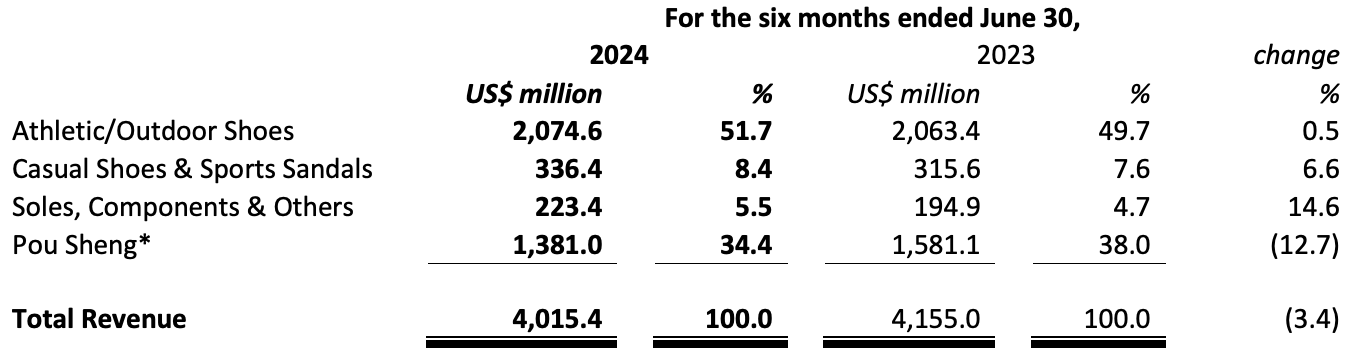

Yue Yuen Industrial (Holdings) Limited reportedly saw the volume of shoes it shipped to brands in the U.S. and Europe increase nearly 10 percent in the first half period ended June 30 (H1), but revenues for those pairs only increased 1.3 percent as average selling prices (ASP) declined for the period. Athletic and Outdoor Footwear value increased 0.5 percent year-over-year and Casual Shoes and Sport Sandals shipment value increased 6.6 percent year-over-year.

Consolidated revenue for the company, which also includes the Pou Sheng China retail business declined 3.4 percent year-over-year (y/y) to $4.02 billion for the six-month period.

Yue Yuen Industrial Ltd, which is based in Hong Kong, reports in US dollar ($) terms.

Revenue by Reporting Segment:

Footwear Manufacturing activity, including athletic/outdoor shoes, casual shoes and sports sandals, increased 1.3 percent y/y to $2.41 billion in the first half. The volume of shoes shipped during the period increased by 9.9 percent to 120.7 million pairs amid a “decent recovery trend and a further normalized order book.” The average selling price decreased by 7.8 percent to $19.98 per pair, reportedly due to a high base effect and changes to its product mix, partially offsetting the recovery of shipment volumes.

Revenue for the overall Manufacturing business (including footwear, as well as soles, components and others) was $2.63 billion in the first half, representing a year-over-year increase of 2.4 percent as compared to the corresponding H1 period last year.

Footwear product value shipped to the U.S. market declined less than one percent to $701.2 million in the first half, compared to $707.2 million in the 2023 first half. Footwear product value shipped to the Europe market were down 2 percent to $682.2 million in the H1 period, compared to $696.0 million in the 2023 H1 period.

Revenue attributed to Pou Sheng decreased by 12.7 percent y/y to $1.38 billion for the H1 period, compared to $1.581 billion in the 2023 corresponding period. In RMB terms (Pou Sheng’s reporting currency), revenue decreased 8.9 percent y/y to RMB 9.98 billion, compared to RMB 10.96 billion in the corresponding period last year. The decline was said to be mostly attributable to weak store traffic amid an increasingly dynamic retail environment in mainland China, despite the relatively resilient performance of its omni-channels.

Pou Sheng had 3,478 directly operated retail stores across the Greater China region at period-end, representing a net closure of 45 stores as compared with the 2023 year-end, with the contribution of quality larger-format stores (above 300 square meters) to Pou Sheng’s directly-operated store count rose to 21.0 percent, up 130 basis points y/y from 19.7 percent at the end of the 2023 H1 period. The company said ensuring a holistic approach to new store openings and selectively rightsizing or upgrade of its stores is at the core of Pou Sheng’s retail refinement strategy, enabling it to focus on enhancing store-level efficiency.

The profit attributable to owners of the company was $184.4 million, an increase of 120.6 percent compared to $83.6

million recorded for the corresponding period last year. The profit attributable to owners of the Manufacturing business increased by 177.5 percent to $155.4 million. The profit attributable to owners of Pou Sheng increased by 9.9 percent to RMB 335.7 million. The basic earnings per share for the first half of 2024 was 11.44 cents, compared to 5.19 cents for the corresponding period of last year.

The Board said it has resolved to declare an interim dividend of HK$0.40 per share (2023: HK$0.20 per share) for shareholders whose names appear on the register of members of the company on Wednesday, September 11, 2024. The interim dividend shall be paid on Friday, October 4, 2024. The company’s commitment to upholding a relatively steady dividend level over the long-term remains intact.

Income Statement Summary

he company’s gross profit slightly decreased by 0.3 percent to $975.1 million, while the overall gross profit margin increased by 0.8 percentage points to 24.3 percent. The gross profit of the Manufacturing business increased by 12.1 percent to $502.6 million, with the gross profit margin of the Manufacturing business increased by 1.7 percentage points to 19.1 percent as compared to the corresponding period of last year, which was mainly attributed to strong demand for footwear capacity which led to its improved overall capacity utilization rate, flexible production scheduling and orderly overtime arrangement, effective cost-reduction, as well as efficiency-improvement efforts. Production leveling across the company’s Manufacturing facilities was uneven, with some factories experiencing higher utilization rates due to more overtime, alongside the ramp-up of new production capacity.

