PVH Corp, the parent of Speedo and Izod, reported fourth-quarter earnings per share on a non-GAAP basis increased 23 percent to $1.76,

including a 10 negative impact related to foreign currency exchange

rates.

Earnings per share on a non-GAAP basis was $1.43 in the prior years fourth quarter.

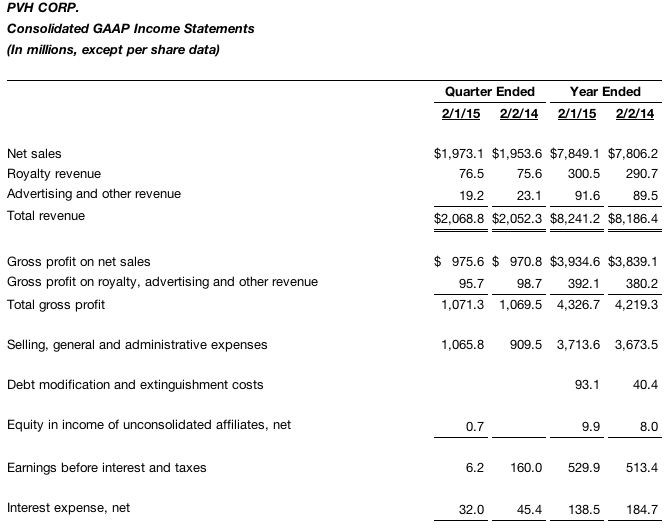

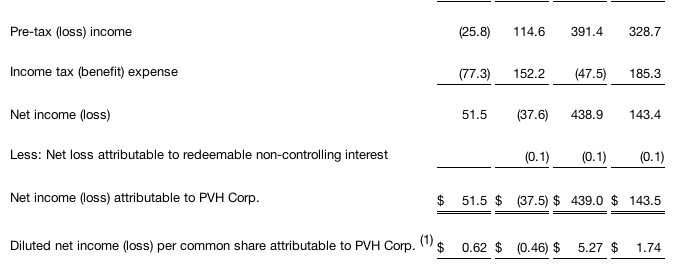

GAAP earnings per share was $0.62 compared to prior years fourth quarter loss per share of 46 cents a share.

Revenue increased 5 percent on a constant currency basis (increased 1 percent on a GAAP basis) over the prior years fourth quarter revenue of $2.05 billion. Revenue changes by business from the prior year period included (i) a 6 percent increase in the Calvin Klein business on a constant currency basis (2 percent increase on a GAAP basis); (ii) a 9 percent increase in the Tommy Hilfiger business on a constant currency basis (2 percent increase on a GAAP basis); and (iii) a 3 percent decrease in the Heritage Brands business.

CEO Comments:

Commenting on these results, Emanuel Chirico, chairman and chief executive officer, noted, “Overall, we are pleased with our fourth quarter results, which matched the top end of our earnings guidance, despite the highly challenging market environment and foreign currency headwinds. The Calvin Klein and Tommy Hilfiger businesses delivered improved year over year results, driven by the strength of their global consumer appeal. 2014 was a year of action for PVH, as we followed through with the investments initiated in 2013, which centered on our people, products, infrastructure, supply chain and distribution. We also announced the exit of our Izod retail business by the end of 2015 to focus on our higher margin businesses.”

Chirico continued, Looking ahead to 2015, we are taking a prudent approach to planning our business. The strength of the U.S. dollar relative to other major currencies in which we conduct business and the volatile global macroeconomic environment is expected to have a significant negative impact on our 2015 results. Nonetheless, we expect that our global lifestyle brands, Calvin Klein and Tommy Hilfiger, will continue to demonstrate strong underlying performance globally.”

Chirico concluded, “We remain committed to maximizing the potential of our businesses and believe the strength of our brands, together with the strategic investments made during 2013 and 2014, along with our strong balance sheet and continued debt repayment, will position us to deliver long term global growth and stockholder value.”

