BRP, Inc., the parent of the Ski-Doo, Sea-Doo, and Lynx power sports brands, maintained its focus on reducing network inventory levels during the fiscal second quarter ended July 31, 2024. This resulted in a decrease in the volume of product shipments, consequently leading to a decline in revenues compared to the comparable period last year.

The decrease in the volume of shipments, higher sales programs due to increased promotional intensity, and decreased leverage of fixed costs due to reduced shipments have led to a decrease in gross profit and gross profit margin year-over-year. A favorable product mix partially offset this decrease.

The company’s North American quarterly retail sales for Powersport Products were down 18 percent for the three-month period ended July 31, 2024. The decrease was mainly attributed to softer industry demand in seasonal and year-round product.

Revenues

The company reported consolidated revenues decreased by $936.1 million, or 33.7 percent, to $1.84 billion for the second quarter, compared to $2.78 billion for the prior-year Q2 period. The revenue decrease was primarily due to a lower volume sold across all product lines, as the company focused on reducing network inventory levels and higher sales programs. The decrease was partially offset by a favorable product mix across most product lines. The decrease includes a favorable foreign exchange rate variation of $29 million.

- Year-Round Products: Revenues from Year-Round Products, which comprised 54 percent of Q2 revenues, decreased by $476.6 million, or 32.6 percent, to $985.0 million for the second quarter, compared to $1.46 billion for the prior-year Q2 period. The decrease in revenues was primarily attributable to a lower volume sold across all product lines, as the company maintained its focus on reducing network inventory levels and higher sales programs. The decrease was partially offset by a favorable product mix of SSV and 3WV. The decrease includes a favorable foreign exchange rate variation of $18 million.

- Seasonal Products: Revenues from Seasonal Products, which comprised 29 percent of Q2 revenues, decreased by $355.7 million, or 39.6 percent, to $541.8 million for the second quarter, compared to $897.5 million for the prior-year Q2 period. The decrease in revenues was primarily attributable to a lower volume sold across all product lines, as the company maintained its focus on reducing network inventory levels and higher sales programs. The decrease was partially offset by a favorable product mix across all product lines. The decrease includes a favorable foreign exchange rate variation of $8 million.

- Powersports PA&A and OEM Engines: Revenues from Powersports PA&A and OEM Engines, 14 percent of Q2 revenues, decreased by $35.9 million, or 12.2 percent, to $258.3 million for the second quarter, compared to $294.2 million for the prior-year Q2 period. The revenue decrease was primarily attributable to a lower volume sold due to a high network inventory level in Snowmobile and a decrease in retail in other product lines. The decrease also includes a favorable foreign exchange rate variation of $3 million.

- Marine: Revenues from the Marine segment, representing 3 percent of Q2 revenues, decreased by $67.5 million, or 53.2 percent, to $59.4 million for the second quarter, compared to $126.9 million for the prior-year Q2 period. The revenue decrease was mainly attributable to a lower volume sold due to high dealer inventory, softer consumer demand in the industry, and higher sales programs.

The company said that it included inter-segment transactions in the analysis.

North American Retail Sales

The company’s North American retail sales for Powersports Products decreased by 18 percent for the second quarter compared to the same period last year. The decrease is mainly explained by softer industry demand for seasonal and year-round products.

North American Year-Round Products retail sales decreased on a percentage basis in the low teens compared to the prior-year Q2 period. In comparison, the Year-Round Products industry decreased on a percentage basis in the mid-single-digits over the same period.

North American Seasonal Products retail sales decreased on a percentage basis in the high-twenties range compared to the prior-year Q2 period. The Seasonal Products industry decreased on a percentage basis in the high-teens range over the same period.

The company’s North American retail sales for Marine Products increased by 35 percent compared to the prior-year Q2 period, given a low retail volume period as the basis of comparison.

Income Statement Summary

Gross profit decreased by $321.1 million, or 46.0 percent, to $376.5 million for the second quarter, compared to $697.6 million for the prior-year Q2 period. Gross profit margin percentage decreased by 470 basis points to 20.4 percent from 25.1 percent for the prior-year Q2 period. The decreases in gross profit and gross profit margin percentage resulted from a lower volume sold, higher sales programs, and decreased leverage of fixed costs due to reduced shipments. The decrease was partially offset by a favorable product mix across most product lines. The decrease in gross profit includes a favorable foreign exchange rate variation of $9 million.

Operating expenses decreased by $16.7 million, or 5.2 percent, to $302.1 million for the second quarter, compared to $318.8 million for the prior-year Q2 period. The decrease in operating expenses was mainly attributable to lower R&D expenses due to the recognition of R&D subsidies from prior years. The decrease was partially offset by restructuring and reorganization costs. The decrease in operating expenses includes a favorable foreign exchange rate variation of $2 million.

