PwC has released its M&A Outlook for 2025, signaling that the landscape is rip for U.S. mergers and acquisitions activity is poised to gain momentum in 2025 due to “declining interest rates, large amounts of dry powder, the need for business model reinvention, and shifting regulatory priorities.”

“Despite a clearer economic and policy outlook, dealmakers will need to navigate a complex environment shaped by the reversal of certain Biden-era reforms, geopolitical challenges and slowing macroeconomic growth. The second Trump administration is signaling shifts in trade, tariffs and security policies. Dealmakers who succeed will be those who prioritize agility and strategic focus,” the company said in its report summary.

Regulatory Changes, Geopolitics Shaking Up M&A

PwC said the U.S. M&A recovery will likely accelerate in 2025 as dealmakers digest the implications of a new regulatory regime, the Fed’s interest rate pivot and other macroeconomic and geopolitical factors. However, there was a note of caution about the incoming Trump administration’s intention to shake up the status quo, including nominating regulators with non-traditional backgrounds.

“It has telegraphed a willingness to significantly alter U.S. global trade and security policies, especially through tariffs,” PwC wrote. As a result, the firm believes the domestic and international dealmaking environment could be extremely volatile.

“We expect some industries, such as oil and gas, to benefit from significant deregulation. Others, such as Big Tech, may be scrutinized more closely. Cross-border deals will remain exposed to geopolitical uncertainty, with trade wars, tariffs and national security concerns complicating M&A strategy and execution,” the company wrote.

Caution over the past year was said to be “understandable and consistent with similar election cycles,” PwC said but the company still expects the recovery to pick up in 2025 now that some sources of uncertainty have been resolved. They cited the election, the Federal Reserve’s pivot and the “direction, if not the degree, of rate cuts is more certain.”

