With a 15 percent revenue gain and 120-basis point improvement in gross margins, Nike Inc. chalked up yet another impressive quarterly performance.

With a 15 percent revenue gain and 120-basis point improvement in gross margins, Nike Inc. chalked up yet another impressive quarterly performance.

Earnings rose 22.7 percent to $655 million, 74 cents a share, exceeding Wall Street’s consensus estimate of 70 cents a share.

On a currency neutral (c-n) basis, revenue increased 18 percent as the Nike Brand grew 17 percent and Converse increased 24 percent. Also on a c-n basis, Nike Brand futures orders grew 11 percent, driven by a 6 percent increase in average selling prices and a 5 percent increase in units.

The one downside was the continued negative impact of foreign currency headwinds, which caused reported orders to increase only 7 percent. That marked Nike’s slowest futures growth rate in four quarters.

On a conference call with analysts, Don Blair, CFO, noted that over the last 90 days the dollar had strengthened against most other currencies and the “FX markets have been extremely volatile.” At the same time, however, he noted that over the same period “we've seen our business performance accelerate and we expect that trend to continue into the second half of FY15.”

Indeed, the 11-percent gain on a c-n basis in futures came despite robust prior-year orders for global football product in advance of the 2014 World Cup.

Excluding global football, total futures order growth this quarter was essentially in line with the 14 percent c-n gain seen at the close of its first quarter. Specifically, the latest quarter's futures growth was led by double-digit expansion in North America, Europe and Greater China, with strong demand across multiple categories including sportswear, basketball and running.

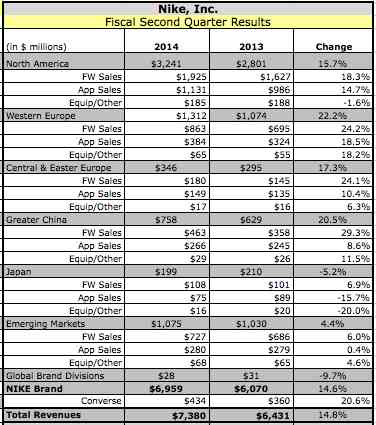

Total global Nike Brand revenues rose 14.6 percent to $6.96 billion. The 17 percent gain in a c-n basis was led by a 21 percent gain in Footwear, followed by Apparel, ahead 13 percent; and Equipment, up 5 percent.

All geographies grew in the quarter as well as all categories except golf. Standouts included Basketball, which saw its 13th consecutive quarter of double-digit growth, led by strong sell-through of key Nike basketball footwear styles like the LeBron 12 and the KD 7. Jordan revenues were driven by the Air Jordan 29 as well as rereleases like the Retro Jordan 6. Women’s also continued to see momentum in the quarter and is on target to reach its goal of $7 billion in annual sales by FY17.

Nike Brand DTC (direct-to-consumer) revenue increased 30 percent, driven by all concepts, notably a 66 percent hike in online sales. EBITDA for Nike Brand rose 25.6 percent to $1.07 billion.

In the North America region, Nike Brand sales in the quarter grew 15.7 percent to $3.24 billion. Footwear was ahead 18.3 percent to $1.93 billion and Apparel advanced 14.7 percent to $1.13 billion. Equipment slipped 1.6 percent to $185 million.

The overall gains in the NA region were led by double-digit growth in basketball, sportswear, men's training and women's training. DTC revenues grew 18 percent, driven by 8 percent comp growth, continued strong growth of Nike.com and new stores. On a reported basis, Q2 EBIT for North America grew 21.3 percent to $785 million, driven by revenue growth and gross margin expansion.

“North America offers a roadmap for other geographies as we continue to deliver strong growth in this critical marketplace,” said Trevor Edwards, president, Nike Brand, on the call. “By developing deep consumer relationships, through the category offense, and delivering segmented and differentiated retail destination, we've driven sustained profitable growth even in more developed markets where we already have significant market share.”

Edwards said Nike Brand has continued to see momentum in the NA region in basketball, sportswear, and men's training while a “clear acceleration” has come in its women's and young athlete businesses.

He credited part of the strong regional performance to the success of in-store concepts such as the Fieldhouse with Dick's Sporting Goods, the Track Club at The Finish Line, and Fly Zone with Foot Locker.

In Western Europe, sales for Nike Brand climbed 22.1 percent on a reported basis to $1.31 billion and grew 24 percent on a c-n basis. The growth was broad-based with every territory increasing at a double-digit rate. Every key category also grew, led by double-digit growth for sportswear, football, and running. On a c-n basis by category, Footwear grew 26 percent, Apparel gained 20 percent, and Equipment advanced 18 percent.

“Wholesale partners like Foot Locker, JD Sports and Intersport are creating compelling category destinations in cities across the geography that are fueling growth,” said Edwards. Its DTC business in Western Europe ran up 40 percent.

