Shoe Carnival Inc. reported second-quarter earnings that were below year-ago levels but well ahead of the pre-pandemic 2019 quarter. Sales were down 6 percent year over year. The off-price shoe chain reiterated its EPS guidance for the year.

Second Quarter Highlights Compared to 2019

- Net sales grew 16.4 percent with both store banners contributing.

- Based on results through the second quarter, Shoe Station banner sales are now expected to exceed previously announced full year expectations of $100 million by more than 10 percent.

- Gross profit margin increased 560 basis points.

- Operating income margin increased 660 basis points and at 12.4 percent was the sixth consecutive quarter in double-digits.

- Second quarter EPS of $1.04 (up 160 percent) and year-to-date EPS of $1.99 (up 131 percent) is on track to deliver previously announced full year guidance in the range of $3.95 to $4.15.

“The Shoe Carnival team delivered exceptional profitability in a challenging economic environment,” said Mark Worden, President and Chief Executive Officer. “The nearly $2.00 of EPS earned during the first half of 2022 is greater than any full year earnings in our 44 years of operation except for last year’s stimulus boosted results.”

“We are proud to deliver our sixth consecutive quarter of double-digit operating income margin and gross profit margin that expanded nearly 600 basis points versus pre-pandemic levels on both a quarterly and year-to-date basis. Contribution from the Shoe Station banner has exceeded initial expectations and we expect to realize additional synergies and to grow store count across both banners. We are optimistic about our long-term growth trajectory and delivering our profitability goals for 2022,” concluded Worden.

Shoe Station Update

Shoe Station operating results to date have exceeded management’s initial expectations. Previously announced expectations were $100 million of annual net sales and a 10 percent operating income margin. The company now anticipates the top-line sales target will be exceeded by more than 10 percent and bottom-line contribution will be in line with the company’s overall expected operating income margin of 11.4 percent to 11.6 percent. The company anticipates further supply chain and omnichannel synergies will be achieved by fiscal year end, with benefits realized in fiscal 2023.

Back-to-School Update

August merchandise sales through the beginning of the fourth week of August include the highest three-day sales achieved during any three days in the company’s history. August-to-date merchandise sales have increased in the mid-teens compared to 2019 and have decreased mid-single digits compared to 2021. Gross profit margin for August is expected to increase over 650 basis points compared to 2019. The August back-to-school shopping period drives over half of the company’s third quarter profitability.

Fiscal 2022 Earnings Outlook

Compared to 2019, EPS growth has accelerated through the first half of 2022, increasing 107 percent in the first quarter and 160 percent in the second quarter. These results, combined with the solid start to the third quarter, provide the foundation for the company’s sales and earnings outlook for fiscal 2022.

- EPS is reaffirmed to be in the range of $3.95 to $4.15, compared to a pre-pandemic annual high of $1.46 in 2019.

- Net sales are expected to be between $1.29 billion and $1.34 billion, up 24 percent to 29 percent compared to 2019.

- Gross profit margin is expected to be in a range of 36.6 percent to 36.7 percent, compared to 30.1 percent in 2019.

- Operating income margin is expected to be in a range of 11.4 percent to 11.6 percent, compared to 5.2 percent in 2019.

Merchandise Inventory

The company ended second quarter 2022 with inventory of $385.5 million, an increase of $48.6 million compared to second quarter 2019. Approximately 59 percent of the increase is inventory for the Shoe Station stores acquired last year or opened this year. The 14.4 percent increase in inventory is supportive of the 20.6 percent increase in net sales year-to-date compared to 2019 and the expectation of increases in sales for the remainder of the year. The number of weeks of sales in the second quarter ending inventory this year is slightly down compared to 2019.

Operating Results Compared to 2019

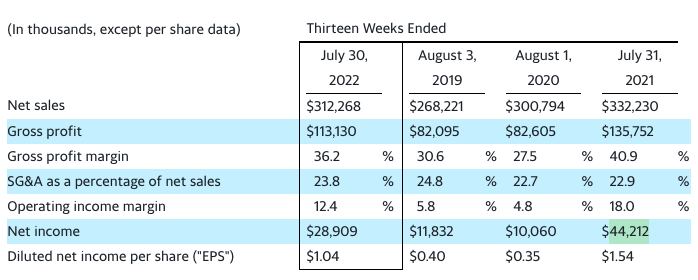

Second quarter 2022 net sales of $312.3 million increased $44.0 million, or 16.4 percent, compared to the pre-pandemic second quarter 2019, driven by contribution from Shoe Station stores and new customer acquisition at Shoe Carnival stores of 28 percent. Year-to-date net sales have increased $107.8 million, or 20.6 percent, compared to 2019, with both store banners contributing nearly equally to the year-to-date increase. Sales from the Shoe Station banner stores, acquired in December 2021, added net sales of $27.2 million for the quarter and $53.4 million year-to-date.

COVID-19-related manufacturing and supply chain disruptions significantly constrained the availability of athletic shoes. Based on weekly averages, athletic inventory was down 25.7 percent during the 2022 second quarter compared to 2019. These lower inventory levels contributed to decreased athletic sales in the quarter by 12.9 percent. This decrease was more than offset by a 30.8 percent increase in sales of non-athletic shoe categories, driving overall comparable store sales up 8.0 percent.

Second quarter 2022 gross profit margin was 36.2 percent, a 560 basis point increase compared to second quarter 2019. Merchandise margin would have increased over 800 basis points primarily due to increased customer relationship management capabilities, which have resulted in more targeted promotional pricing and higher average selling prices. However, inflationary impacts on transportation and fuel expenses partially offset the increase in merchandise margin and also increased the company’s distribution costs.

Operating income for second quarter 2022 was $38.8 million and was 12.4 percent of net sales, a 660 basis point increase compared to second quarter 2019.

Second quarter 2022 net income was $28.9 million, or $1.04 per diluted share, an increase of 160 percent compared to second quarter 2019.

Operating Results Compared to 2021

Net sales decreased $20.0 million, or 6.0 percent, compared to second quarter 2021 with a comparable store decline of 13.8 percent partially offset by sales from Shoe Station stores. The comparable store decline was primarily driven by lower athletic sales.

Gross profit margin decreased 470 basis points compared to second quarter 2021, primarily due to higher costs, including higher freight and fuel costs, and the de-leveraging effect of lower sales on buying, distribution and occupancy costs.

In second quarter 2021, operating income, net income and EPS were $59.7 million, $44.2 million, and $1.54, respectively.

Store Updates

Store count is on track to achieve 400 stores by the end of fiscal 2022. No store closures during fiscal 2022 are anticipated.

The company is currently modernizing its stores and plans to have over 50 percent of stores modernized by the summer of 2023 and the full program complete by the end of fiscal 2024.

Share Repurchase Program

As of July 30, 2022, the company had $29.5 million available for future repurchases under its share repurchase program, and during the second quarter no shares were repurchased.