Fourth Quarter Business Review:

Calvin Klein

Revenue in the Calvin Klein business for the quarter increased 6 percent on a constant currency basis (increased 2 percent on a GAAP basis) from $688 million in the prior years fourth quarter. Calvin Klein North America revenue increased 13 percent, driven by growth in the wholesale businesses, coupled with square footage expansion in company-operated retail stores. The underwear business experienced strong momentum in the department store channel and helped fuel the overall growth in the wholesale business. North America retail comparable store sales were relatively flat as a result of the highly promotional retail environment during the holiday period. Calvin Klein International revenue decreased 2 percent on a constant currency basis (decreased 8 percent on a GAAP basis) compared to the prior year. Calvin Klein International retail comparable store sales declined 7 percent, as anticipated, largely due to a decrease in Asia resulting from the timing of the Chinese New Year, as the fourth quarter of fiscal 2014 did not include a Chinese New Year, while the fourth quarter of fiscal 2013 did.

Earnings before interest and taxes on a non-GAAP basis for the quarter increased to $91 million, including a $3 million negative impact due to foreign currency exchange rate changes, from $86 million in the prior years fourth quarter. The earnings increase was driven in large part by the revenue increase in North America, combined with an increase in gross margin in the international business, particularly in Europe.

GAAP earnings before interest and taxes was $74 million compared to $23 million in the prior years fourth quarter. The increase was principally driven by a reduction in integration and restructuring costs incurred during the fourth quarter of 2014 compared to the fourth quarter of 2013, combined with the increase in non-GAAP earnings discussed above.

Tommy Hilfiger

Revenue in the Tommy Hilfiger business for the quarter increased 9 percent on a constant currency basis (increased 2 percent on a GAAP basis) from $902 million in the prior year period. Tommy Hilfiger North America revenue increased 9 percent, principally due to a double-digit percentage increase in the wholesale business that was attributable, in part, to a shift in timing of shipments into the fourth quarter of 2014 from the third quarter, combined with square footage expansion in company-operated retail stores. North America retail comparable store sales were relatively flat as a result of the highly promotional retail environment during the holiday period. Tommy Hilfiger International revenue increased 9 percent on a constant currency basis (decreased 4 percent on a GAAP basis). Europe revenue growth was driven by a 6 percent comparable store sales increase, square footage expansion in company-operated stores and a mid-single digit percentage revenue increase in the wholesale business.

Earnings before interest and taxes was $121 million on a non-GAAP basis, including a $9 million negative impact due to foreign currency exchange rate changes, compared to $118 million in the prior years fourth quarter. The increase was principally attributable to the revenue increase mentioned above.

On a GAAP basis, earnings before interest and taxes was relatively flat compared to the prior years fourth quarter of $118 million, as the non-GAAP earnings increase discussed above was mostly offset by the costs related to the companys initiative to exit a discontinued product line in Japan.

Heritage Brands (Van Heusen, Izod, Arrow, Speedo, Warner's and Olga.)

Revenue for the Heritage Brands business for the quarter decreased 3 percent from $462 million in the prior year period. This decrease was principally driven by a 5 percent decrease in the wholesale business attributable to poor performance in the companys dress shirt business. The decline in the dress shirt business was primarily driven by an overall decline in the industry, along with underperformance in certain of the companys dress shirt brands. Partially offsetting the wholesale decline was a 1 percent increase in retail comparable store sales (excluding the Izod retail business, which is no longer included in retail comparable store sales, as the business is being exited in fiscal 2015).

Earnings before interest and taxes on a non-GAAP basis decreased to $17 million compared to $29 million in the prior years fourth quarter due to the revenue decline in the companys dress shirt business coupled with a decline in gross margin in that business, as additional markdowns were required due to excess inventory levels.

Loss before interest and taxes on a GAAP basis was $9 million as compared to income before interest and taxes of $21 million in the prior years fourth quarter. The decrease was mainly attributable to the dress shirt business decline noted above and $21 million of expenses incurred in connection with exiting the Izod retail business (most of which were noncash impairment charges), partially offset by a reduction in acquisition, integration and restructuring costs incurred in 2014 as compared to the prior year period.

Fourth Quarter Consolidated Earnings:

Earnings before interest and taxes on a non-GAAP basis increased 4 percent on a constant currency basis (decreased 2 percent including foreign currency exchange rate impacts) from the prior years fourth quarter of $207 million, due to continued strong performance in the Tommy Hilfiger business and an earnings increase in the Calvin Klein business, partially offset by poor performance within the companys Heritage Brands dress shirt business.

