The TJX Companies, Inc., the parent company of TJ Maxx, Marshall’s, Sierra Trading, and HomeGoods, reported net sales for the first quarter of Fiscal 2025 were $12.5 billion, an increase of 6 percent versus the first quarter of Fiscal 2024. Consolidated comparable store sales increased 3 percent for the quarter ended May 4.

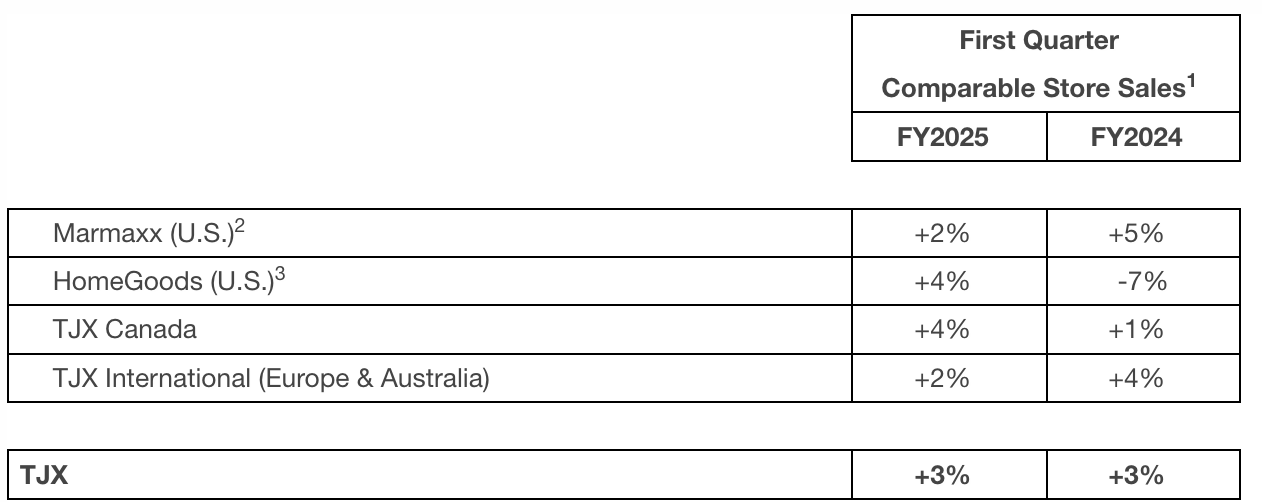

Comparable Store Sales by Division

The company’s comparable store sales by division for the first quarter were as follows:

“I am very pleased with our first quarter performance. Overall comp store sales increased 3 percent, at the high-end of our plan, and both profitability and earnings per share were well above our expectations,” said Ernie Herrman, CEO and president of The TJX Companies, Inc. “Our teams across the company executed on our initiatives and were laser-focused on delivering consumers exciting values on great brands and fashions and a treasure-hunt shopping experience, every day. We saw comp sales growth at every division entirely driven by customer transactions, which underscores the strength of our value proposition. This also gives us confidence in our ability to gain market share across all of our geographies. The second quarter is off to a good start and we see numerous opportunities for our business for the balance of the year that we plan to pursue. Longer term, we are excited about the potential we see to drive customer transactions and sales, capture additional market share, and increase the profitability of TJX.”

