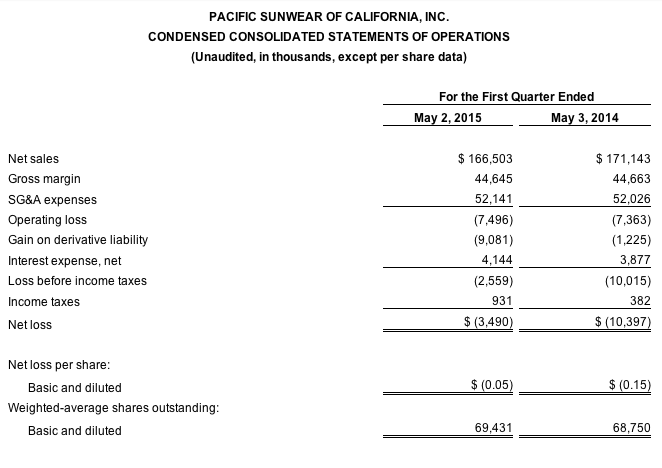

Pacific Sunwear of California, Inc. reported sales slid 2.7 percent in the first quarter, to $166.5 million from $171.1 million for the first quarter of fiscal 2014 ended May 3, 2014. Comparable store sales for the first quarter of fiscal 2015 decreased 2 percent. The company ended the first quarter of fiscal 2015 with 605 stores versus 618 stores a year ago.

On a GAAP basis, the company reported a net loss of $3.5 million, or 5 cents a share, compared to a net loss of $10.4 million, or 15 cents, for the first quarter of fiscal 2014. The net loss for the company's first quarter of fiscal 2015 included a non-cash gain of $9.1 million, or $0.13 per diluted share, compared to a non-cash gain of $1.2 million, or 2 cents per diluted share, for the first quarter of fiscal 2014 related to the derivative liability that resulted from the issuance of the Convertible Series B Preferred Stock (the “Series B Preferred”) in connection with the term loan financing the company completed in December 2011.

On a non-GAAP basis, excluding the non-cash gain on the derivative liability and assuming a tax benefit of approximately $3.0 million, the company would have incurred a net loss for the first quarter of fiscal 2015 of $8.6 million, or 12 cents per diluted share, as compared to a net loss of $7.4 million, or 11 cents per diluted share, for the same period a year ago.

“Continued increases in merchandise margins offset our first quarterly negative sales comp in more than three years,” said Gary H. Schoenfeld, president and chief executive officer. “Some key categories including shorts and non-apparel have underperformed, which is also reflected in our near-term outlook for the second quarter. Yet as we look ahead to the back half of this year, we believe the strength of several key brand initiatives, coupled with anticipated growth in long bottoms will get us back to positive comp store sales along with further increases in margins.”

Financial Outlook for Second Fiscal Quarter of 2015

The company's guidance range for the second quarter of fiscal 2015 contemplates a non-GAAP net (loss) income per diluted share of between a loss of 5 cents and a profit of 1 cent, compared to loss of 3 cents in the second quarter of fiscal 2014.

The forecasted second quarter non-GAAP net (loss) income per diluted share guidance range is based on the following assumptions:

- Comparable store sales from -4 percent to flat;

- Net sales from $201 million to $209 million;

- Gross margin rate, including buying, distribution and occupancy, of 27 percent to 29 percent;

- SG&A expenses in the range of $54 million to $56 million; and

- Applicable non-GAAP adjustments are tax effected using a normalized annual income tax rate.

The company's second fiscal quarter of 2015 guidance range excludes the quarterly impact of the change in the fair value of the derivative liability due to the inherently variable nature of this financial instrument.

Derivative Liability

In fiscal 2011, as a result of the issuance of the Series B Preferred in connection with the company's $60 million senior secured term loan financing with an affiliate of Golden Gate Capital, the company recorded a derivative liability equal to approximately $15 million, which represents the fair value of the Series B Preferred upon issuance. In accordance with applicable U.S. GAAP, the company has marked this derivative liability to fair value through earnings and will continue to do so on a quarterly basis until the shares of Series B Preferred are either converted into shares of the company's common stock or until the conversion rights expire (December 2021).

As of May 28, 2015, the company operated 604 stores in all 50 states and Puerto Rico.