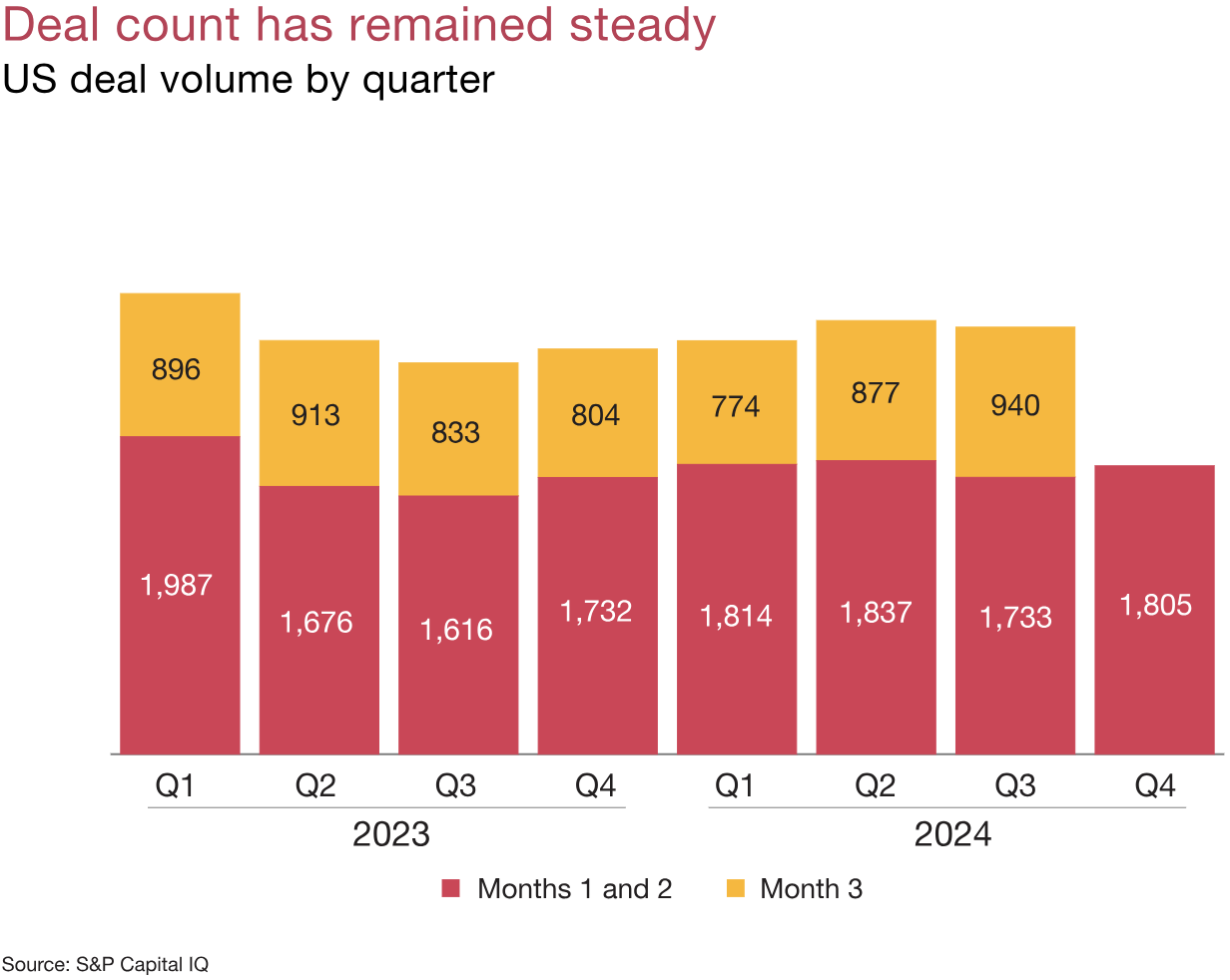

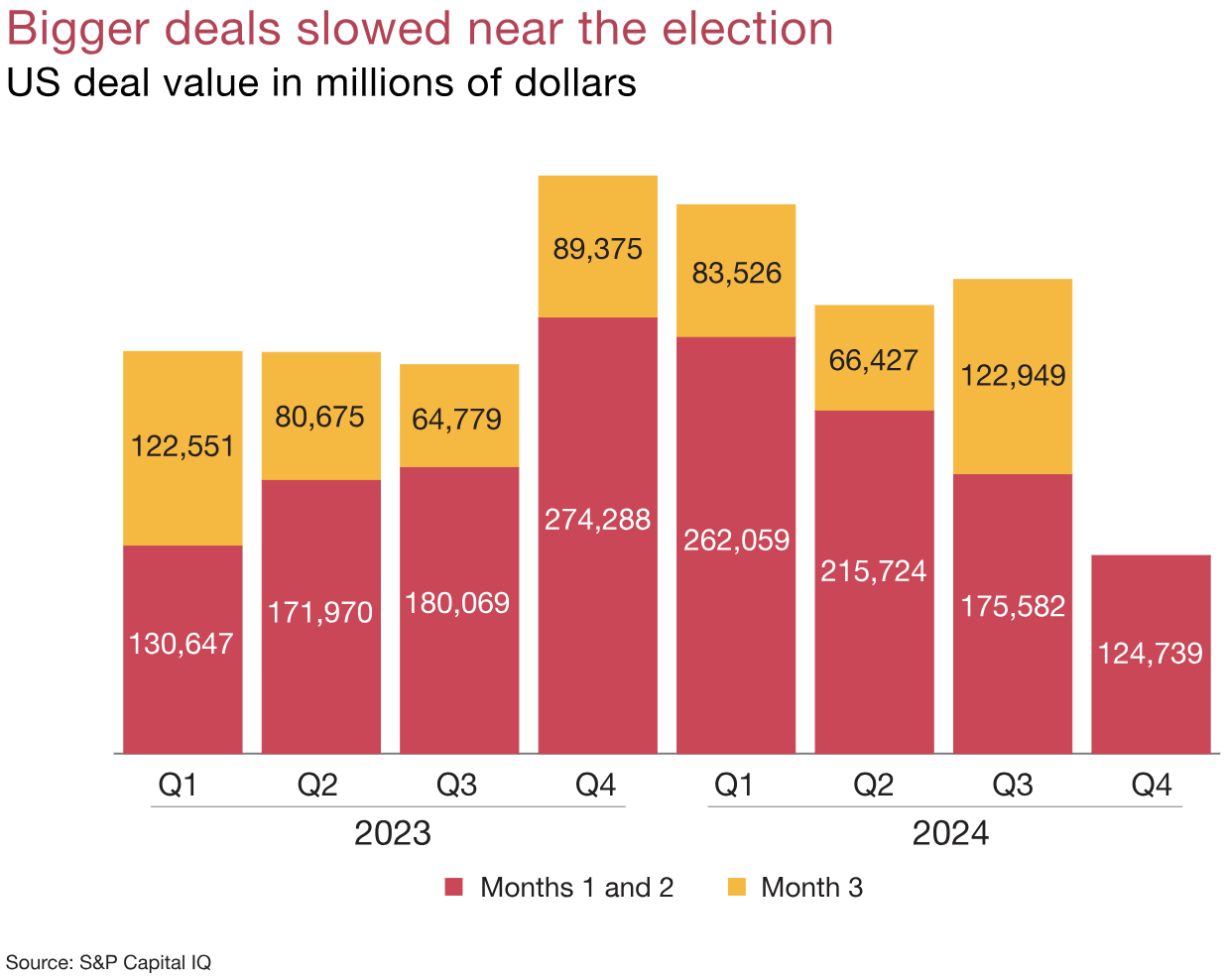

PwC wrote, “Finally, a soft landing remains our baseline and M&A volume historically accelerates in non-recession years, according to PwC analysis of S&P Global data. There were 9,780 deals for $1.05 trillion in the first 11 months of 2024. Both volume and value were up slightly compared to the same period a year ago, when there were 9,653 deals for $1.02 trillion. Deal volume has been impacted over the past couple years due in part to a private equity (PE) exit drought.”

PE Exits, IPO Markets Could Boost Deal Activity

PwC’s analysis of PitchBook Data, Inc., found that several thousand PE exits were delayed over the past two years. The company said some of these exits are more likely to happen now that more certainty has returned to the market — meaning more potential targets for corporate acquirers.

“Some of those portfolio companies may be mature enough that they consider an IPO exit strategy. The overall IPO market continued a gradual comeback this year, with proceeds raised nearly 50% higher than in 2023 and nearly four times the amount raised in 2022,” the company wrote.

“Activity was broad-based, with notable participation from industries including technology, life sciences, consumer markets and financial services. Stock prices of this year’s traditional IPOs were up nearly 29 percent, outperforming the S&P 500, which rose by 26 percent over the year as of November 29 — further highlighting the strength and investor interest in new offerings,” PwC said.

Looking ahead, PwC said today’s corporate development leaders operate in an ecosystem that’s being transformed by long-term mega trends, including radical technological advancements and significant demographic and political realignments.

Companies that don’t address these challenges could face the ire of activist investors and, eventually, obsolete business models.