Earnings before interest and taxes on a GAAP basis was $6 million as compared to $160 million in the prior years fourth quarter. The decrease was primarily due to a retirement plan actuarial loss of $139 million incurred in the fourth quarter of 2014 (as compared to an actuarial gain of $53 million in the fourth quarter of 2013) and the expenses incurred in connection with exiting the Izod retail business, partially offset by lower integration and restructuring costs compared to the fourth quarter of 2013.

Net interest expense decreased to $32 million from $45 million in the prior years fourth quarter due to lower average debt balances and interest rates, combined with the effect of the amendment and restatement of the companys credit facility during the first quarter of 2014 and the related redemption of its 7 3/8 percent senior notes due 2020.

Full Year 2014 Consolidated Results:

Earnings per share on a non-GAAP basis for 2014 was $7.30 compared to $7.03 for the prior year. GAAP earnings per share was $5.27 compared to $1.74 for the prior year.

Revenue was $8.24 billion, including a negative $100 million impact related to foreign currency exchange rate changes. Revenue in the prior year was $8.22 billion on a non-GAAP basis and $8.19 billion on a GAAP basis.

The revenue increase was due to:

- A 3 percent increase in the Calvin Klein business compared to 2013, driven by (i) the ten additional days of operations in 2014 of the acquired Calvin Klein businesses compared to 2013; (ii) mid-single digit and high-single digit percentage increases in the North America wholesale and retail businesses, respectively; (iii) an increase in royalty revenue; and (iv) the absence of $30 million of sales returns recorded in 2013 for certain wholesale customers in Asia in the acquired business in connection with an initiative to reduce excess inventory levels. Retail comparable store sales increased 2 percent in North America and decreased 5 percent internationally. The decline in international retail comparable store sales was due in large part to a decrease in Asia resulting from the timing of the Chinese New Year, as fiscal 2014 did not include a Chinese New Year, while the holiday fell into both the first and fourth quarters in fiscal 2013. Also contributing to the retail comparable store decline was underperformance in Europe in the first half of the year.

- A 6 percent increase on a constant currency basis (4 percent increase on a GAAP basis) in the Tommy Hilfiger business compared to 2013. Tommy Hilfiger North America revenue increased 6 percent, principally due to high-single digit percentage wholesale growth, retail comparable store sales growth of 2 percent and square footage expansion in company-operated stores. Tommy Hilfiger International revenue increased 5 percent on a constant currency basis (increased 3 percent on a GAAP basis), driven principally by European retail comparable store sales growth of 3 percent, square footage expansion in company-operated stores and low-single digit percentage wholesale growth.

- A 1 percent decrease in the Heritage Brands business compared to the prior year excluding $176 million of revenue related to the Bass business, as mid-single digit percentage growth in the wholesale sportswear business was more than offset by the poor performance of the dress shirt business and a 5 percent comparable store sales decline in the companys retail stores (excluding the Izod retail business in the fourth quarter, which is no longer included in retail comparable store sales as the business is being exited in 2015). Including the Bass revenue in 2013, revenue decreased 9 percent, or $186 million, to $1.80 billion from $1.99 billion in the prior year.

Earnings before interest and taxes on a non-GAAP basis decreased to $921 million from $967 million in the prior year, principally due to:

- A $30 million decline in the Calvin Klein business, driven principally by investments in the acquired Warnaco businesses.

- A $31 million increase in the Tommy Hilfiger business, principally attributable to the revenue increase mentioned above, combined with operating margin improvement.

- A $43 million decline in the Heritage Brands business, principally attributable to the revenue decrease mentioned above and a gross margin decline resulting from overall increased promotional activity in order to drive traffic and revenue, combined with poor performance within the dress shirt and retail businesses.

GAAP earnings before interest and taxes increased to $530 million from $513 million in the prior year. The earnings increase was primarily due to a net decrease in restructuring and Warnaco acquisition and integration costs as compared to the prior year. Also contributing to the earnings increase was an increase in the Tommy Hilfiger business. Partially offsetting these increases were (i) the earnings decreases on a non-GAAP basis in the Calvin Klein and Heritage Brands businesses discussed above; (ii) a retirement plan actuarial loss incurred in 2014 (as compared to an actuarial gain in 2013); and (iii) expenses incurred in connection with exiting the Izod retail business.

