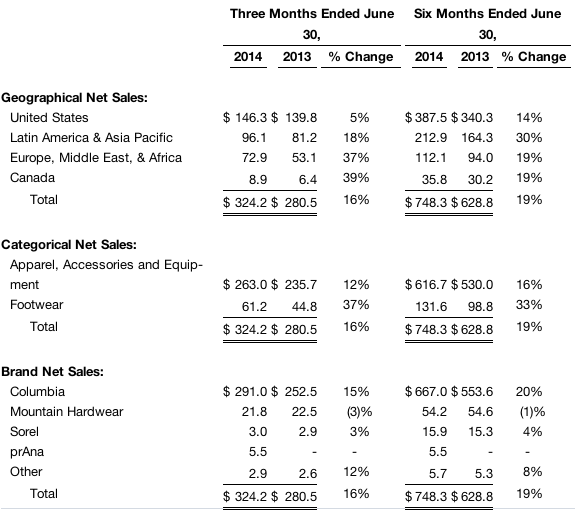

Columbia Sportswear Co. reported net sales grew 16 percent in the second quarter to $324.2 million compared with sales of $280.5 million for the same period in 2013, including a less than 1 percentage point benefit from changes in currency exchange rates.

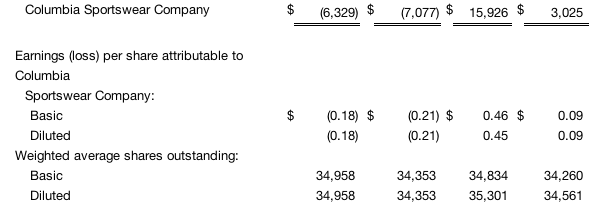

Second quarter 2014 net loss totaled $6.3 million, or 18 cents a share, including a net tax benefit of $5.6 million, or 16 cents per share, resulting from the favorable resolution of uncertain tax positions from prior years. During the quarter, the company incurred approximately $3.4 million of non-recurring transaction costs related to the prAna acquisition, and approximately $1.3 million in amortization of certain acquired assets and other integration costs which, combined, equated to $2.9 million net of tax, or $(0.08) per share. Second quarter 2013 net loss totaled $7.1 million, or $(0.21) per share.

Tim Boyle, Columbia’s president and chief executive officer, commented, “We are very pleased with our performance through the first half of 2014 and anticipate strong Columbia and Sorel brand momentum in the second half, particularly in North America. In addition, our brands continued to stabilize in the key Europe-direct markets that are a focal point of our ongoing efforts to drive renewed growth and improved profitability.

“With the successful completion of our previously announced acquisition of prAna during the second quarter, we enter the second half of 2014 with a new exciting brand in our portfolio, which we expect to be accretive in 2015.”

Boyle concluded, “Our first half performance, coupled with the confidence we have in our brands, our line-up of innovative products, and our global team, led us to increase our full year 2014 financial outlook. We believe we are beginning to make meaningful, sustainable progress toward our goal of improving our profitability.”

Second Quarter Results

The second quarter is the company’s smallest revenue quarter, historically accounting for a mid-teens percentage of annual net sales. As a result, regional, category and brand net sales results often produce large percentage variances in relation to the prior year’s comparable period due to the small base of comparison and shifts in the timing of shipments.

Net sales in the U.S. increased $6.5 million, or 5 percent, to $146.3 million, including $5.5 million of incremental prAna net sales. Latin America/Asia Pacific (LAAP) region net sales increased $14.9 million, or 18 percent, to $96.1 million, including incremental sales from the company’s new China joint venture and a neutral effect of changes in currency exchange rates. Europe/Middle East/Africa (EMEA) region net sales increased $19.8 million, or 37 percent, to $72.9 million, including a 2 percentage point benefit from changes in currency exchanges rates. Net sales in Canada increased $2.5 million, or 39 percent, to $8.9 million, including a 10 percentage point negative effect from changes in currency exchanges rates.

Apparel, Accessories & Equipment net sales increased $27.3 million, or 12 percent, to $263.0 million. Footwear net sales increased $16.4 million, or 37 percent, to $61.2 million.

Columbia brand net sales increased $38.5 million, or 15 percent, to $291.0 million, and the newly-acquired prAna brand contributed $5.5 million of incremental net sales.

Balance Sheet

During the second quarter, the company completed its previously announced acquisition of prAna Living LLC for $188.5 million, net of acquired cash. The company ended the second quarter with $394.4 million in cash and short-term investments, compared with $430.6 million at June 30, 2013. Approximately 54 percent of cash and short-term investments was held in foreign jurisdictions where a repatriation of those funds to the United States would likely result in a significant tax cost to the company.

Consolidated inventories of $456.4 million at June 30, 2014 were approximately 8 percent higher than the $423.8 million balance at June 30, 2013.

Updated 2014 Financial Outlook

All projections related to anticipated future results are forward-looking in nature and are subject to risks and uncertainties that may cause actual results to differ, perhaps materially. The company’s annual net sales are weighted more heavily toward the second half of the fiscal year, while operating expenses are more equally distributed, resulting in a highly seasonal profitability pattern weighted toward the second half of the fiscal year.

All per-share amounts in the following outlook are based on projected outstanding shares prior to the effect of the pending two-for-one stock split scheduled to take effect after the close of business on September 26, 2014.

Anticipated Fiscal 2014 Effects of prAna Acquisition

The company expects to recognize incremental prAna net sales of approximately $55 million during fiscal year 2014, which is expected to contribute low double-digit operating margin to consolidated 2014 results, excluding one-time transaction costs of approximately $3.4 million and purchase accounting amortization and other integration costs expected to total approximately $8.0 million. Combined, these excluded costs are expected to equate to approximately $7.1 million net of tax, or $(0.20) per diluted share.

Consolidated FY2014 Financial Outlook

Including prAna’s anticipated operating results for the June through December period, as well as the non-recurring transaction costs and amortization of certain acquired assets and other integration costs described above, we expect our full year 2014 financial results to include:

- global net sales of approximately $2.01 billion to $2.04 billion, representing 19 to 21 percent growth over 2013 net sales of $1.68 billion. The anticipated growth of approximately $320 million to $355 million includes incremental net sales of approximately $155 million from the new China JV and approximately $55 million from the newly-acquired prAna brand, coupled with high single-digit percentage organic growth;

- gross margin expansion of up to 75 basis points compared with 2013;

- selling, general and administrative expense leverage of up to 20 basis points compared with 2013;

- licensing income of approximately $6 million;

- operating margin of up to 8.3 percent, compared with 2013 operating margin of 7.8 percent;

- adjusted operating margin of 8.8 percent, excluding prAna’s anticipated operating results, approximately $3.4 million of non-recurring transaction costs and $8.0 million in amortization of certain acquired assets and other integration costs related to the prAna acquisition. This compares to 2013 adjusted operating margin of 8.4 percent, which excluded a $9.0 million non-cash asset impairment charge;

- a full year tax rate of approximately 27.0 percent, which could differ based on the resolution and status of tax uncertainties, the geographic mix of pre-tax income, and other discrete events that may occur during the year;

- net income after non-controlling interest of approximately $114 million to $120 million, or $3.22 to $3.38 per diluted share, compared to $94.3 million, or $2.72 per diluted share, in 2013. Fiscal year 2014 net income includes the expected effects of:

- one-time acquisition costs and first-year purchase accounting amortization and integration costs related to the prAna acquisition totaling approximately $7.1 million net of tax, or $(0.20) per diluted share;

- approximately $0.15 incremental diluted earnings per share from the new China JV, after interest, taxes and non-controlling interest.