging Reported EBITDA includes $3.2 million of stock-based compensation expense for both fiscal 2018 and fiscal 2017.

Resort – Combination of Mountain and Lodging Segments

- Resort net revenue was $2,007.6 million for fiscal 2018, an increase of $117.3 million, or 6.2 percent, compared to fiscal 2017, primarily attributable to growth at Whistler Blackcomb, strong North American pass sales growth for the 2017/2018 North American ski season and the incremental operations of Stowe.

- Resort Reported EBITDA was $616.6 million for fiscal 2018, an increase of $23.2 million, or 3.9 percent, compared to fiscal 2017. Results included $10.2 million of acquisition and integration related expenses compared to $10.8 million of acquisition and integration related expenses in the prior fiscal year. Additionally, fiscal 2018 results included $2.6 million of additional payroll taxes related to the CEO’s exercise of SARs.

Real Estate Segment

- Real Estate segment net revenue decreased $12.9 million, or 76.4 percent, as compared to the prior fiscal year, primarily due to the company selling out of condominium units as of July 31, 2017.

- Real Estate segment operating expense for fiscal 2018 includes the recognition of a $5.5 million benefit of non-cash income in the current period related to a legal settlement in fiscal 2015 for which cash proceeds were received and established as a liability for estimated future remediation costs of a construction development. All known items have been remediated, and, based on continued monitoring, the company has concluded that the need for further remediation is remote. Additionally, Real Estate segment operating expense for the prior year included the $4.3 million one-time charge related to the resolution of the company’s financial contribution to the new Town of Vail public parking structure, which was paid during fiscal 2018.

- Net Real Estate Cash Flow for fiscal 2018 was $0.1 million, which includes the $4.3 million contribution to the Town of Vail parking structure noted above, a decrease of $18.3 million compared to the prior fiscal year.

- Real Estate Reported EBITDA was $1.0 million, an increase of $1.4 million as compared to the prior year.

Total Performance

- Total net revenue increased $104.3 million, or 5.5 percent, to $2,011.6 million.

- Net income attributable to Vail Resorts, Inc. was $379.9 million, or $9.13 per diluted share, compared to $210.6 million, or $5.22 per diluted share, in the prior fiscal year. Net income attributable to Vail Resorts, Inc. for fiscal 2018 included a tax benefit of approximately $71.1 million (or $1.71 earnings per diluted share) related to employee exercises of equity awards (primarily related to the CEO’s exercise of SARs) which, beginning August 1, 2017, is recorded in net income as a result of the adoption of revised accounting guidance related to employee stock compensation. Additionally, included in net income attributable to Vail Resorts, Inc. for fiscal 2018 was a one-time, provisional net tax benefit related to U.S. tax reform legislation, estimated to be approximately $61.0 million, or $1.47 per diluted share, which was recognized as a discrete item and recorded within benefit (provision) for income taxes during fiscal 2018. The above-mentioned accounting impacts related to U.S. tax reform legislation (“U.S. Tax Reform”) are provisional, based on currently available information and technical guidance on the interpretation of the new law.

Return of Capital

The company declared a quarterly cash dividend of $1.47 per share of Vail Resorts common stock that will be payable on October 26, 2018, to shareholders of record on October 9, 2018. Additionally, a Canadian dollar equivalent dividend on the exchangeable shares of Whistler Blackcomb will be payable on October 26, 2018, to exchangeable shareholders of record on October 9, 2018. The exchangeable shares were issued to certain Canadian persons in connection with our acquisition of Whistler Blackcomb.

Acquisitions

On August 15, 2018, the company announced the closing of the Stevens Pass acquisition. The final purchase price, after adjustments, was approximately $64.0 million.

On September 27, 2018, the company announced the closing of the Triple Peaks acquisition. Triple Peaks is the parent company of Okemo Mountain Resort in Vermont, Mount Sunapee Resort in New Hampshire and Crested Butte Mountain Resort in Colorado. The company purchased Triple Peaks for a final purchase price of approximately $74 million after adjustments for certain agreed-upon terms. As part of the transaction and with funds provided by Vail Resorts, Triple Peaks paid off $155 million in leases that all three resorts had with Ski Resort Holdings, LLC, an affiliate of Oz Real Estate. The 2018/2019 Epic Pass, Epic Local Pass and Military Epic Pass now include unlimited and unrestricted access to Okemo Mountain Resort, Mount Sunapee Resort and Crested Butte Mountain Resort; the Epic 7 Day and the Epic 4 Day now offer up to seven and four unrestricted days, respectively.

