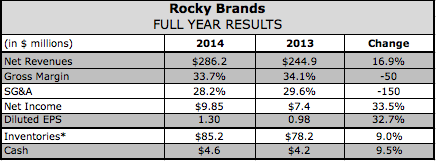

With broad-based growth across categories, Rocky Brands, Inc. reported fourth-quarter sales increased 28.2 percent to a record $78.9 million. Earnings jumped 125.2 percent to $4.47 million, or 59 cents a share.

With broad-based growth across categories, Rocky Brands, Inc. reported fourth-quarter sales increased 28.2 percent to a record $78.9 million. Earnings jumped 125.2 percent to $4.47 million, or 59 cents a share.

On a conference call with analysts, David Sharp, president and CEO, said wholesale revenues grew 30 percent in the quarter to $62.0 million, including $3.3 million in Creative Recreation branded sales acquired last year.

Work, its largest category, advanced 15 percent, driven primarily by the Georgia Boot brand and to a lesser extent the Rocky brand. Demand for work categories such as farm and ranch, logging and industrial supported Georgia Boot’s growth. Colder weather late in the quarter boosted Rocky in the category.

Western footwear sales jumped 47 percent, driven by strong gains for both the Durango and Rocky. Most of the growth has come from increased demand in the cold western and farm channels. Solid growth was seen in the more fashion forward Durango City line of boots.

Hunting climbed 33 percent, driven by both unit growth and higher selling prices. Growth was broad based and included national outdoor and sporting goods retailers like Cabela's, Bass Pro and Dick SG as well as its network of regional and independent dealers across the country.

Creative Recreation, a sneaker-inspired collection, “has started to become a more meaningful contributor to our profitability following the work we’ve done to improve the brand’s supply chain,” said Sharp. Rich Cofinco, co-founder of Creative Recreation, has returned as creative director and the brand has expanded its sales team in order to broaden coverage, especially the under-penetrated East Coast.

Retail sales increased 6.6 percent to $13.7 million while military segment sales increased to $3.2 million compared to $1.0 million in the fourth quarter of 2013.

Gross margins in the quarter reached 35.0 percent of sales versus 35.4 percent a year ago, with the decline reflecting higher military sales which carry lower gross margins than wholesale and retail. SG&A expenses were lowered 330 basis points to 26.2 percent of sales.

Looking ahead, Sharp predicted “another year of solid growth in 2015.” With gross margins remaining stable and SG&A dollars growing only modestly, EPS is expected to expand “at a much faster pace” than sales. Sharp said that despite the strong gains recently, new product collections are leading to additional shelf space with its key retail partners and new distribution – includes department stores, leather shoe stores and specialty boutiques – “that is helping us reach a wider consumer audience.”