The gross profit margin for Pou Sheng in the Period was 34.2 percent, an increase of 0.7 percentage points. Well managed discount controls, coupled with effective inventory management, reportedly helped offset an unfavorable channel mix.

The company’s total Selling and Distribution expenses for the H1 period decreased 10.4 percent to $424.2 million (first half of 2023: $473.4 million), equivalent to approximately 10.6 percent (first half of 2023: 11.4 percent) of revenue.

Administrative expenses for the period decreased by 3.8 percent to $275.3 million (first half of 2023: $286.3

million), equivalent to approximately 6.9 percent (first half of 2023: 6.9 percent) of revenue.

Other income for the period decreased by 4.7 percent to $63.4 million (first half of 2023: $66.5 million), equivalent to approximately 1.6 percent (first half of 2023: 1.6 percent) of revenue. Other expenses decreased by 38.8 percent to $79.7 million (first half of 2023: $130.2 million), equivalent to approximately 2.0 percent (first half of 2023: 3.1 percent) of revenue. Among which, there were no expenses for production capacity adjustments incurred during the Period, when compared to one-off expenses of approximately $20.5 million for production capacity adjustments during the corresponding period of 2023. As a result, the company’s net operating expenses for the Period decreased by $107.6 million or 13.1 percent.

Non-recurring profit attributable to owners of the company was $5.5 million in the first half, compared to $3.7 million recognized in the corresponding period of last year. This included a one-off gain on the partial disposal of associates totaling $24.0 million, which was largely offset by a loss of $11.9 million due to fair value changes on financial instruments at fair value through profit or loss (“FVTPL”) and a combined impairment loss of $6.6 million on interests in a joint venture and an associate.

Excluding all items of non-recurring in nature, the recurring profit attributable to owners of the company for the period under review was $178.9 million, representing an increase of 123.8 percent compared with $79.9 million for the corresponding H1 period last year.

Balance Sheet Summary

The company’s financial position reportedly remained solid in the first half, ending the period with net cash of $65.8 million, compared to $169.4 million on December 31, 2203.

The company’s gearing ratio (total bank borrowings to total equity) was 18.1 percent (December 31, 2023: 20.7 percent). Free cash inflow amounted to $79.9 million (first half of 2023: $279.1 million).

Share of Results of Associates and Joint Ventures

For the Period under review, the share of results of associates and joint ventures was a combined profit of $32.9 million, compared to a combined profit of $29.1 million in the corresponding period of last year.

Outlook

The company said it is confident about the solid recovery trend taking place in the footwear industry, alongside improving order visibility, which is allowing the further normalization of its order book. The market research agency Statista estimates that global footwear market consumption will experience a compound annual growth rate of 3.4 percent from 2024 to 2028. However, the overall business environment remains unsettled in a short period of time due to uncertainties stemming from global macroeconomic conditions, including persistent inflation and high interest rates, as well as regional conflicts and its impact on shipping lanes.

Yue Yuen said it will continue to proactively monitor the economic and industry-specific environment and is adopting a comprehensive plan to increase its Manufacturing manpower and capacity to balance demand, its order pipeline and labor supply. While the ramp-up of new production capacity will take time, which may impact the company’s short-term efficiency, it will continue to strengthen its operational resilience by enhancing efficiency and productivity, through its highly flexible and agile strategies, and by leveraging its core strengths, adaptability and competitive edges, as well as cost and expense controls, to safeguard its profitability, while focusing on maintaining a healthy cash flow and a solid financial position.

The Group remains optimistic about the long-term prospects of its Manufacturing business and remains committed to its mid to long-term capacity allocation strategy. This includes diversifying its Manufacturing capacity in regions such as Indonesia and India where labor supply and infrastructure are supportive of sustainable growth. It will continue to exploit its strategy of prioritizing value growth, leveraging the ‘athleisure’ trend and its integrated product development capability that combines automation technology and research and development strength to seek more high value-added orders with a solid product mix.

For Pou Sheng, amid the ongoing dynamic retail environment in mainland China, the company said it will continue to safeguard its margins through its retail refinement strategy – dynamically managing its B&M and omni-channel footprint, as well as introducing new store concepts and broadening its category offerings. It will also implement its digital transformation strategy, including the enhancement and upgrade of its SAP system in order to better integrate its business and finance functions and strengthen strategic decision-making at the management level. It will further maximize its strategic partnerships with existing and new business associates and diversify its channel mix, while remaining committed to dynamic inventory control and more effective working capital management.

Going forward, the company remains confident that the above strategies will enable it to continue providing its

brand partners with the best possible end-to-end solutions, anchoring its quality growth while safeguarding

its solid long-term profitability and ability to deliver sustainable returns to shareholders.

“Order visibility improved in the first half of the year, driven by the gradual recovery of the footwear industry, alongside the Olympics, and following the completion of the destocking cycle,” commented company Chairman Lu Chin Chu. “As a result, our Manufacturing business saw a decent recovery and solid growth in profitability. Amid the ongoing dynamic retail environment in mainland China, Pou Sheng further safeguarded its competitiveness by introducing new store concepts and broadening category offerings. Based on our solid operating performance, we are pleased to declare an interim dividend of HK$0.40 per share, in line with historical levels in normal operational years. Looking ahead, we will continue to build operational resilience, strive for sustainable development, and create value and returns for shareholders.