Season Pass Sales

Commenting on season pass sales, Katz said, “We are very pleased with our season pass sales to date. Through September 23, 2018, North American ski season pass sales increased approximately 25 percent in units and 15 percent in sales dollars as compared to the period in the prior year through September 24, 2017, including all military pass sales in both periods and excluding pass sales from Stevens Pass and Triple Peaks in both periods and adjusted to eliminate the impact of foreign currency by applying current period exchange rates to the prior period for Whistler Blackcomb pass sales. Growth in our total season pass sales dollars was lower than our unit growth given the inclusion of the new Military Epic Pass which is available at a substantial discount to our Epic Pass. The average price increase on all non-military passes was approximately 4.5 percent. Excluding sales of military passes to new purchasers who were not pass holders last year, season pass sales increased approximately 9 percent in units and 12 percent in sales dollars over the comparable period in 2017.”

Katz continued, “We experienced strong growth in our season pass sales across nearly all products and geographies, including continued strong growth in destination markets, which drove over half of the unit growth. We also saw very strong growth in the local Whistler Blackcomb market and continued growth in the Colorado and Tahoe markets. We believe this growth continues to be driven by our increasingly sophisticated and data-driven targeted marketing efforts to move destination guests into our season pass products as well as the strategic long-term pass partnerships and acquisitions we have announced that continue to expand our resort network and make the network incrementally more compelling to skiers worldwide. Our growth was also positively impacted by the significant success of sales of our new Military Epic Pass. The vast majority of Military Epic Passes were sold to guests that were not previously season pass purchasers, and over half of the Military Epic Pass purchasers were not previously in our guest database. While the Military Epic Pass has a price that is much lower than our other season pass products, we are seeing significant incremental revenue for the program that far exceeds any loss of revenue from prior year pass holders who purchased a Military Epic Pass for this year. Furthermore, we are helping to introduce our sport to, and create much higher engagement for, the men and women who have served their countries in the armed forces and their immediate families. While in December 2017 our reported season pass growth rates were materially below the rates reported in September 2017; we expect our December 2018 season pass growth rates to be relatively consistent with our September 2018 growth rates.”

Katz concluded, “Our Epic Australia Pass sales are off to a very strong start with growth of approximately 20 percent in units and approximately 23 percent in sales dollars through September 23, 2018 compared to the prior year period ending September 24, 2017. The Epic Australia Pass continues to be a very compelling product for our Australian guests who can ski locally at Perisher, experience our growing network in North America and, for the first time, ski at Hakuba Valley in Japan through our new long-term partnership. Pass sales will continue through the Australian off-season leading up to the 2019 season.”

Guidance

Commenting on guidance for fiscal 2019, Katz said, “Net income attributable to Vail Resorts, Inc. is expected to be between $288 million and $335 million in fiscal 2019. Our guidance includes an estimated benefit between $32 million and $40 million from the reduction of our U.S. federal tax rate from 35 percent to 21 percent as a result of the U.S. Tax Reform. We estimate Resort Reported EBITDA for fiscal 2019 will be between $718 million and $750 million. Our Resort Reported EBITDA guidance includes the operating results for Stevens Pass, Okemo, Mount Sunapee and Crested Butte from the date of acquisition and also includes approximately $11 million of anticipated acquisition and integration related expenses. Apart from our normal business drivers, our guidance for fiscal 2019 includes the following additional assumptions: (i) a full rebound in our performance in our second fiscal quarter, as compared to fiscal 2018, from assumed normal conditions throughout the period; (ii) a negative impact to our fiscal 2019 third quarter from the late Easter holiday (which is on April 21, 2019); (iii) $15 million of incremental expense related to above normal increases in labor costs, due to increasing our minimum wage by over $1 per hour at most resorts and other significant investments in compensation, all implemented due to both local market wage pressure and the benefits the company received from U.S. Tax Reform and (iv) a $6 million negative Resort Reported EBITDA impact from assumed lower rates for the Australian and Canadian dollars versus the average rates in fiscal 2018. We expect Resort EBITDA Margin to be approximately 31.5 percent in fiscal 2019 using the midpoint of the guidance range. This is an estimated 80 basis point increase over fiscal 2018. We estimate fiscal 2019 Real Estate Reported EBITDA to be between negative $3 million and $3 million. Fiscal 2019 guidance does not include any payroll tax impacts or income tax benefits related to the potential exercise of CEO stock appreciation awards.”

All of these estimates are predicated on the assumption of normal weather conditions throughout the ski season and an exchange rate of $0.77 between the Canadian Dollar and U.S. Dollar, related to the operations of Whistler Blackcomb in Canada and an exchange rate of $0.72 between the Australian dollar and U.S. dollar, related to the operations of Perisher in Australia.

The following table reflects the forecasted guidance range for the company’s fiscal year ending July 31, 2019, for Reported EBITDA (after stock-based compensation expense) and reconciles such Reported EBITDA guidance to net income attributable to Vail Resorts, Inc. guidance for fiscal 2019.

Photo courtesy Vail Resorts