Earnings per share (EPS) growth expectations have risen over the past year. PwC believes that many companies will turn to strategic M&A to fuel this expansion in addition to traditional organic growth.

This new environment will favor flexible dealmakers capable of strategic scenario planning around regulatory and geopolitical exposures.

Companies should prioritize simplifying their portfolios and having the capability to execute a focused value creation strategy amid a slowing economy.

“We see three themes that will shape dealmaking in 2025: the need for companies to justify their valuations, an inflection point for regulatory activity, and the impact of geopolitical unrest on cross-border deals,” PwC wrote.

Justifying Valuations

Businesses probably shouldn’t count on the macroeconomy alone to achieve their growth aspirations in 2025. After exiting a profit recession last year, strong corporate earnings contributed to stock prices reaching record highs in 2024. Projected profit estimates have risen in lockstep, but they may be overly optimistic in a slowing economy.

The S&P 500 in late November was trading at 22.5X estimates of next year’s earnings, according to a PwC analysis of data from S&P and FactSet. That’s 40.1 percent higher than the average over the last 20 years. Meanwhile, PwC anticipates annual real GDP will have shown growth at 2.7 percent in 2024, but then moderate to 2.1 percent in 2025.

Cost management is another reason for concern over existing valuations. Inflation, while greatly reduced, is still higher than the Fed’s preferred 2 percent mark. That eats into company margins, as does a higher cost of capital. While short-term interest rates are dropping, they are still elevated compared to the past 15 years, and we don’t expect them to drop to the ultralow rates of the previous era. Increased tariffs and deportation efforts are important variables, as they could boost inflation — leading to the Fed raising interest rates again.

