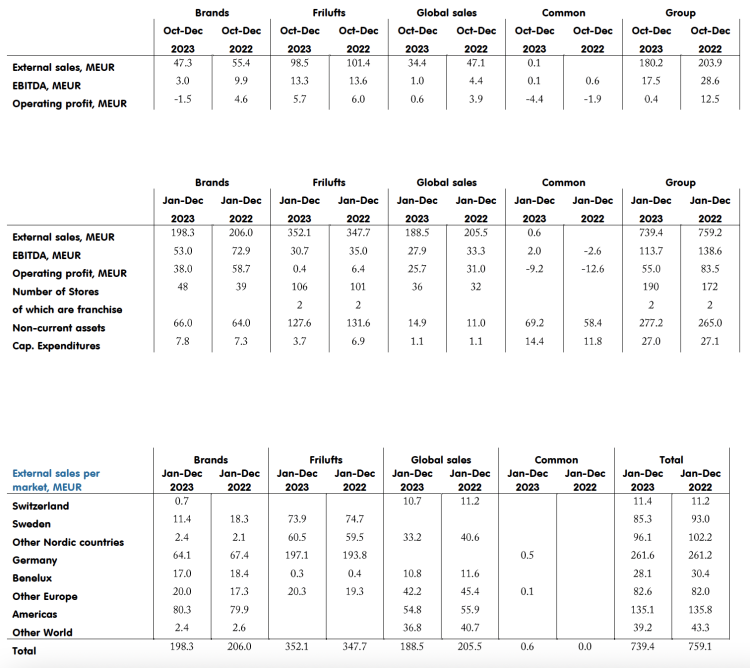

Fenix Outdoor International AG (Group) reported that consolidated fourth-quarter sales declined 11.6 percent to €180.2 million, compared to €203.9 million in the prior-year comp quarter. Group operating profit shrank considerably to €413,000 in Q4, compared to €12.5 million in operating profit in Q4 2022. Fenix posted a net loss of €6.8 million, a loss of €0.51 a share, in the 2023 fourth quarter, compared to net income of €6.0 million, or €0.45, in the 2022 fourth quarter.

“We have ended another quarter of strange trading,” said Fenix Group Chairman of the Board Martin Nordin in his comments to investors at year-end. “The quarter started in the same way Q3 ended. There was very warm weather in Europe, which meant that a major part of the seasonal sales was lost. It is obvious that the trading in the industry was driven by large inventories in the retail part of the business, general liquidity problems and heavy discounts again. As usual, Christmas sales were hurt by people shopping on discounts during Black Friday and Cyber Monday. However, this year, there was a slower-than-usual lead-in of full-price sales due to early discounting and a greater hangover to full-price sales as Cyber [Monday] turned into weeks of promotional sales. As usual, we did not participate in this in any major way which protected our margin, but with a very high likelihood hurt our sales.

He also noted that in recent years the fourth quarter has shown very good sales growth. ”

“It is not very unlikely that growth expectations were set too high,” he admitted.

“What is encouraging is that the Friluft Group only decreased by 2.9 percent,” he added. “Most of the drop in sales came from our wholesale business in Brands and Global Sales. A very encouraging fact is that, in comparison to last year, the direct-to-consumer sales, especially of Fjallraven, were better than the average of competing brands in our DTC channels. This leads us to believe that the inventory/liquidity problem among the retail businesses hampered the wholesale business quite a bit.”

He said these factors led to the operating result close to zero.

“Based on the insecurity in the market, as well as after having analyzed our cost structure, we decided to lower our cost through savings measures,” he offered. “In total, we have taken one-time costs during Q4 of €10.3 million.

Nordin said this includes the following:

- Extraordinary write-down of inventory in the North American business, €3.2 million;

- Restructuring of shop network including closures, €1.85 million;

- Write-down of IT investments deemed out of life prematurely, €2.5 million; and

- Other costs for restructuring, €2.3 million.

“We expect these measures will lower our cost with about €7 million for 2024 and onwards,” he said.

In terms of sales in the Americas, Nordin said the business was also affected by the weaker dollar.

“The market still showed a slight growth for the whole year in local currency,” he noted. “The U.S. was, in Q4, hit more by large inventory and a sluggish retail trade which has been confirmed in the reports of other companies operating in our industry.”

He said there were some exceptions to the generally bad trading climate. Canada, for example, continued to recover, showing healthy growth. Nordin also noted the JV in China continued its recovery after COVID-19 and showed record Q4 sales and profit, “as well as for the whole year.”

Brands

The company’s Brands segment, which includes Fjällräven, Royal Robbins, Hanwag, and Fenix Outdoor, had sales of €47.3 million in the fourth quarter, falling 14.8 percent from €55.4 million in the prior-year fourth quarter. The company said there were lower sales across all major markets.

Gross margin in the segment was said to be hit by stock write-downs and higher customs affected by a shift in product mix.

The operating loss was €1.5 million for the quarter, compared to €4.6 million operating profit in the prior-year quarter. The Brands segment has taken almost €5.5 million of the extraordinary expenses to restructure parts of the shop network, but Nordin said it is also related to the increase the company has been facing in other areas such as IT and digital projects.

“In terms of Brand performance, Hanwag is still feeling the decrease in volume in their key product segments as well as the high inventory in the retail leg,” Nordin shared. “Fjallraven is still experiencing the effect of high inventory in retail, but when we are watching the direct-to-consumer channels it still shows growth for the year even though the tough fourth quarter.”