Normalized EBITDA decreased by $274.6 million, or 58.0 percent, to $198.5 million for the second quarter, compared to $473.1 million for the prior-year Q2 period. The decrease in normalized EBITDA [1] was primarily due to lower gross margin, partially offset by lower operating expenses.

Net income decreased by $331.5 million to $7.2 million for the second quarter, compared to $338.7 million for the prior-year Q2 period. The decrease in net income was said to be primarily due to a lower operating income resulting from a lower gross margin, in addition to an increase in financing costs and an unfavorable foreign exchange rate variation on the U.S. denominated long-term debt. The decrease was partially offset by a lower income tax expense.

“Our results were in line with expectations and reflect our ongoing focus on reducing network inventory to maintain our dealer value proposition. We have made great strides on that front, but the retail environment is more challenging with the economic context pressuring consumer demand. As such, our priority is to continue to proactively manage production and inventory levels, which leads us to revise our year-end guidance,” said José Boisjoli, president and CEO of BRP.

Fiscal 2024 First Half (H1) Summary

- Revenues decreased by $1.33 billion, or 25.6 percent, to $3.87 billion for the fiscal 2024 first half, compared to $5.21 billion for the prior-year H1 period.

- Normalized EBITDA decreased by $404.5 million, or 47.6 percent, to $445.7 million for the fiscal 2024 first half, compared to $850.2 million for the prior-year H1 period.

- Net income (loss) decreased by $493.4 million to a loss of 0.2 million for the fiscal 2024 first half, compared to net income of $493.2 million for the prior-year H1 period.

Liquidity and Capital Resources

The company generated net cash flows from operating activities totaling $253.0 million for the fiscal 2024 first half compared to net cash flows of $748.2 million for the six-month period ended July 31, 2023. The decrease was mainly due to lower profitability and unfavorable changes in working capital, partially offset by lower income taxes paid. The unfavorable changes in working capital were reportedly the result of maintaining higher provisions, which reflected the industry’s promotional intensity, and a decrease in trade payables due to a reduction in purchasing activities.

The company invested $180.7 million of its liquidity in capital expenditures to introduce new products and modernize its software infrastructure to support future growth.

During the first half, the company also returned $246.2 million to its shareholders through quarterly dividend payouts and share repurchase programs.

Dividend

On September 5, 2024, the company’s Board of Directors declared a quarterly dividend of $0.21 per share for holders of its multiple voting shares and subordinate voting shares. The dividend will be paid on October 11, 2024, to shareholders of record at the close of business on September 27, 2024.

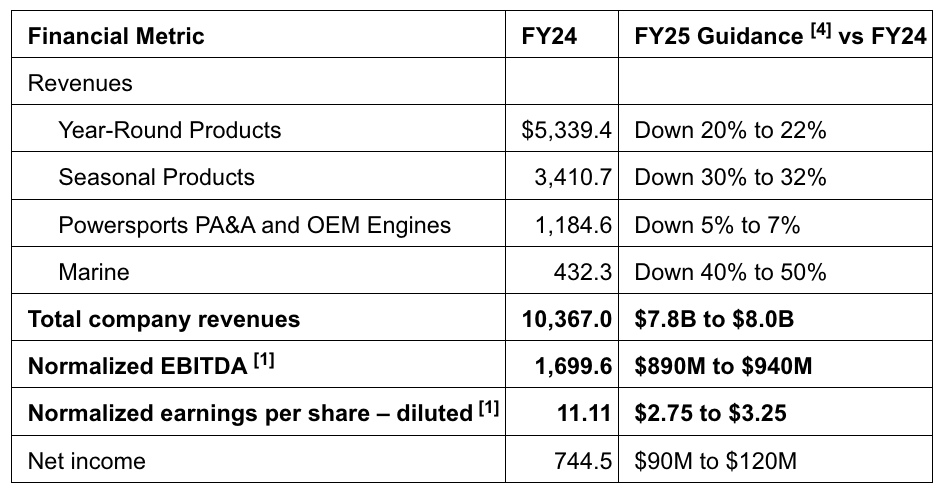

Fiscal 2025 Full-Year Guidance

BRP, Inc. has updated FY25 guidance as follows:

Fiscal Third Quarter Outlook

BRP, Inc. expects Q3 Fiscal 2025 Normalized diluted earnings per share to be up between high-single digit to low-teens percentage versus Q2 Fiscal 2025.

Image courtesy Ski-Doo