AI spending also factors into our valuation calculus. Despite some headwinds, $1 billion-plus deals — involving AI, cybersecurity, energy transition, insurance rollups and software targets — are being announced at one of the fastest paces in the last decade. Companies are pouring billions of dollars into AI with the expectation that it will eventually boost cost and revenue synergies. But not many companies are recognizing meaningful returns on AI yet. In the meantime, the increased spending may pressure the valuations of some companies.

Inorganic strategy will be key to closing this gap. Acquisitions can provide access to new markets, capabilities and product lines. They also contribute to cost synergies that make companies more efficient. Further, divestitures are a strategic way to rebalance underperforming portfolios and generate capital that can be used to reinvest in core offerings.

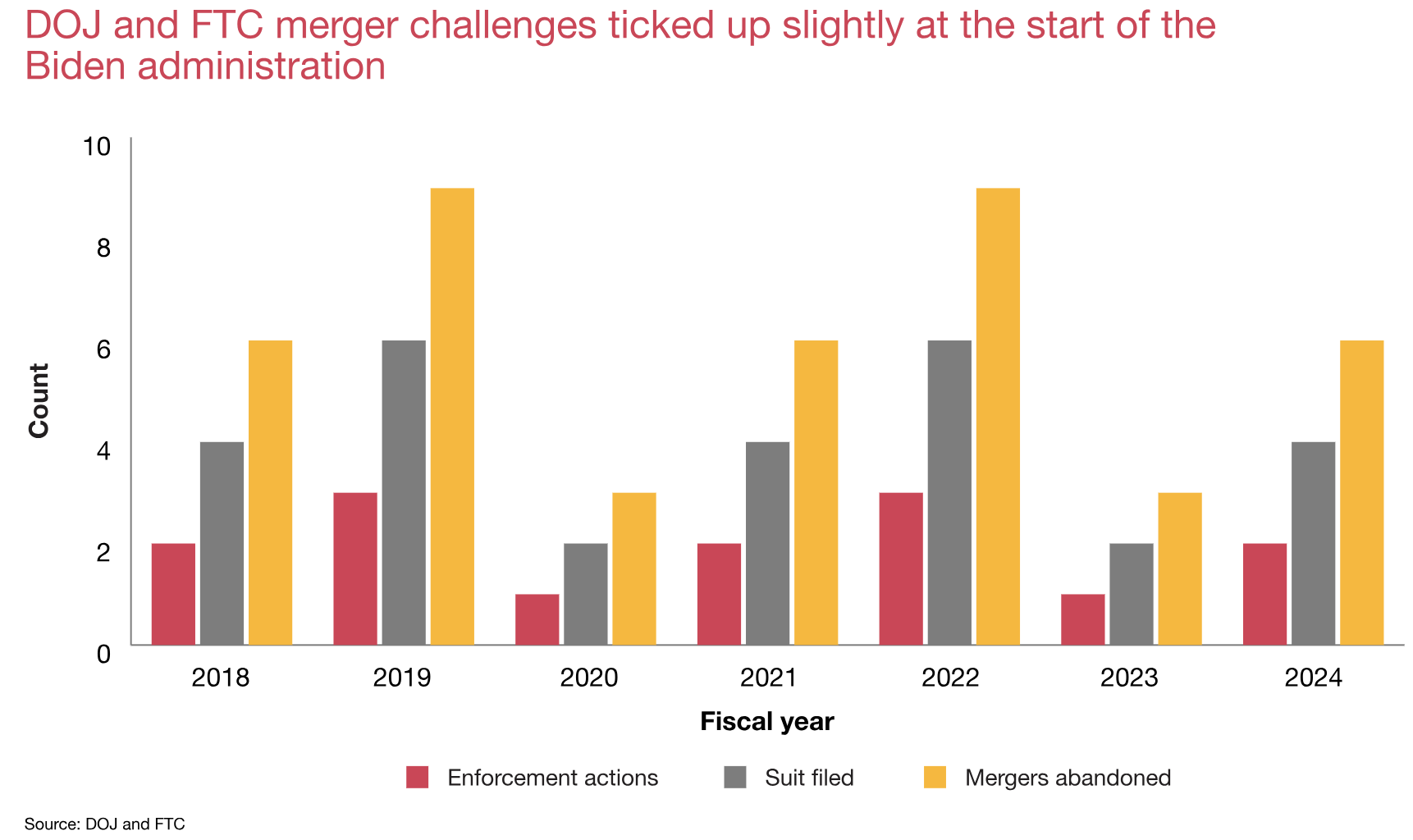

Regulatory Inflection Point

This is a critical juncture for regulation. While the second Trump administration is expected to shift toward deregulation, we don’t believe the federal government will completely return to the broadly laissez faire approach that reigned from the early 1980s through 2016. Instead, it will likely consolidate a new regulatory consensus that began under Biden and the first Trump term.

