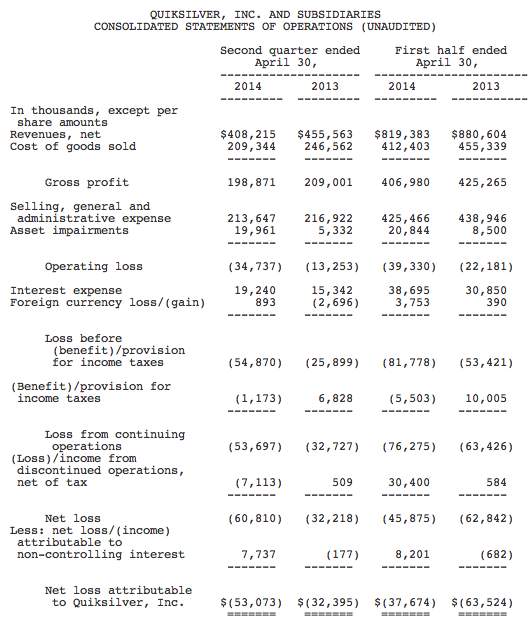

Quiksilver Inc., the parent of Quiksilver, Roxy and DC, reported its net loss swelled to $53.1 million, or 27 cents a share, in the second quarter from $32.4 million, or 20 cents, in part due to an an increase in asset impairments and a 9 percent revenue decline. Sales were down 16 percent on a currency-neutral basis in the Americas. The company also said it expects pro-forma adjusted EBITDA for the full year to come in below year-ago levels.

Quiksilver Inc., the parent of Quiksilver, Roxy and DC, reported its net loss swelled to $53.1 million, or 27 cents a share, in the second quarter from $32.4 million, or 20 cents, in part due to an an increase in asset impairments and a 9 percent revenue decline. Sales were down 16 percent on a currency-neutral basis in the Americas. The company also said it expects pro-forma adjusted EBITDA for the full year to come in below year-ago levels.

“We made progress on our Profit Improvement Plan,” said Andy Mooney, president and chief executive officer of Quiksilver, Inc. “During the second quarter, we again reduced our expense structure, increased sales in our direct to consumer channels and emerging markets, and drove improvements in gross margins. These improvements were offset by decreased net revenues in our wholesale channel, especially in the developed markets in North America and Europe. Consequently, pro-forma adjusted EBITDA decreased versus the prior year.”

All of the results presented below represent the company's continuing operations.

Please refer to the accompanying tables for a reconciliation of GAAP results from continuing operations to certain non-GAAP results from continuing operations, including pro-forma loss from continuing operations, pro-forma loss from continuing operations per share, adjusted EBITDA and pro-forma adjusted EBITDA, for all periods presented, net revenues in historical and constant currency, and a definition of the Company's emerging markets.

Second quarter review:

The company repoted the following comparisons of results of continuing operations for the second quarter of fiscal 2014 versus the second quarter of fiscal 2013.

- Net revenues were $408 million compared with $456 million, and were down 9 percent, or $42 million, in constant currency.

- Americas net revenues decreased 18 percent to $186 million from $226 million, and were down 16 percent in constant currency.

- EMEA net revenues decreased 2 percent to $162 million from $165 million, and were down 5 percent in constant currency.

- APAC net revenues decreased 6 percent to $60 million from $64 million, but were up 3 percent in constant currency.

Gross margin increased to 48.7 percent from 45.9 percent. The 280 basis point improvement in gross margin reflects the sales growth in our direct to consumer channels, reduced clearance activity in the wholesale channel of certain regions and benefits of licensing activities.

SG&A expense decreased $3 million to $214 million from $217 million, primarily due to reduced selling expenses associated with the decline in net revenues, reduced employee compensation expenses and event spending, partially offset by an increase in bad debt expense.

Asset impairments increased to $20 million from $5 million due to a $15 million write-down of Surfdome goodwill and intangible assets in connection with the reclassification of Surfdome from discontinued operations to continuing operations.

Pro-forma Adjusted EBITDA decreased to $12 million from $18 million.

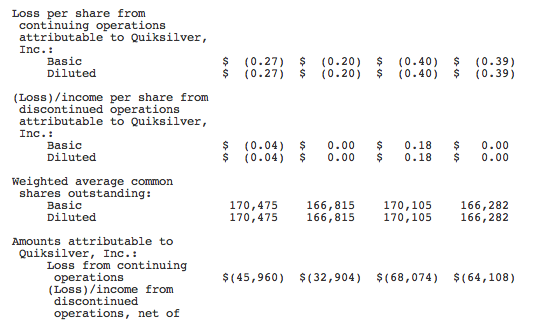

Net loss from continuing operations attributable to Quiksilver, Inc. was $46 million, or $0.27 per share, compared with $33 million, or $0.20 per share.

Pro-forma loss from continuing operations, which excludes the after-tax impact of restructuring and other special charges and non-cash asset impairments, increased to $25 million, or $0.15 per share, compared with $21 million, or $0.12 per share.

Brand performance

Net revenues from continuing operations by brand and channel for the second quarter of fiscal 2014 compared with the second quarter of fiscal 2013 were as follows.

Brands (constant currency):

- Quiksilver decreased $13 million, or 7 percent, to $167 million.

- Roxy decreased $7 million, or 6 percent, to $121 million.

- DC decreased $24 million, or 19 percent, to $103 million.

Distribution channels (constant currency):

- Wholesale revenues decreased 15 percent to $286 million.

- Retail revenues were flat at $90 million. Same-store sales in company-owned retail stores increased 1 percent.

- Company-owned retail stores totaled 658 at the end of the fiscal 2014 second quarter compared with 630 at the end of the fiscal 2013 second quarter.

- E-commerce revenues grew 23 percent to $30 million.

- Emerging markets generated net revenue growth of 28 percent in constant currency.

Outlook:

The company anticipates that the general sales trends of recent quarters compared to the same prior year period will continue into the second half of fiscal 2014 with continued net revenue declines in the North America and Europe wholesale channels being partially offset by net revenue growth in emerging markets and e-commerce. The company also anticipates some continued year-over-year gross margin improvements in the second half of fiscal 2014, and that pro-forma adjusted EBITDA for fiscal 2014 will be below the $118 million achieved in fiscal 2013.

The company said that it has revised the timing for achieving its Profit Improvement Plan adjusted EBITDA target to the end of fiscal 2017.