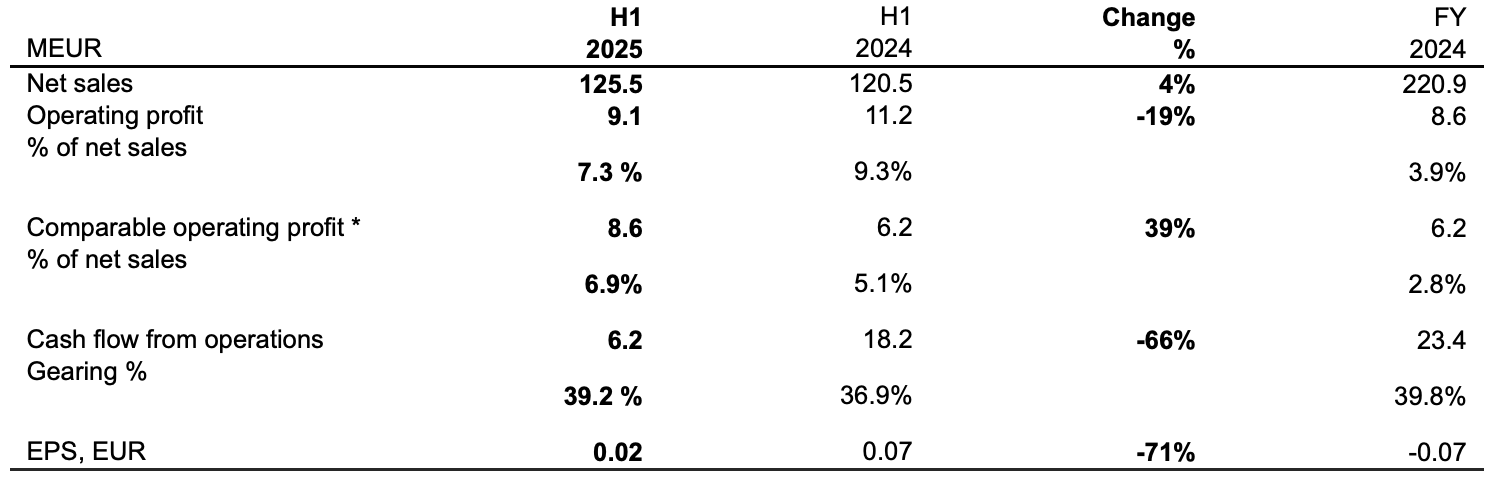

Rapala VMC reported 2025 first half (H1) net sales were €125.5 million, up 4 percent compared to €120.5 million in the 2024 H1 period. With comparable exchange rates, currency-neutral sales were said to be up 5 percent from the prior-year H1 period.

The Helsinski, Finland-based company said U.S. reciprocal tariffs have disrupted supply chains with stop and go, inventory build ups, as well as occupy a dedicated internal task force to develop solutions to minimize impacts. They remain a matter of the greatest attention and although mitigated do impact gross margins as only partially compensated by customers.

Regional Summary

Rapala said the operating environment varied significantly across regions during the first half of 2025.

“The North American market remained resilient, supported by stable consumer demand and steady retail activity,” the Board of Directors (Board) noted in the company’s 2025 Interim Report summary. “In contrast, the European and Asian markets were impacted by increased uncertainty and limited economic visibility, primarily driven by the ongoing global trade disputes. The effects of this market turbulence became more pronounced during the second quarter.”

North America

Sales in North America increased 12 percent compared to the 2024 H1 period. With comparable translation exchange rates, currency-neutral sales were reportedly up 14 percent year-over-year.

“Favorable fishing conditions in Autumn 2024, combined with an exceptionally strong winter fishing season in 2024/2025, enabled retailers to reduce their inventories by year-end,” the Board reported. “This supported robust replenishment sales of winter products in the early part of the year and facilitated a healthy level of spring load-in orders.”

Sales growth was said to be further driven by the successful launch of the new 13 Fishing branded product range, the continued strong performance of CrushCity soft plastic lures, and the solid momentum of all key brands.

Nordic Region

Sales in the Nordic market decreased 4 percent compared to the 2024 H1 period with both reported and comparable translation exchange rates.

The company said the year began with poor snow conditions, which led to exceptionally low replenishment sales of winter sports equipment which had a significant impact on the sales of the region.

“On a positive note, past organizational changes in the fishing business are yielding positive results, enabling strong operational performance,” the Board said. “Product availability remained good and increased sales were achieved in majority of the key brands.”

Still, the summer season was said to have “started somewhat later than usual,” which impacted replenishment sales towards the end of the reporting period.

Rest of Europe

Sales in the Rest of Europe region decreased 6 percent compared to the 2024 H1 period with both reported and comparable translation exchange rates.

Retailer carryover stock from the previous season impacted the sales in the region. The year began on a positive note, but momentum slowed significantly midway through the reporting period. Consumer activity remained subdued, and retailers continued to exercise extreme caution with replenishment orders. Focus remained on core brands and as a highlight, Okuma brand continued on a growth path.

Rest of the World

With reported translation exchange rates, sales in the Rest of the World market were flat year-over-year. With comparable translation exchange rates, sales increased by 5 percent compared to the previous year.

Sales in the Asian markets reportedly declined, as ongoing global trade disputes continued to weigh on consumer sentiment and cause foreign exchange volatility. The competition landscape also evolved, with Asian fishing equipment manufacturers increasing their investments in domestic markets, thereby emerging as stronger local competitors. In contrast, Latin American markets performed well, supported by economic recovery and currency stability in key countries. These strengthened consumer confidence and supported the sales of imported products.

