Newell Brands reported earnings dropped in the second quarter but came in above Wall Street’s consensus estimates. Newell also indicated that it delivered significant improvements in operating margin and operating cash flow.

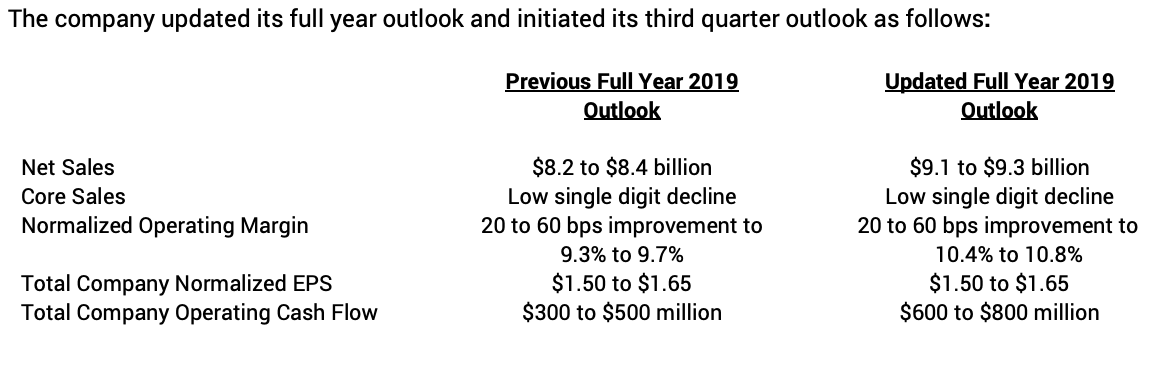

“The financial results we announced this morning represent another quarter of progress, with disciplined cost management and focused execution behind working capital initiatives driving better than expected margin and cash flow progression in the second quarter,” said Chris Peterson, Newell Brands Interim Chief Executive Officer and Chief Financial Officer. “Encouraging first half results and the green shoots of progress we are driving across the business give us the confidence to reiterate our outlook for full year core sales, operating margin and earnings per share and to raise our full year outlook for operating cash flow to between $600 and $800 million. While still early in the organization’s turnaround, we believe our decisive and strategic actions to strengthen our performance will drive further improvement going forward, as we work to transform Newell Brands into a leading next-generation consumer products company.”

Second Quarter 2019 Executive Summary

- Net sales from continuing operations were $2.1 billion, a decline of 3.9 percent compared with the prior year period.

- Core sales from continuing operations declined 1.1 percent from the prior year period.

- Reported operating margin was 8.4 percent compared with 3.8 percent in the prior year period. Normalized operating margin was 11.3 percent compared to 9.7 percent in the prior year period.

- Reported diluted earnings per share for the total company were $0.21 compared with $0.27 in the prior year period.

- Normalized diluted earnings per share for the total company were $0.45 compared with $0.78 in the prior year period.

- Operating cash flow was $191 million, a $180 million improvement versus a year ago.

- Gross debt was reduced by $517 million in the quarter; net debt was reduced by $777 million.

- Divestitures of Process Solutions and Rexair were completed and an agreement was signed to divest the U.S. Playing Cards business, which is anticipated to close in the second half of 2019.

- The company announced its decision to retain the Rubbermaid Commercial Products business, which has previously been included in discontinued operations. The addition of Rubbermaid Commercial Products to the continuing operations portfolio will be accretive to operating margins, normalized earnings per share and operating cash flow in 2020 and future years.

- The company announced its decision to move its corporate headquarters to Atlanta, GA, in order to facilitate a stronger connection between senior leaders and the operations of the business, and to enhance the company’s culture and sense of community. Three of Newell’s seven operating divisions (Writing, Baby and Food) are based in Atlanta.

Second Quarter 2019 Operating Results

Net sales were $2.1 billion, a 3.9 percent decline compared to the prior year period, attributable to the impact of foreign exchange and a 1.1 percent decline in core sales.