Net interest expense decreased to $139 million from $185 million in the prior year due to lower average debt balances and interest rates combined with the effect of the amendment and restatement of the companys credit facility during the first quarter of 2014 and the related redemption of its 7 3/8 percent senior notes due 2020. During the fourth quarter of 2014, the company made debt repayments totaling approximately $180 million on its outstanding term loans, for total 2014 term loan debt repayments of $425 million, most of which were voluntary.

2015 Guidance:

In 2015, the company expects its full year earnings per share results to be negatively impacted versus the prior year by (i) approximately $1.20 per share from foreign currency exchange rates due to the significant strengthening of the United States dollar against other currencies in which the company transacts significant levels of business, and (ii) volatility in the global macroeconomic environment, particularly with respect to the companys businesses in Russia. The company expects a negative impact of approximately $0.10 per share from its Russia businesses due to political and economic instability in the region.

Full Year Guidance

Earnings per share is currently projected to be in a range of $6.75 to $6.90 on a non-GAAP basis, which reflects the expected $1.30 negative impact related to foreign currency exchange rates and pressures on the companys Russia businesses as described above. Excluding this negative impact, earnings per share on a non-GAAP basis is expected to increase 10 percent to 12 percent versus the prior years non-GAAP earnings per share of $7.30.

Revenue in 2015 is currently projected to increase approximately 3 percent on a constant currency basis (decrease approximately 4 percent on a GAAP basis). It is currently projected that revenue for the Calvin Klein business in 2015 will increase approximately 5 percent on a constant currency basis (will be relatively flat on a GAAP basis). Revenue for the Tommy Hilfiger business in 2015 is currently expected to increase approximately 3 percent on a constant currency basis (decrease approximately 7 percent on a GAAP basis). Revenue for the Heritage Brands business in 2015 is currently projected to decrease approximately 4 percent.

Net interest expense is expected to be approximately $120 million to $125 million in 2015 compared to the 2014 amount of $139 million, due to the impact of 2015 anticipated debt payments and the full year impact of payments made in 2014. The company expects to use its free cash flow to repay at least $425 million of debt in 2015. The company currently estimates that the 2015 effective tax rate will be approximately 22 percent.

The companys earnings per share estimate on a non-GAAP basis excludes approximately $50 million of pre-tax costs associated primarily with the Warnaco integration and related restructuring and $20 million of pre-tax costs associated with operating and exiting the Izod retail business. (Please see section entitled Non-GAAP Exclusions for details on these pre-tax costs.)

First Quarter Guidance

First quarter 2015 earnings per share on a non-GAAP basis is currently projected to be in a range of $1.35 to $1.40, which reflects an expected $0.30 per share negative impact related to foreign currency exchange rates and pressures on the companys Russia businesses as described above. Excluding this negative impact, earnings per share on a non-GAAP basis is expected to increase 12 percent to 16 percent versus the prior years first quarter non-GAAP earnings per share of $1.47.

Revenue in the first quarter of 2015 is currently projected to increase approximately 2 percent on a constant currency basis (decrease approximately 6 percent on a GAAP basis). It is currently projected that revenue for the Calvin Klein business in the first quarter of 2015 will increase approximately 3 percent on a constant currency basis (decrease approximately 3 percent on a GAAP basis). Revenue for the Tommy Hilfiger business in the first quarter of 2015 is currently expected to increase approximately 2 percent on a constant currency basis (decrease approximately 10 percent on a GAAP basis). Revenue for the Heritage Brands business in the first quarter of 2015 is currently projected to decrease approximately 1 percent.

The company projects that first quarter net interest expense will be approximately $30 million, a reduction of $11 million compared to the first quarter of 2014 due to the impact of payments made in 2014. The company currently estimates that the first quarter tax rate will be between 25 percent and 26 percent.

The companys first quarter earnings per share estimate excludes approximately $20 million of pre-tax costs associated with the integration and related restructuring of Warnaco and $10 million of pre-tax costs associated with operating and exiting the Izod retail business. (Please see section entitled Non-GAAP Exclusions for details on these pre-tax costs.)

