Yue Yuen Industrial (Holdings) Limited recorded revenue of $9,121.4 million in 2017, representing a growth of 7.6 percent, compared to the previous year. The profit attributable to owners of the company declined by 2.9 percent to $519.2 million, as compared to $534.6 million for the previous year. Basic earnings per share decreased by 2.8 percent to 31.55 cents, as compared with 32.47 cents for the previous year.

Excluding all items of non-recurring operating nature, the recurring profit for the year decreased by 4.6 percent to $500.8 million, compared to a recurring profit of $525.1 million for the previous year. The Group’s nonrecurring profit in the year under review amounted to $18.4 million, which included fair value gain on derivative financial instruments, as well as a gain of $19.1 million on the disposal of associates and subsidiaries. The profit attributable to owners of the company for the same period of last year included a non-recurring profit of $9.4 million.

The Board is pleased to propose a final dividend of HK$1.1 per share for the year ended December 31, 2017 (2016: HK$1.00 per share), amounting to a dividend per share for the year of HK$5.0 (2016: HK$1.40 per share), inclive of an interim dividend of HK$0.40 per share (2016: HK$0.40 per share) and a one-off special dividend of HK$3.50 per share (2016: NIL).

Business Review

Revenue

In the financial year ended December 31, 2017, the revenue attributed to the group’s manufacturing business improved by 0.9 percent, compared to the previous year, while the volume of footwear produced grew to 324.6 million pairs.

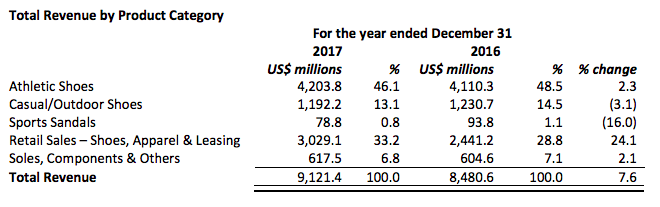

Total Revenue by Product Category

To hedge against rising competition and market uncertainties, the group will further leverage its cores strengths and edges to safeguard its stainable and steady growth. This includes continuing to enhance its product and material development capability, and exploring vertical integration and related business opportunities to tap new markets, which could also create synergies for the overall Group in the long-term.

In the financial year ended December 31, 2017, the revenue attributable to Pou Sheng International (Holdings) Limited (“Pou Sheng”), the Group’s retail subsidiary, grew by 13.6 percent to $2,775.4 million, compared to $2,443.7 million in the previous year. In RMB terms (Pou Sheng’s reporting currency), revenue increased by 16.0 percent to RMB18,833.3 million, compared to RMB16,236.4 million in the previous year. As of December 31, 2017, Pou Sheng had 5,465 directly operated retail outlets and 3,313 stores operated by sub-distributors in the PRC.

Gross Profit

The gross profit of the group’s manufacturing business improved during the period under review, despite facing rising wages and raw material price volatility. The group managed to expand its gross margin by achieving better operational efficiency, while also increasing its investment in automation-related areas.

Pou Sheng’s gross profit margin declined from 35.5 percent in the previo year to 35.0 percent due to increased discounting and allowances on the aging inventory of emerging brands.

Selling and Distribution Expenses, and Administrative Expenses

The group’s total selling and distribution expenses for the year under review amounted to $986.2 million (2016: $804.7 million), equivalent to approximately 10.8 percent (2016: 9.5 percent) of revenue. The increase in selling and distribution expenses was attributable mostly to the optimization and upgrade of directly operated retail outlets, increased remuneration for sales staff at Pou Sheng, as well as the consolidation of Texas Clothing Group, a new subsidiary engaged in the apparel wholesale business that the Group acquired in the second quarter of the year under review.

Administrative expenses for the year under review amounted to $635.8 million (2016: $611.1 million), equivalent to approximately 7.0 percent (2016: 7.2 percent) of revenue, remaining stable.

Share of Results from Associates and Joint Ventures

During the year under review, the share of results from associates and joint ventures was a combined profit of $64.6 million, compared to a combined profit of $66.8 million in the previo financial year.

Prospects

The manufacturing business will continue to face market uncertainties, intense competition and potential risks arising from the challenging and dynamic operating environment. These risks include stronger-than-expected wage inflation, raw material price volatility and a weakening dollar against regional Asian currencies. That said, economic growth and consumer sentiment should continue to improve in most major economies, including the United States, the PRC and the Eurozone, providing new growth opportunities for the group and its customers.

In the retail segment, Pou Sheng continues to face increased market competition and other challenges in the sporting goods industry and is exploring and investing heavily in a variety of initiatives to adapt to the shifting market dynamics. All these initiatives require significant investment and resources. As a result, on January 21, 2018, the group’s parent company, Pou Chen Corporation (“Pou Chen”), requested Pou Sheng’s Board to put forward the proposal to the Scheme Shareholders for the privatization of Pou Sheng by Pou Chen (the “Proposal”) by way of a scheme of arrangement under Section 99 of the Bermuda Companies Act (the “Scheme”). If the Proposal is confirmed and implemented, the company will effectively disposing all of its Pou Sheng shares, representing approximately 62.38 percent of the total issued share capital of Pou Sheng, which provides the company with a cash exit, and enables the company to agnate aggregate net proceeds of approximately HK$6,759 million which will be distributed to its shareholders by way of a one-off special dividend of HK$4.1 per share. Yue Yuen is expected to recognize a gain before transaction costs of approximately $305 million from the disposal.

For further details of the Proposal, please refer to the joint announcement of the company, Pou Chen and Pou Sheng dated January 21, 2018, as well as the Scheme document jointly issued by Pou Sheng and Pou Chen dated March 12, 2018.

The disposal of Pou Sheng will enable the group to focus more on its core manufacturing segment, ensuring that it will remain a global manufacturing leader – of both athletic and casual/outdoor footwear, as well as a growing suite of other products – while upholding its fundamental principles and core values, as well as its commitment to world-class corporate social responsibility.

Looking forward, the group’s main priority is to increase revenue growth by providing differentiated services and irreplaceable value to its customers, while growing profitability through the increased of automation, innovation and production workflow optimization. This will require continuo investments in technology, process re-engineering and other enhancements to the group’s manufacturing capabilities. This will enable it to continue providing branded customers with end-to-end manufacturing solutions, maintaining solid profitability so as to ensure stainable returns for shareholders.

Lu Chin Chu, chairman, commented, “We are pleased with the Group’s solid financial performance, despite growing competition and uncertainties within the current dynamic operating environment. We will continue to invest in technology, process re-engineering and other enhancements in order to strengthen our end-to-end capabilities and safeguard our stainable and steady growth.”