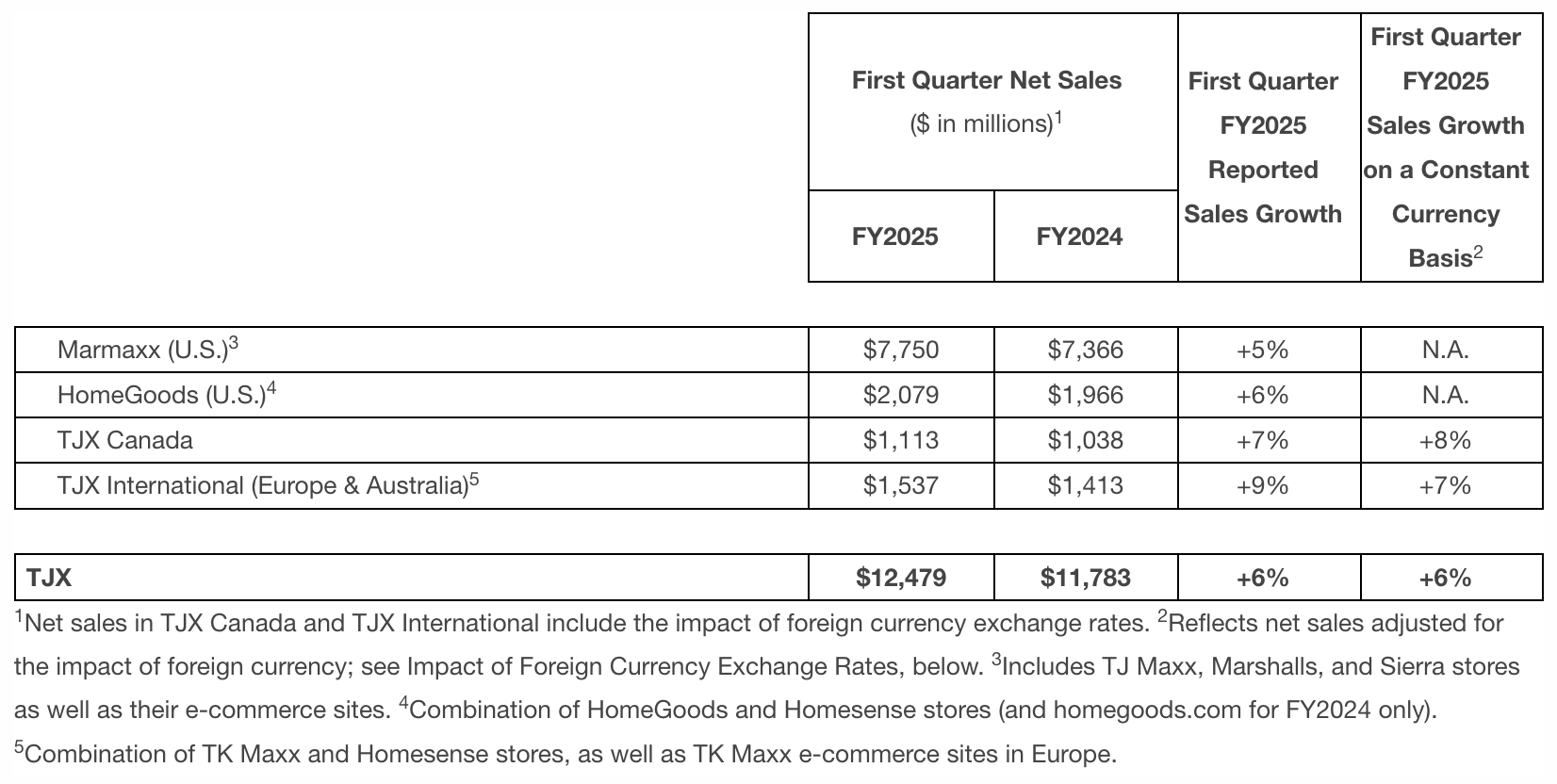

Net Sales by Division

The company’s net sales by division for the first quarter were as follows:

Margins

The company’s pretax profit margin was 11.1 percent on net sales in Q1, up 80 basis points versus last year’s first quarter pretax profit margin of 10.3 percent. This was said to be well above the company’s plan primarily due to a larger-than-expected benefit from lower freight costs, a reserve release, and higher net interest income.

Gross profit margin for the first quarter was 30.0 percent of net sales, a 110 basis point increase versus the first quarter of Fiscal 2024. A benefit from lower freight costs and favorable markdowns drove this year-over-year increase.

Selling, general and administrative (SG&A) costs as a percentage of sales for the first quarter were 19.2 percent, a 20 basis point increase versus the first quarter of Fiscal 2024. This year-over-year increase was due to incremental store wage and payroll costs.

Net interest income benefitted the first quarter of Fiscal 2025 pretax profit margin by 0.1 percentage point versus the prior year.

Net income for the first quarter was $1.1 billion, 93 cents per diluted share, up 22 percent versus 76 cents per share in the first quarter of Fiscal 2024.

Impact of Foreign Currency Exchange Rates

Changes in foreign currency exchange rates affect the translation of sales and earnings of the company’s international businesses into U.S. dollars for financial reporting purposes. In addition, of an ordinary course, inventory-related hedging instruments are marked to market at the end of each quarter. Changes in currency exchange rates can have a material effect on the magnitude of these translations and adjustments when there is significant volatility in currency exchange rates. Given the company’s global operations, to facilitate comparability, the company has provided sales growth and inventory on a constant currency basis, which assumes a constant exchange rate between periods for translation based on the rate in effect for the prior period.

The movement in foreign currency exchange rates had a neutral impact on the company’s net sales growth in the first quarter of Fiscal 2025 versus the prior year. The overall net impact of foreign currency exchange rates had a 1 cent positive impact on first quarter Fiscal 2025 diluted earnings per share.

The impact of the foreign currency exchange rate on diluted earnings per share does not include the impact of currency exchange rates on various transactions, which the company refers to as “transactional foreign exchange.”

Inventory

Total inventories as of May 4, 2024 were $6.2 billion, compared to $6.4 billion at the end of the first quarter of Fiscal 2024. Consolidated inventories per-store at quarter-end, including distribution centers, but excluding inventory in transit, the company’s e-commerce sites, and Sierra stores were down 5 percent on a reported and constant-currency basis. Inventory on a constant-currency basis reflects inventory adjusted for the impact of foreign currency exchange rates, if any, as described above. The company is pleased with its in-store inventory levels and is confident it is well-positioned to take advantage of the outstanding availability of quality, branded merchandise in the marketplace and flow fresh goods to its stores and online throughout the spring and summer.

Cash and Shareholder Distributions

For the first quarter of Fiscal 2025, the company generated $737 million of operating cash flow and ended the quarter with $5.1 billion in cash.

During the first quarter of Fiscal 2025, the company returned $886 million to shareholders. The company repurchased $509 million of TJX stock, retiring 5.3 million shares, and paid $377 million in shareholder dividends during the quarter.