Non-GAAP Exclusions:

The discussions in this release that refer to non-GAAP amounts exclude the following:

- Pre-tax costs of approximately $20 million expected to be incurred in 2015 related to operating and exiting the Izod retail business, of which $10 million is expected to be incurred in the first quarter.

- Pre-tax costs of approximately $50 million expected to be incurred in 2015 in connection with the integration of Warnaco and the related restructuring, of which $20 million is expected to be incurred in the first quarter.

- Pre-tax costs of approximately $138 million incurred in 2014 in connection with (i) the integration of Warnaco and the related restructuring, including a pre-tax gain resulting from the deconsolidation of certain Calvin Klein subsidiaries in Australia and New Zealand, which were transferred to the companys joint venture there, and the previously consolidated Calvin Klein joint venture in India, which the company effectively no longer controls; (ii) the sale of the Bass business, which closed in the fourth quarter of 2013 (as certain costs related to the sale were incurred in 2014); (iii) the impairment of certain Tommy Hilfiger stores in North America in the second quarter of 2014; and (iv) costs incurred in connection with the exit of a discontinued product line in the Tommy Hilfiger Japan business. Of the total costs, $26 million was incurred in the first quarter, $46 million was incurred in the second quarter, $29 million was incurred in the third quarter and $37 million was incurred in the fourth quarter.

- Pre-tax costs of approximately $21 million incurred in the fourth quarter of 2014 related to the exit of the Izod retail business, which includes approximately $18 million of noncash charges related to asset impairments.

- Pre-tax costs of $93 million recorded in the first quarter of 2014 associated with the amendment and restatement of the companys credit facility and the related redemption of its 7 3/8 percent senior notes due 2020.

- A pre-tax expense of $139 million recorded in the fourth quarter of 2014 related to recognized actuarial losses on retirement plans.

- Discrete tax benefits of $92 million in 2014 primarily related to various Warnaco integration activities and the resolution of uncertain tax positions, of which $30 million was recorded in the second quarter, $25 million was recorded in the third quarter and $37 million was recorded in the fourth quarter.

- A revenue reduction of $30 million in the first quarter of 2013 attributable to sales returns accepted from certain Warnaco Asia wholesale customers to reduce excess inventory levels.

- Pre-tax costs of $511 million incurred in 2013 in connection with the acquisition, integration and related restructuring of Warnaco, including costs associated with the debt modification and extinguishment completed at the time of the Warnaco acquisition, and the sales returns mentioned above, of which $224 million was incurred in the first quarter, $128 million was incurred in the second quarter, $61 million was incurred in the third quarter and $99 million was incurred in the fourth quarter. Approximately $215 million of the acquisition, integration and related restructuring charges incurred in 2013 were noncash charges, the majority of which were short-lived valuation adjustments and amortization.

- Pre-tax income of $24 million recorded in the third quarter of 2013 due to the amendment of an unfavorable contract, which resulted in the reduction of a liability recorded at the time of the Tommy Hilfiger acquisition.

- A pre-tax loss of $20 million, including related costs, incurred in 2013 in connection with the sale of substantially all of the assets of the Bass business, which closed on November 4, 2013, of which $19 million was incurred in the third quarter and $1 million was incurred in the fourth quarter.

- Pre-tax income of $53 million recorded in the fourth quarter of 2013 related to recognized actuarial gains on retirement plans.

- A tax expense of $120 million recorded in the fourth quarter of 2013 in connection with an increase to the companys previously established liability for an uncertain tax position related to European and U.S. transfer pricing arrangements.

- A net tax expense of $5 million recorded in 2013 associated with various Warnaco integration activities and various adjustments to liabilities for changes in estimates in uncertain tax positions, of which an expense of $28 million was recorded in the second quarter, a benefit of $28 million was recorded in the third quarter and an expense of $5 million was recorded in the fourth quarter.

- Estimated tax effects associated with the above pre-tax items, which are based on the companys assessment of deductibility. In making this assessment, the company evaluated each item that it had identified above as a non-GAAP exclusion to determine if such item is taxable or tax deductible, and if so, in what jurisdiction the tax expense or tax deduction would occur. All items above were identified as either primarily taxable or tax deductible, with the tax effect taken at the statutory income tax rate of the local jurisdiction, or as non-taxable or non-deductible, in which case the company assumed no tax effect.