Reported gross margin was 35.3 percent compared with 35.2 percent in the prior year period, as pricing, productivity and positive mix offset headwinds from foreign exchange, tariffs and inflation. Normalized gross margin was 35.6 percent compared with 35.1 percent in the prior year period.

Reported operating income was $178 million compared with $83.9 million in the prior year period, due to gross margin expansion and a reduction in overhead costs. Normalized operating income was $240 million compared with $214 million in the prior year period. Reported operating margin was 8.4 percent compared with 3.8 percent in the prior year. Normalized operating margin was 11.3 percent compared to 9.7 percent in the prior year period.

Reported tax expense was $16.7 million, or 16.8 percent, compared with $53.0 million in the prior year period. Normalized tax expense was $41.1 million, or 25.4 percent, compared with a benefit of $0.7 million in the prior year period.

The company reported net income of $89.8 million compared with $132 million in the prior year period. Reported diluted earnings per share for the total company were $0.21 compared with $0.27 in the prior year period.

Normalized net income for the total company was $190 million, or $0.45 diluted earnings per share, compared with $379 million, or $0.78 diluted earnings per share, in the prior year period. Wall Street’s consensus estimate had been 36 cents a share.

Operating cash flow was $191 million compared with $11.2 million in the prior year period, primarily enabled by strategic actions taken to improve cash conversion cycles on receivables and payables.

Second Quarter 2019 Operating Segment Results

The Learning & Development segment generated net sales of $849 million compared with $839 million in the prior year period, as core sales growth more than offset the headwind from foreign exchange. Core sales increased 3.5 percent, driven by increases in both Baby and Writing. Reported operating income was $217 million compared with $196 million in the prior year period. Reported operating margin was 25.6 percent compared with 23.3 percent in the prior year period. Normalized operating income was $221 million versus $207 million in the year-ago period. Normalized operating margin was 26.1 percent compared with 24.7 percent in the prior year period.

The Food & Appliances segment generated net sales of $562 million compared with $620 million in the prior year period, due primarily to the impact of unfavorable foreign exchange and a core sales decrease of 7.1 percent. The core sales decline largely reflected a timing shift in orders from the second quarter to the first quarter associated with an SAP implementation in Fresh Preserving, and continued challenges in the Appliances business. Reported operating income was $33.5 million compared with $39.5 million in the prior year period. Reported operating margin was 6.0 percent compared with 6.4 percent in the prior year period. Normalized operating income was $43.1 million versus $47.6 million in the prior year period. Normalized operating margin was 7.7 percent, the same as in the prior year period.

The Home & Outdoor Living segment generated net sales of $705 million compared with $742 million in the prior year period, with the change attributed to the impact of unfavorable foreign exchange, the exit of 72 underperforming Yankee Candle retail stores in the first half of 2019 and a core sales decline of 1.1 percent. The Home Fragrance and Connected Home and Security divisions posted positive core sales, which were offset by lower core sales in Outdoor and Recreation largely due to the impact of lost distribution in the prior year. Reported operating income was $19.2 million compared with operating income of $9.4 million in the prior year period. Reported operating margin was 2.7 percent compared with 1.3 percent in the prior year period. Normalized operating income was $39.7 million compared with $48.4 million in the prior year period. Normalized operating margin was 5.6 percent compared with 6.5 percent in the prior year period.

Outlook for Full Year and Third Quarter 2019

For the third quarter, Newell expects:

- Net Sales: $2.42 to $2.47 billion

- Core Sales: 2 to 4 percent decline

- Normalized Operating Margin: 100 to 130 bps contraction to 11.9 percent to 12.2 percent

- Total Company Normalized EPS: $0.55 to $0.60

Newell Brands’ portfolio of brands include: Paper Mate, Sharpie, Dymo, EXPO, Parker, Elmer’s, Coleman, Marmot, Oster, Sunbeam, FoodSaver, Mr. Coffee, Rubbermaid Commercial Products, Graco, Baby Jogger, NUK, Calphalon, Rubbermaid, Contigo, First Alert and Yankee Candle. Outdoor & Recreation brands also include Aerobed, Bubba, Campingaz and Stearns.

Photo courtesy Coleman