Boston Consulting Group (BCG) has offered its take on the 2024 Holiday selling season, suggesting that holiday cheer will be present but measured for U.S. retailers.

“It’s a different kind of year,” BCG wrote in its 2024 Holiday Outlook Survey summary. “On one hand, signs point to strong consumer spending; however, on the other hand, there are factors that will add a few twists and turns to this year’s calendar.

“While consumers will have divided attention in the coming months, retailers across all channels should ready the sleigh, because conditions call for a fast, exhilarating ride as shopping begins,” said BCG.

Spending Will Grow, but Modestly

BCG gathered insights from U.S. consumers and credit card data to compile its Holiday Outlook and noted in its summary that the growth outlook is mixed. “While just over a quarter of consumers (28 percent) plan to spend more than they did last year, just over a quarter (27 percent) plan to spend less—and just under a half (45 percent) plan to spend the same,” BCG observed.

The company said several factors contribute to this modest growth outlook.

“On one hand, real consumption has continued to grow in the post-pandemic era, and American household incomes and balance sheets are strong relative to historical levels. Moreover, both job growth and income growth are at similar levels to the pre-pandemic economy,” BCG continued.

But BCG also said other factors will keep the cheer in check:

- Despite positive indicators of economic growth, consumer sentiment has fallen over the past two years.

- Ongoing geopolitical tensions, global military conflicts and the upcoming 2024 presidential election have created an environment of split attention for U.S. consumers.

- High inflation, even with its recent cooling, has led to peak prices for staple goods, tightening budgets for holiday shopping and causing more intentional channel selection and deal-seeking during this period.

- Households may play it safe this holiday season but still spend as much as, or modestly more than, last year.

The 2024 Holiday Retail Calendar Adds Twists, Turns and Speed

BCG wrote that the Holiday selling season also has new twists and turns this year, courtesy of the calendar.

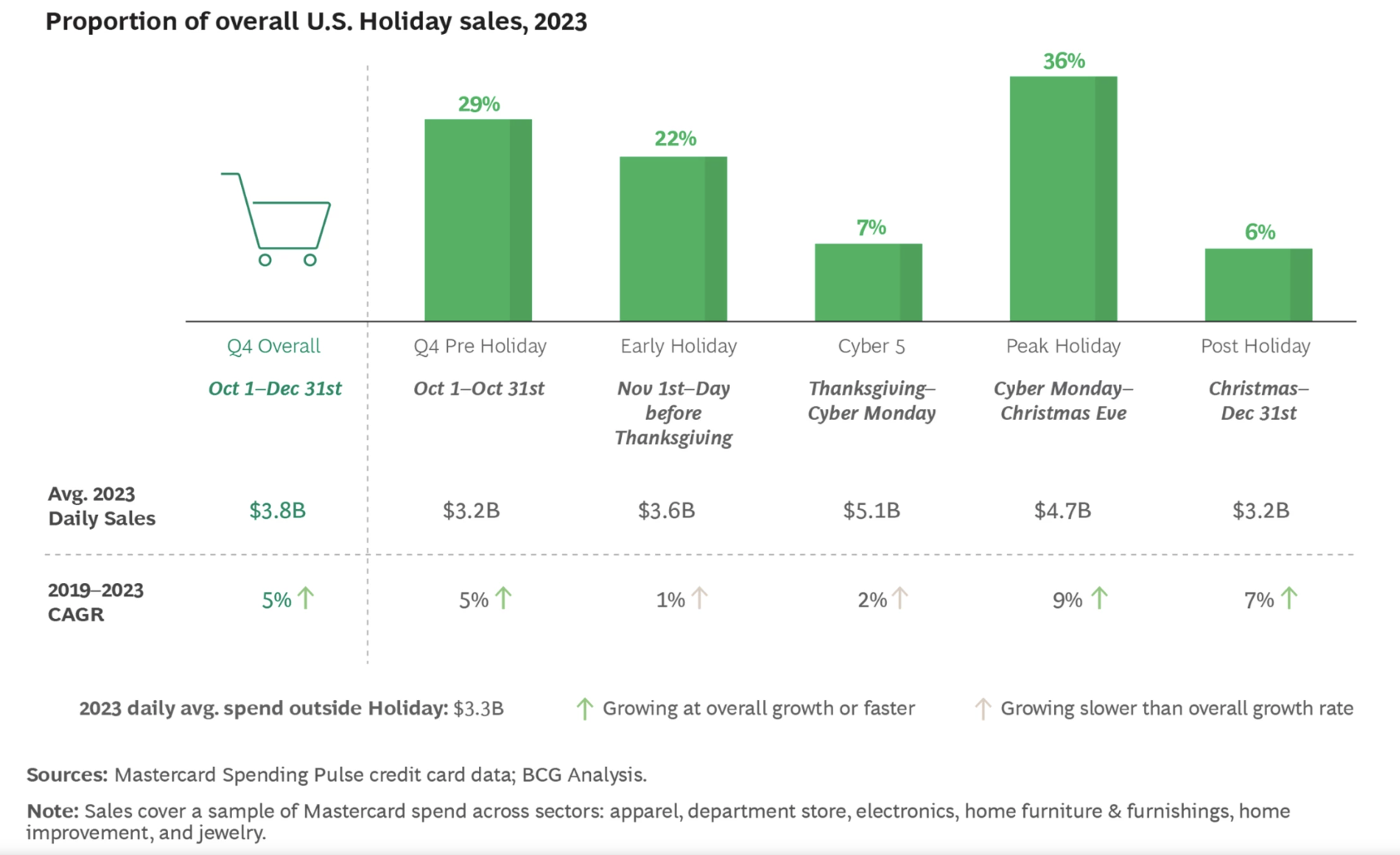

BCG defines the holiday season in five periods, as follows:

In 2023, consumers completed over 50 percent of their Holiday shopping before Thanksgiving. However, the peak Holiday period (after Cyber Monday through Christmas Eve) was still the busiest, with 36 percent of shopping.