The company continues to expect to repurchase approximately $2.0 to $2.5 billion of TJX stock during the fiscal year ending February 1, 2025. The company may adjust the amount purchased under this plan up or down depending on various factors. The company remains committed to returning cash to its shareholders while continuing to invest in the business to support the near- and long-term growth of TJX.

Second Quarter and Full Year Fiscal 2025 Outlook

For the second quarter of Fiscal 2025, the company is planning consolidated comparable store sales to be up 2 percent to 3 percent, pretax profit margin to be in the range of 10.4 percent to 10.5 percent, and diluted earnings per share to be in the range of 88 cents to 90 cents.

For the full year Fiscal 2025, the company continues to plan consolidated comparable store sales to be up 2 percent to 3 percent. The company is increasing its outlook for pretax profit margin to be in the range of 11.0 percent to 11.1 percent and increasing its diluted earnings per share outlook to be in the range of $4.03 to $4.09.

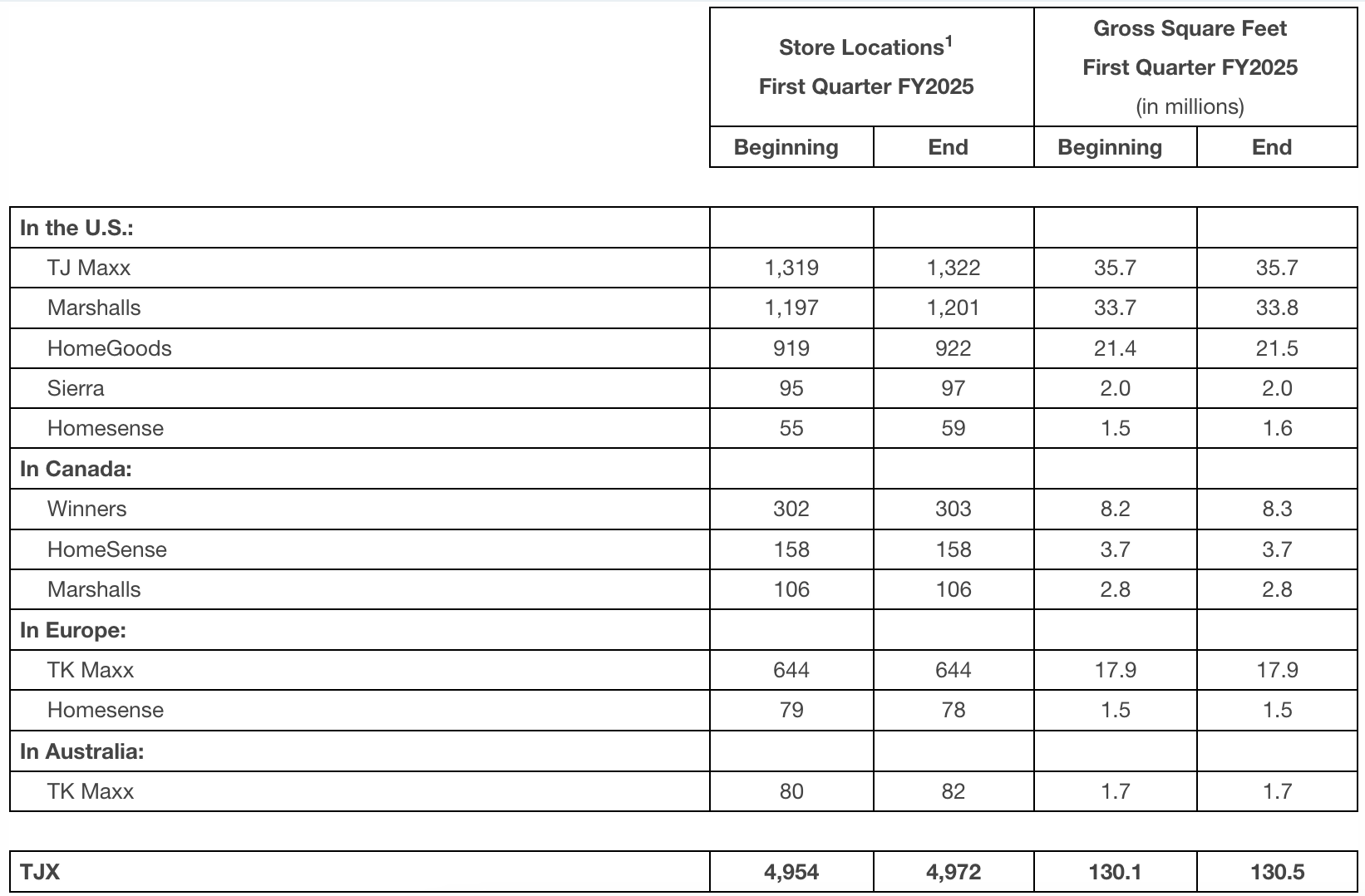

Stores by Concept

During the fiscal quarter ended May 4, 2024, the company increased its store count by 18 for a total of 4,972 stores and increased square footage by 0.3 percent versus the prior quarter.

Image courtesy TJX Cos.