Western Europe’s EBITDA vaulted 112.2 percent to $261 million, driven primarily by strong revenue growth, gross margin expansion and SG&A leverage. EBIT growth for Western Europe also benefited from two nonoperating items: A legal charge included in last year's Q2 results, and more favorable standardized exchange rates used for geography segment reporting.

Emerging Markets grew 4.4 percent $1.08 billion while gaining 13 percent on a c-n basis. All territories on a c-n basis except Mexico and Korea posted higher revenues, with five of them growing at a double-digit rate. From a category perspective, the growth was led by sportswear, basketball and running. On a c-n basis, sales were led by a 15 percent hike in Footwear while Apparel and Equipment were both up 8 percent.

In Brazil, Q2 revenue growth slowed due to “volatile macroeconomic conditions.” Edward said near-term Nike is working on better managing the flow of product into the marketplace and clearing excess inventory. But he said the country’s “passion for sport and the Nike Brand remains strong.”

Inventories remain high in Mexico due to transition issues with a distribution center in the early FY14. Normalized inventory levels are expected there by the end of the FY15.

EBITDA in the Emerging Markets slid 2.9 percent to $236 million, primarily due to lower gross margin on the FX headwinds and higher operating overhead for new retail stores.

In Greater China, revenues for Nike Brand jumped 20.5 percent to $758 million and moved up 21 percent on a c-n basis. The gains were led by double-digit growth in sportswear, running and basketball. By category on a c-n basis, Footwear led the gains, up 30 percent; followed by Equipment, ahead 12 percent; and Apparel, up 9 percent.

Edwards said China is benefiting from efforts to reset the marketplace with expanding profitability at wholesale doors it’s re-profiled and “exceptional numbers” at its own stores in the region.

“We've driven this return to growth by focusing on increased retail productivity, differentiating our point of distribution and creating more focused consumer experiences,” said Edwards. “This allows us to provide a narrow, yet deep product assortment in each door. This better serves the consumer and also allows us to maintain the healthy inventory levels we are currently seeing in the market.”

EBITDA in Greater China leapt 31.0 percent to $258 million, fueled by strong revenue growth and significant gross margin expansion, partially offset by increased investments in DTC and its new Shanghai campus. Given the continuing benefits of strategy to reset the market, Nike now expects full-year FY15 revenue in China to grow at a mid-teens rate.

In Central & Eastern Europe, sales for Nike Brand grew 17.3 percent on a reported basis to $346 million while expanding 25 percent on a c-n basis. Excluding Israel, every territory reported double-digit revenue growth and every key category expanded except action sports. On a c-n basis, sales jumped 32 percent in Footwear, 19 percent in Apparel, and 18 percent in Equipment. Central & Eastern Europe EBITDA increased 18.8 percent to $57 million, driven by strong revenue growth in SG& A leverage.

In Japan, sales for Nike Brand gave back 5.3 percent to $758 million but gained 3 percent on a c-n basis. Sales on a c-n basis grew 16 percent in Footwear in the region but fell 8 percent in Apparel and 13 percent in Equipment. EBITDA was down 38.3 percent to $29 million.

Converse revenues rose 20.6 percent to $434 million and gained 24 percent on a c-n basis. The gains were driven by continued strength in existing direct distribution markets such as the US, DTC growth, and market conversions in Europe and Asia. Converse's EBITDA was down 12.0 percent to $88 million, driven by investments in infrastructure, demand creation and DTC to enable long-term growth.

Gross margin increased 120 basis points to 45.1 percent. The increase was primarily attributable to a shift in mix to higher margin products, continued growth in ITS higher-margin DTC business and a modest benefit from foreign exchange. Those factors were partially offset by higher product input costs.

Selling and administrative expense increased 17 percent to $2.4 billion. Demand creation expense was $766 million, up 11 percent versus the prior year, driven by marketing support for new product launches, digital brand marketing and consumer events. Operating overhead expense increased 19 percent to $1.7 billion, reflecting growth in the DTC business, as well as investments in operational infrastructure and digital capabilities and engagement.

Inventories at Nov. 30 were up 11 percent and “remain healthy overall” with the majority of the growth in North America, Europe and Converse and driven in part by the expansion of our DTC business. Said Blair, “We continue to focus on inventory management with particular attention on Brazil and Mexico where we're working to balance supply and demand to position those markets for ongoing growth.”

The company kept its guidance unchanged for the year.

For the third quarter, Nike expects constant dollar revenue growth in the low teens with reported revenue growth about three points lower, reflecting the stronger dollar. For the full year, constant dollar revenue growth is projected in the low double digits with reported revenue growth 2 to 3 points lower. Gross margin is expected to expand by about 100 basis points in the quarter and 100 to 125 basis points for the year.

Concluded Blair, “Notwithstanding the volatility we've seen recently in the macro environment, we're confident we're on track to deliver strong growth for this fiscal year.”