This year’s late Thanksgiving leaves only 27 days between Thanksgiving and Christmas—five fewer shopping days than last year. Hanukkah is also later relative to 2023.

Second, BCG pointed to the U.S. presidential election that will take place in early November.

“Marketers are keenly aware of factors typical of the lead-up to major elections, including a crowded media market and higher costs due to increased competition,” BCG said. “These factors are now in full swing, as the election is already contracting supply and boosting prices for the best media spots likely to draw consumer attention. As a result, consumers’ attention will indeed be fragmented, with many less likely to think about their holiday shopping lists until their votes are in.”

However, the company said that historical precedent suggests that the election is unlikely to drive a contraction in consumer spending, no matter which candidate wins. Why? BCG said the answer lies with a nuanced distinction: the same circumstances can affect consumer confidence differently from actual consumer spending.

“Consider some notable events in recent history that affected consumer confidence: the financial crisis, the pandemic, and the last two presidential elections,” BCG offered. “Of these four, only two triggered decreases in consumer spending—the financial crisis and the pandemic. In both cases, the drop in consumer confidence was bipartisan, and spending took a meaningful hit. By contrast, during the last two elections, consumer confidence decreases were partisan rather than bipartisan—and consumer spending grew following both. Given this precedent, it is reasonable to predict that the election will have little ultimate impact on consumer spending, regardless of the outcome—but it could affect who is doing the spending, and when.”

In light of these calendar twists and turns, BCG recommends that retailers keep three things in mind:

- Expect a distinct early peak in spending ahead of Black Friday and Cyber Weekend. These weeks are a must-win period for retailers.

- The compressed peak season, the desire to wait out higher media costs around the election, and fewer days between Thanksgiving and Christmas could create more active media and promo competition during the peak selling season.

- Winning strategies will be multi-faceted throughout the Holiday season, with the first tactics deployed in October and a highly responsive approach during peak December shopping days.

Shifting from Macro Timing Considerations to Micro Consumer Behavior

BCG observed that among the many trends that emerged during the pandemic was a significant acceleration in weekday holiday shopping, which led to weekdays overtaking weekends in daily spending. This trend saw a reversal last year during the 2023 holiday shopping season, during which consumer shopping appeared to return to ‘normal‘, with weekday spending dropping slightly below Saturday and Sunday levels. Weekend shopping returned to the U.S. consumer’s routine and is expected to continue through the 2024 holiday season.

“But retailers shouldn’t underestimate the importance of weekday shopping,” BCG wrote. “E-commerce has continued to grow, and the prominence of online channels is 1.4x higher during weekdays. This raises the stakes for digital experiences Monday through Friday. With online shopping comprising 40 percent of weekday shopping, it is quickly approaching the status of primary channel for consumers making weekday purchases, and we wouldn’t be surprised to see online exceed 50 percent of weekday spending in the next 2-4 shopping seasons. The takeaway? Winning the holiday season and achieving growth targets in 2024 and beyond will rely more on weekday success online than on record in-store days on the weekend.”

Evolving Shopping Behavior and Channel Landscape Will Lead to Mixed Results

BCG noted over the past three years that some retail channels have struggled to keep pace with market growth while others have accelerated unexpectedly.

“The pandemic era (2019 to 2022) saw modest customer growth for direct-from-brand stores and specialty retailers. But both channels experienced significant acceleration last holiday season, and, continuing this trend, we expect them to continue to outgrow the total retail landscape this year,” the company explained.

BCG said “disruptor channels” have found a solid foothold over the past two years.

“While they remain small, both social media commerce and online marketplaces specialized in deals and gamification such as Temu and Shein are becoming increasingly formidable players,” BCG offered, “Timing matters, though—direct, social media and emerging marketplace channels see the most strength early in the holiday shopping season, when early shoppers are seeking the ‘just right’ gift and often prefer to buy directly from brands.”

The company said that later in the Holiday season, consumers will insist on the predictable fulfillment and competitive prices that mega-retailers and platforms are known for. Leaning into a fast-fulfillment advantage can help capitalize on consumers seeking rapid shipping to ensure gifts arrive on time.

“Our view is that holiday performance for consumer brands and for retailers will depend on well-timed execution, recognizing that shoppers have different missions across the full holiday season. Throughout the season, deal seeking will be a core behavior, in part a reaction to the higher prices across grocery and other non-discretionary categories,” the company concluded.

Go Here to access Boston Consulting Group’s 2024 Holiday Outlook Survey.

Image, data and graphics courtesy Boston Consulting Group