President-elect Trump broke with decades of a rough consensus that favored free trade and deregulation — especially regarding China. The Biden administration kept pressure on China while also ratcheting up domestic antitrust regulation.

The future of one such example is murkier after President-elect Trump’s victory: The Federal Trade Commission and Department of Justice in October finalized changes to the longstanding Hart-Scott-Rodino Act premerger notification form. The changes, which take effect in February 2025, reflect greater regulatory interest in serial acquirers like PE firms. Serial acquirers will have to disclose information on all acquisitions in the past five years with more than $10 million in assets and net sales, as well as board information to identify potential interlocking directorates.

The Inflation Reduction Act also faces a turning point in 2025. Renewables and the clean energy sectors could face stricter regulations, limits on new incentives and higher tariffs. While a full repeal is unlikely, and would require action from Congress, the Trump administration could slow the flow of unspent funds or direct how proposed regulations are finalized.

This will be a year for significant tax legislation, with key 2017 Tax Cuts and Jobs Act (TCJA) individual provisions set to expire at the end of 2025 and several significant business tax provisions set to change. A Republican sweep allows for the use of “budget reconciliation” procedures to enact tax legislation in 2025 with only Republican votes (which is how the TCJA was enacted in 2017). But narrow Republican margins in both the House and Senate could make it difficult to enact all of President-elect Trump’s campaign proposals. Reaching an agreement on how to address expiring TCJA tax provisions and campaign tax and trade proposals could delay action on a reconciliation tax bill until late 2025.

Federal spending levels will be another policy topic to watch, as will some types of potential antitrust enforcement. Even with Republicans in charge, big tech megadeals that impact tens of thousands of domestic jobs and M&A involving strategic foreign competitors will likely continue to face bipartisan scrutiny.

M&A activity tends to increase during presidential inauguration years in favorable economic times, according to PwC analysis of S&P Global data. Excluding recessions, US M&A volume grew a median of 10% year-over-year during the first year of a new administration since 1992.

However, the extent to which the incoming administration embraces tariffs and immigration deportation initiatives will be critical. These policies could have a huge impact on everything from supply chains to further interest rate cuts. Trump’s policies, including those on tariffs, also will impact IPO markets. While PwC expects activity to pick up by mid-2025, the recovery may be more measured than in previous “open window” periods, as companies wait for additional stability in central bank policies and broader economic conditions.