External Net Sales by Region

Profitability and Expenses

Comparable (excluding mark-to-market valuations of operative currency derivatives and other items affecting comparability) operating profit increased by €2.4 million from the comparison period. Reported operating profit decreased by €2.1 million from the comparison period and the items affecting comparability had a positive impact of €0.5 million (€5.0 million) on reported operating profit.

Comparable operating profit margin was 6.9 percent (5.1 percent) for the first half of 2025. The improved profitability was primarily driven by increased sales in both the winter fishing and open water markets. While tariffs had a negative impact on the cost base, overall profitability strengthened thanks to a structurally lower operating expense level.

Reported operating profit margin was 7.3 percent (2024: 9.3 percent) for the first half. Reported operating profit includes a €0.6 million (2024: -0.2 million) mark-to-market valuation of operative currency derivatives. Other items affecting comparability, included in the reported operating, profit were -€0.2 million (€5.0 million). This amount includes a gain on the disposal of real estate in Finland, as well as a non-cash currency translation loss relating to the closure of the Russian manufacturing operation. Prior year gain comes from the sale and lease back transaction of the Canadian real estate.

Total financial (net) expenses were €4.9 million (2024: €4.3 million) for the first half of the year. Net interest and other financing expenses were €3.5 million (2024: €4.5 million) and (net) foreign exchange losses were €1.3 million versus a €0.2 gain in H1 2024.

Net profit for the first half of the year decreased by €2.5 million and was €2.2 million, or €0.02 per share, in H1 compared to €4.7 million, €0.07 per share, in H1 2024.

Financial Position

Cash flow from operations decreased from the previous year and amount to €6.2 million (2024: €18.2 million). Change in net working capital had a negative €4.8 million (2024: positive €12.5 million) impact on cash flow. Excluding working capital impact, cash flow from operations improved from the previous year and was €11.0 million (2024: €5.7 million), following the relentless focus on cash generation and operational efficiencies.

End of the period inventory was € 82.2 million (€84.7 million). The change in obsolescence allowance increased inventory value by €0.2 million. Changes in translation exchange rates decreased inventory value by €3.3 million. The organic increase in inventory was €0.5 million. Inventory composition is healthier and includes higher proportion of winter fishing products in response to a stronger order book for the upcoming winter season.

Net cash used in investing activities was €0.7 million (2024: positive €5.7). Capital expenditure was €1.8 million (€2.7 million) and disposals €1.1 million (8.7 million). Expenditure consisted mainly of maintenance of manufacturing capacity and investments in new products. Disposals include proceeds from the sale of real estate in Finland. Prior year disposals include the sale and lease back of the Canadian real estate.

Liquidity position of the Group was good. Undrawn committed long-term credit facilities amounted to €38.0 million. Commercial papers sold under the commercial paper program amounted to €14.0 million (€15.0 million) at the end of the reporting period. Gearing ratio increased and equity-to-assets ratio decreased from last year.

The Group’s €106 million senior secured term and revolving credit facilities agreement includes financial covenants based on the available liquidity (minimum €22.5 million), 12-month rolling EBITDA (minimum €10 million), net debt to consolidated equity (maximum 100 percent) and net debt to EBITDA, or “leverage ratio”. The financial leverage ratio covenant level is 3.80. Covenants are regularly tested, either quarterly or on the last date of each month. The risk of breaching the covenants would trigger negotiations between the Group and lending banks to resolve the potential covenant breach, and to agree on actions to rectify the situation. In the unlikely event of unresolved covenant breach, the lending banks would have the right to call all or any part of the loans and related interest.

On Q1/2025 and Q2/2025 testing dates, the leverage ratio landed at 3.48 and 2.91. Calculation of the covenants include customary adjustments mainly related to items affecting comparability and asset disposals, and therefore deviate from the reported figures elsewhere in this report. The Group is currently compliant with all financial covenants and expects to comply with future bank requirements as well. The Group’s liquidity position remains good, and cash and cash equivalents amounted to 25.4 million at June 30, 2025.

During the reporting period, the Group agreed on an amendment and an extension of 6 months with the lending banks for the €106 million facilities. As of the reporting date, the facilities mature in the second half of 2026, subject to an extension option of 6 months. The Group is preparing to refinance the facilities and the hybrid capital bond during the next 12 months.

The Group equity includes a hybrid loan of €30.0 million issued in November 2023. The accumulated non-recognized interest on hybrid bond were €2.2 million.

Short-Term Outlook and Risks

The Board said it believes that the company’s renewed strategy will provide added value to customers and other stakeholders.

“We will continue to invest in growth and efficiency to strengthen our position as one of the leading companies in the fishing tackle market,” the company noted.

The Board said North American consumer demand has remained robust despite rising uncertainties in the global trade environment and efforts to mitigate the tariff impact on sales and profitability have been successful.

“Nevertheless, the ongoing tariff situation reduces visibility and continues to create challenges in driving sales and maintaining profitability,” the Board said.

European markets are reportedly showing slower consumer spending following the economic and political developments of the first half. This is expected to result in lower replenishment sales in H2. Rapala said its improved operational efficiency and structurally lower operating expense base are expected to partially offset the impact of the potential sales decline.

Pre-sales for the upcoming 2025/2026 winter fishing season have reportedly “progressed according to expectations” in the North American market. In the Nordic region, the winter fishing market is expected to remain at the prior-year level.

“Our guidance reflects current market conditions but remains subject to potential trade-related disruptions, including tariffs and regulatory changes, which may impact demand and cost structures,” stated the Board.

Consequently, the Group expects 2025 full year comparable operating profit (excluding mark-to-market valuations of operative currency derivatives and other items affecting comparability) to increase from 2024.

Image courtesy Rapala VMC