Global Sales

Global sales had external net sales of €34.4 million in Q4, down from €47.1 million in Q4 2022. The segment’s operating profit was €0.6 million, down sharply from €3.9 million in the prior year’s comparable period.

The bottom line was said to be positively driven by the Asian business, in particular the Chinese JV. The North American and European part of Global Sales was hit in the same way as the Brands business.

Frilufts

Nordin said the Frilufts operation had a mediocre Q4 and did not reach last year’s numbers. Globetrotter was reportedly hit more than the Nordics. Sweden did beat last year’s number in local currency as did the rest of the Nordics.

Fourth quarter sales at Frilufts was €98.5 million, a decrease of 2.9 percent from €101.4 million in Q4 2022. EBIT at Frilufts was €5.7 million, compared to €6.0 million in the prior-year quarter.

Nordin said the Norwegian operation showed a “positive development” but is still losing money. He said the small UK operation also struggled in the tough market but is still profitable.

For the full year, Frilufts sales were €352.1 million, growth of 1.2 percent.

“It should also be noted that in terms of channels, brick-and-mortar sales performed better than the digital channels both in the quarter as well as for the year,” Nordin added.

Digital/Direct-to-Consumer

Fourth quarter Direct-to-Consumer (DTC) sales were €136.1 million, down 2.3 percent from €139.3 million in Q4 2022.

- Digital DTC sales were reported at €45.2 million, down 4.4 percent from €47.2 million in the prior-year quarter.

- Brick & Mortar delivered €91.0 million in sales in Q4, down 1.2 percent versus the €92.1 million contributed in Q4 2022.

- Digital represented 33.2 percent of DTC sales in Q4, compared to 33.9 percent in Q4 2022.

Full-year total DTC sales were €461.9 million, up just 1.6 percent from €455.6 million in full-year 2022 after increasing 14 percent in 2022.

- Digital was up 0.4 percent to €146.9 million.

- Brick & Mortar rose 2.2 percent to €315.1 million.

- Digital was 31.8 percent of DTC sales for the year, compared to 32.2 percent in full-year 2021.

Nordin reminded investors that he indicated a year ago that the numbers last year indicated a new balance in the retail area and it seems that the new proportions lay somewhere around 30 percent to 35 percent digital versus brick-and-mortar.

“It should be said, however, that there is a difference between markets as well as types of stores and retail,” he added this year.

“This should in no way indicate that we believe that the digital transformations have stopped, rather, it creates a baseline for how we will approach our investments and cost structure going forward,” he said in last year’s investor letter.

Looking Ahead

“We are facing a very challenging market in 2024,” Nordin shared. “A lot of retailers have financial challenges, which means somewhat lower pre-orders than normal. They are counting more on re-orders from the brands. There are also some larger retailers that have been sold and have gone into reconstruction. The order books are okay, but growth will have to come from re-orders as well as our own DTC channels.”

He went on to say they believe that Q1 2024 will be a bit tougher for the wholesale part of the business, as the retailers are less inclined to take on inventory.

“Retail, on the other hand, has started quite well in 2024, especially as the cold weather in the Nordics had a positive effect on sales during January,” he noted.

In terms of trends, Nordin said several brands are outperforming others at this stage. He said those brands are focusing more on outdoor as a lifestyle in general, so-called “outdoor fashion.”

“If this will be a paradigm shift for the industry, it is still to be seen,” he suggested.

He said that other brands that are probably outperforming, at least from percentage growth, are some direct-to-consumer brands that are purely digital.

“Their complete control of their channels gives them an advantage from some perspective,” he said. “For example, they do not have to worry about their retailer’s reaction to price changes, etc. This gives them more price flexibility. We are NOT intending to go only digital as we still believe a real outdoor brand needs to be able to face full comparative and physical competition. We will, however, while being respectful of our retailers, put more focus on our brand store concepts and direct-to-consumer channels as a complement to our retail customers.”

Nordin went on to say that the last few quarters indicate that the company has been “somewhat frivolous” with its investments and costs. He added that they took measures and added costs in Q4 to enable the company to rectify these mistakes.

“We believe that the measures taken will decrease our costs already in 2024 with €7 million,” Nordin noted. “The new climate, with real interest rates again, also means that we have launched higher hurdles for investments. We are also refining our operations by investing in ERP system for the Brands and Global Sales segments, which we think will fine-tune and make our operation more efficient. The automation of our new warehouse operation in Ludwigslust is proceeding according to plan, but we do not believe we will reap the benefits from it until the earliest late 2024.”

Nordin said the company strongly believes that the over-inventory situation in the retail leg will have improved during Q2 and will mean an improvement in sales for wholesale during the second quarter.

“We saw that our re-order rate during July and August in 2023 was greatly improved compared to 2022, which means there is a possible shortage of goods in the market,” he opined. “We also need to keep in mind that there is also a possibility of a hangover for the industry in general due to the excessive growth experienced during COVID. There is also, as mentioned earlier, the issue of financial health among retailers.”

He said he believes Fenix will start to see a decrease in inventory measured on same-time-of-year-levels for the group starting end of the first quarter, so the focus for this year will be sales and cost control.

Fourth Quarter Results by Segment and Geographic Region

Image, data and charts courtesy Fenix Outdoor International AG