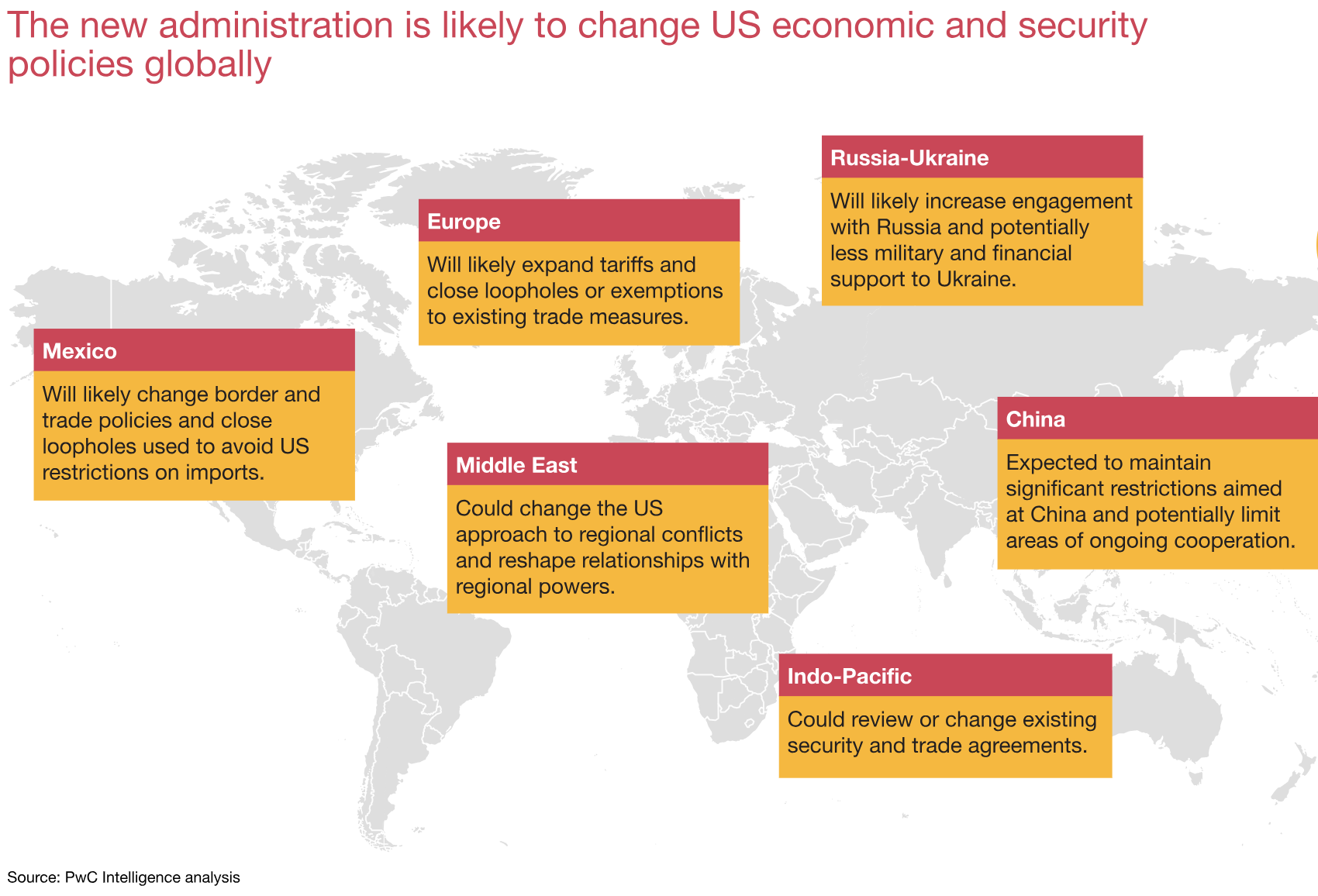

Geopolitical Landscape

According to an October 2024 PwC Pulse Survey, 68 percent of executives see geopolitical uncertainty as a risk to their company. The global order is in transition due to wars in Europe and the Middle East, continuing U.S.-China tensions and populist movements worldwide. Economic nationalism makes trade tensions more likely and trade agreements harder to negotiate. Washington will likely continue to elevate its scrutiny of Chinese influence over U.S. national security. President-elect Trump also has been supportive of imposing additional tariffs on foreign competitors.

While the specifics aren’t yet clear, tariffs could have a major impact on cross-border deals. Three quarters (75 percent) of executives in PwC’s October 2024 Pulse Survey said that a 10 percent universal tariff on imports would significantly hinder their growth. Tariffs could stall deals in some industries heavily reliant on imports but also could unlock new values. For instance, a US-centric business might be able to partially offset tariffs by exporting to those same countries. Or a US-centric business might command a higher valuation than a company with more international operations.

Military conflict can directly threaten corporate infrastructure, supply chains and market access. Geopolitical instability also has two indirect, but important, implications for M&A. First, it weakens executive confidence, which is a key indicator of potential dealmaking. Global strife also impacts financing costs as credit spreads increase — making it harder to fund deals.

The Bottom Line

“The dealmaking environment was in a mild recovery during most of 2024,” PwC concluded. “That recovery slowed in the run-up to the election consistent with past cycles. Some sources of uncertainty have now been answered. Dry powder is plentiful and there’s a backlog in the M&A pipeline. We believe the conditions are set for at least a moderate recovery and, assuming no external shocks, potentially much more than that.”

To learn more about PwC, go here.

Charts courtesy PwC